STEEL AND CEMENT INDUSTRY

Bolstering the Infrastructure of Bangladesh

From infrastructural development to industrial, from household machineries to surgical scalpels, the presence of steel is everywhere. Thus, the growth in the production and use of steel is undoubtedly a key indicator of development for any country. As per the World Steel Association, from 2008 to 2018 the worldwide production of steel increased by 35% and use of steel increased by 42%. Moreover, majority of the total production takes place in Asia. Among the top 20 producing countries China, India and Japan secured top the top 3 positions. Even though China leads this market in case of both consumption and production, this particular sector of Bangladesh has been showing continuous growth for last couple of years, making itself self-sufficient in producing raw materials.

Worldwide crude steel production 2008 vs 2018:

![]()

Key Players and market share

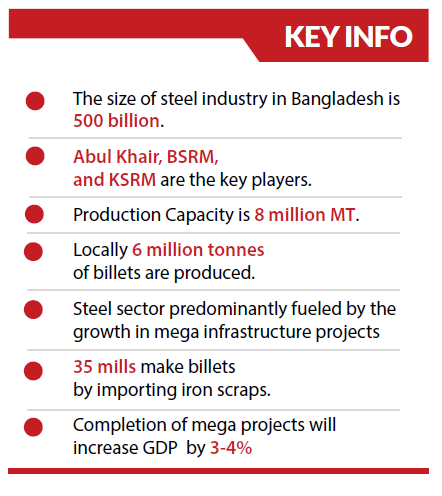

The nature of the steel industry of Bangladesh can be defined as oligopoly. Even though there are around 400 mills having production capacity of 8 million MT, top three steel makers, Abul Khair, BSRM, and KSRM cover more than 50% of the annual demand of the country. Among the producers Abul Khair Group is the largest having the capacity of producing 1.3 Million MT high quality graded hot rolled steel bars per annum. Although Abul Khair Steel is capable of producing 1.4 million MT per annum, they are planning to expand it till 1.6 million MT. BSRM also has the production capacity of 1.2 million MT annually. Even though BSRM has billet melting plant, the group still has to import iron scrap, whereas Abul Khair Steel does not need to import. However, to cater the growing demand other producers like KSRM and GPS ispat are increasing their production capacity.

Production Capacity

The BDT 500 billion sized industry has the production capacity of 8 million MT. Having the growth rate of 37.5% in 2018 total consumption of Bangladesh was 7.5 million MT. According to the leading manufacturers, more than 3 million MT of steel was produced in 2015 representing a market value of $3.57 billion which is estimated to double by 2022.

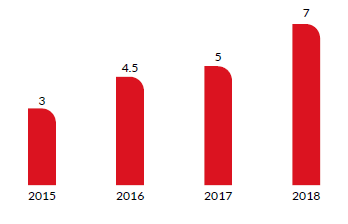

Total steel production in Bangladesh (In mn Tonnes)

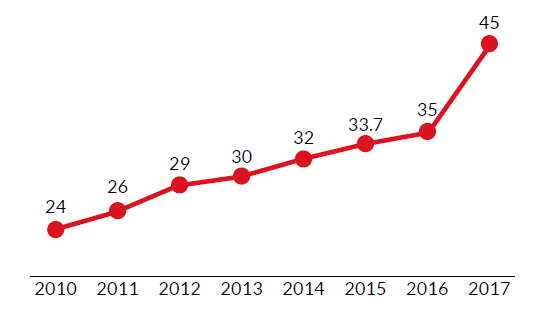

Per capita steel consumption

From 2012 to 2017 per capita steel consumption of Bangladesh increased from 25 kg to 45 kg. It is assumed that the consumption might increase to 73 kg by 2022. However, Bangladesh is falling behind in per capita consumption compared to global average and the peer countries. As per World steel association, the global average is 208kg, whereas in India the average is 65.2kg and in Pakistan 42kg. Developed countries are undoubtedly ahead in consumption. Japan has per capita consumption of 1000kg, South Korea 400 kg and 600 kg in USA.

Per Capita steel consumption in Bangladesh (kg)

Import/ Production of raw materials/ Supply side (iron scrap):

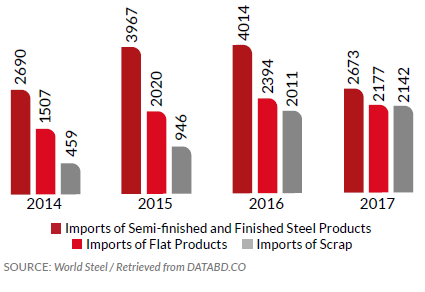

Major Imports in Steel Industry: Bangladesh (In thousand MT)

Scrap, sponge, and pig iron are major raw materials for steel smelting in Bangladesh with imports growing from 2.5 million MT in 2016 to 4-4.5 million MT in 2018. The majority of imports are scraps, flat products, and semi-finished and finished steel products making up a total of 6.992 million MT or over 93% of all imports. Even five years ago, Bangladesh had to import almost half of the required raw-materials. Thanks to the huge investment made by the leading mills, Bangladesh is now self-sufficient in billet manufacturing and this increased the production of key raw material of steel products. Bangladesh now produces locally 6 million tonnes of billet which is enough to make 5.5 million tonnes of high quality rods. The expansion projects of BSRM, Abul Khair Steel, GPH Ispat, KSRM, Metrocem and Anwar Ispat were mainly driven by the growing demand in the construction sector caused by the mega projects taken by the government. According to customs data in 2014-15 Bangladesh imported 1.7 million tonnes of billets which fell significantly to 0.17 million tonnes in 2017-18 saving a large amount of foreign money. Improvement in power generation also has a huge contribution in making the producers invest more in expansion. However, currently 35 mills make billet by importing iron scrap which has increased scrap import and the usage of scrap cuts the steel production cost by at least $158 per tonnes.

If the billets were not produced locally, the price of steel would have been BDT 12,000 higher per tonne than the existing market price.

Key Info:

Pricing:

The breakthrough in the local production of billet plays a significant role in pricing of the steel products as well.However, the price of 60-grade rod is around BDT 62,000 to 67,000 per tonne. Government’s policy support and duty hike in imports also played a vital role in decreasing billet import. Now, the importers have to pay BDT 800 advance income tax along with 20% regulatory duty, 15% VAT and 4% advance trade VAT.

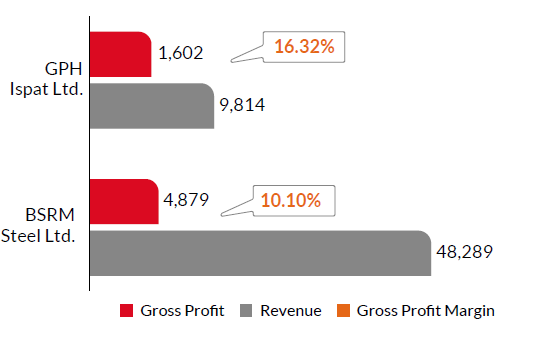

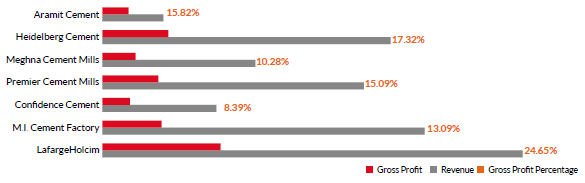

Revenue and profit comparison of listed steel and cement companies:

By nature, steel manufacturing is a heavy business, thus, cost of production for sold goods can even cover 80-90%. This reflects the revenue vs gross profit comparison between BSRM Steels Ltd, a DSE listed company and GPH Ispat Ltd, a non-listed company.

Bangladesh-China and Bangladesh-Japan joint venture integrated steel plant

Aiming to produce 2 million tonnes integrated iron and steel production annually, Chinese steel giant Kunming Iron and Steel Holding Company (KISC) is all set to invest US$ 2.3 billion in a steel manufacturing project in Mirersarai. Which is considered as the largest investment in manufacturing sector in the country. Moreover, Nippon Steel and Sumitomo Metal Corporation, Japan’s largest steelmaker is also set to invest around $60mn through a joint venture with a local steelmaker, McDonald Steel Building Products.

Growth Divers

The highest steel consuming sectors of Bangladesh are infrastructural projects of commercial, public and housing sectors. Among these public sector consumes the highest amount of production because of its mega projects consisting of annual development plans (ADP) and infrastructural projects. For example, completely locally manufactured steels are used in projects like Rooppur nuclear power plant and Padma Bridge. This year’s ADP allocation is 17.2% higher than last years. Moreover, project aid allocation for Rooppur nuclear power plant is 16.7% of overall ADP allocation. This year’s ADP consists of 1475 projects, out of which 41 projects are new and 673 projects will continue till FY21, which means there will be an increasing demand of steels in FY20. Moreover, 5 out of 14 mega projects are scheduled to be completed by FY20 but the progress does not comply.

Impact of budgetary tax and VAT measures on price

In the proposed budget for 2019-20, BDT 1000 per tonee tax is imposed on the import of mild steel rod (MS rod). It was BDT 2000 in the initial proposal but then it was decreased. Moreover, specific tax on MS products made from local/imported scrap for re-rolling has also been reduced to BDT. 1200 per tonne. From the existing VAT rate of 5% specific tax for ship scrap has been fixed at Tk 1,000. Ingot/billet produced from melt able scrap and MS products produced from ingot/billet are subject to BDT 2000 per tonne. However, even though the specific tax is downwardly revised, the VAT on MS products will go up till BDT 250 per tonne.

Environment issue

Since Bangladesh don’t possess any iron ore mine, besides importing, Bangladesh has to rely on shipbreaking industry largely as a major source of raw material- iron scrap. However, even though Chittagong is considered as world’s largest ship breaking yard and the cheapest place to break ships, the industry is exposed to some questionable practices of the ship breakers which causes serious environmental and human hazards. This industry affects the environment in some seriously harmful ways and in 2018, 18ship-breakers died and 12 others were injured in 17workplace accidents. However, EU has become very strict about maintaining a standard to reduce the hazard, where only EU registered ships can be recycled only at EU approved sustainable facilities but it is tough for most of the South Asian ship breakers. However, now-a-days, industries are shifting towards importing more than sourcing from ship breakers.

Challenges of steel industry

The biggest challenge of the steel industry is to maintain sufficient supply of raw materials. With the expansion of billet manufacturing, the problem is somewhat eased. However, Bangladesh has to depend partially on imports thus, it is very important to ensure proper supply of raw materials to keep the wheels running.

Apart from that, steel industry is a heavy manufacturing industry which requires vast and continuous amount of power and gas. Any unwanted situation or fall in this two sectors can hamper the steel industry largely.

However, financial and regulatory consistency is also important to run such huge industry. As discussed before ship breaking industry is a major source of raw materials. If they fail to maintain standards, it will also affect the steel industry.

Bangladesh Cement Industry

The emergence of the cement industry in Bangladesh goes as far back as 1994. This was in response to the huge local demand and thus import of cement from foreign lands. By 2003, the industry had not only placated local demand, but also started exports. Championed first by Crown Cement (otherwise known as M.I Cement), several cement producers have exported their product to the seven sister regions and West Bengal, with potential to further accelerate the export volume.

Market Share

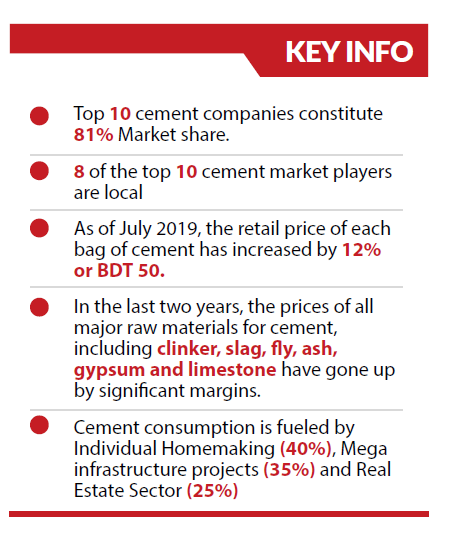

By the end of 2018, local manufacturers of cement had seized a majority of the market share, a complete reversal of the scenario from 15 years earlier, when the multinational companies ruled over the industry. Two global cement groups, the United Arab Emirates based company – Emirates Cement, and the Mexico based company – Cemex were forced to divest their operations in Bangladesh by 2016. The top 10 cement market players in the country have in hand approximately 81% of the market share. Among them, 8 are local companies and the other 2 are multinational. The local companies have been thriving in the industry with deft marketing strategies that include lower pricing, extensive branding and better customer relationships. A scenario demonstrating the market share of cement industry (containing only the DSE listed companies by distinction) are as follows:

Market Share of Cement Industry

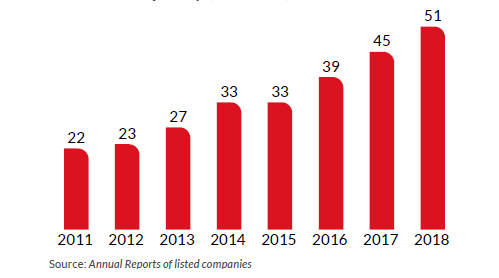

Production Capacity

Industry players have been expanding their capacities aggressively in speculation of future growth. In recent years, cement producers have significantly increased production capacity, all in anticipation of huge demand in the industry given the soaring income level, outstanding levels of economic growth, and the large number of mega-projects being undertaken.

Effective Capacity (Million MT)

Although over-capacity does exist in the industry, market demand is almost equal to the effective capacity during peak season. Total cement production capacity is expected to reach about 65 million metric tons by 2019. However, due to interruptions in power supply and other constraints, effective capacity is expected to be lower than those figures.

Pricing

Impact of taxes

Until the current fiscal year, cement manufacturers paid 5% Advance Income Tax (AIT) to import raw materials and the tax was adjustable. According to the National Board of Revenue (NBR) he AIT to be paid by cement manufacturers for import of raw materials will be treated as minimum tax from the fiscal year of 2019-2020. In the opinion cement industry insiders, the bid to consider5% AIT as minimum tax will put an increased burden on them. They already pay source tax against the supply of cement locally. In addition, manufacturers will have to pay 5%advance tax while importing raw materials and other required ingredients. This will increase operational cost and thus the retail prices of cement, according to the Bangladesh Cement Manufacturers’ Association.

Impact of utilities costs

Ancillary to this, the government has increased gas prices by almost 38%, raising prices from BDT 7.76 to BDT 10.7 per cubic foot for manufacturing industries, by almost 41% (from BDT 3.16 to BDT 4.45) for power generation companies and by 44% (BDT 9.62 to BDT 13.85) for captive power companies. As per the estimation of the Bangladesh Cement Manufacturers Association, production costs for cement manufacturers may go up by as much as BDT 11 per bag on average as a consequence of the increase in gas prices.

Impact of freight costs

Freight costs have also increased due to higher fuel and charter costs. This situation has only been exacerbated by major devaluation of the Bangladeshi Taka versus the US Dollar, sharp rise of transportation cost due to weight restrictions imposed by the government on highways and spiraling financial costs due to liquidity risks

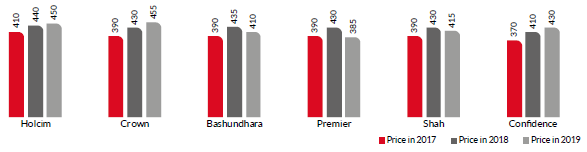

Retail Prices of Cement in Dhaka (BDT per 50 kg bag)

Import Price (BDT per MT)

Change in prices

According to a survey done by the Daily Star in February of the current year, local cement brands were selling within a price range of BDT 395 to BDT 420 per bag. By comparison, multinational brands were charging between BDT 418 to BDT 450. As of July 2019, the retail price of each bag of cement has increased by 12% or BDT 50. This development is sure to push up construction costs, be it government mega projects or private construction. However due to the existing rivalry and price war among the manufacturers in the industry, it is unlikely that the prices will increase by that much.

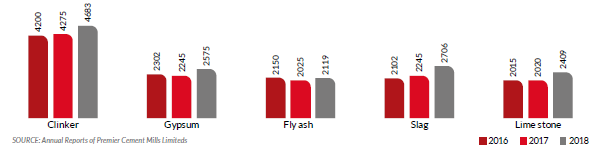

Import

In the last two years, the prices of all major raw materials for cement, including clinker, slag, fly, ash, gypsum and limestone went up by significant margins. Clinker, which is the main raw material for production of cement, is exported almost exclusively from Vietnam (90% of Bangladesh’s clinker import is from Vietnam). In 2017, in an effort to preserve the environment from further harm, the government of

China began discouraging clinker production locally, which made them seek out clinker from Vietnam, their nearest source for the material. Following the sudden increase in demand, the price of clinker rose by almost

USD 10 per metric ton, bringing the price of clinker up to USD 47-50 per ton. This has caused the cement manufacturers to raise their prices since early 2018.

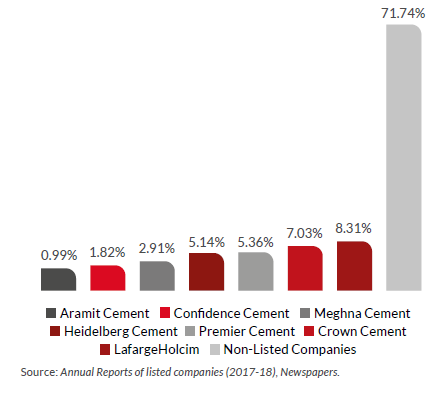

Revenue and Profit comparison of Listed Cement Companies (BDT Million)

Challenges

There are 32 working cement factories in the country among which 4 are multinational and the other 28 are local. Only 7 of these companies are listed on the Dhaka Stock Exchange. The industry faces challenges of low utilization of resources, a growing overcapacity and, sensitivity to prices of raw materials and energy required for production. The market is also highly sensitive to changes in foreign exchange rates as the majority of fuel and raw materials are imported from abroad. As stated previously in this article, the devaluation of Taka from (BDT 80/USD to BDT 84.29/USD), raised cost of production by a definitive margin, which in turn caused retail prices to go higher in 2018. Costs of production are further exacerbated due to government policy of allowing less truck loads to reduce pressure on roads. This has in turn pushed producers to turn to barges for transport on water to reduce costs. Although producers are seeking to transport cement and raw materials by boat, an inadequate supply of barges hinders progress. All together, these factors are contributing to operational inefficiencies despite measure taken by producers to reduce costs, such as strategically locating facilities to reduce high transportations costs.

Despite the many challenges at work, the cement industry has recently announced record sales in

2018, due to the increased consumption in rural and infrastructure projects. This year sales of 33 million metric tons took place, a 12% growth in consumption. Exports to India have also been on the rise with a 24% growth during July 2017 to May 2018 according to Export Promotion Bureau. MI Cement has also recently announced an expansion set to increase production capacity 76% by 2021 from a current 11,000 metric tons per day to 19,400 metric tons.

Environmental Issues:

The cement sector in Bangladesh is heavily influenced by seasonality due to Bangladesh’s subtropical monsoon climate. September to May are peak seasons when demand spikes as construction goes up, with demand declining in the time between May and September, with activity of varying depending on the duration of the rainy season.

Cement industry can harm the environment at all stages of production, use and even packaging. It creates airborne pollution by emitting carbon in the form of dust clouds. Concrete causes damage to even the most fertile of land. It also creates a lot of dust at the time of packaging and therefore, requires an Environment

Clearance Certificate (ECC). Companies that do not operate in accordance with proper guidelines are charged fines.

Way forward:

Prospects for overall growth in the sector is bright for the country in terms of increasing demand due to: Urbanization come, Real estate development Government mega projects. These factors drive industry growth. Infrastructural development ranging from the likes of the Metro Rail Project or the construction of the Padma Bridge to urbanization plans in Purbachal and Bashundhara, the market demand for steel and cement is on a constant rise and the future only seems brighter. However, uncertainty in price fluctuations due to imports of raw materials, fuel, logistics, and foreign exchange rate fluctuations are definitive challenges for the industry. Competitors are also expanding their capacity despite having unutilized facilities in anticipation of increasing demands. It is almost certain without a doubt that growth in this sector will continue, however, a question of profitability in terms of rising costs must be addressed for the industry to further flourish. In the same way that a large majority of cement producers have their own private road transportation, Bangladesh may see an increase in barges for water transportation to reduce costs. New technologies are also being adopted in order to improve operational efficiencies to not only reduce wastage in the industry but also reduce the amount of clinker required for production without sacrificing quality. This is especially important in the future as new players enter the market, and competitors seek greater profits in a current situation of price wars between competitors.

Even though Bangladesh is already self-sufficient in meeting the domestic needs, considering several mega projects, rapid boost in housing sector, EPZ and government’s concern about making industrialization smooth, it can be stated that there are scopes for the steel industry to grow more and go beyond the domestic horizon significantly. However, there are still some scopes to grow more. If the ship breaking industry is modernized and ensures proper law and regulations imposed by the regulatory authority, the steel industry will boom more significantly. Moreover, if production efficiency is ensured, low cost production will stop the foreign producers to enter our market.

Monthly Business Review - November 2019

In 2018 alone, total consumption of steel in Bangladesh was 7.5 million metric tons, recording 37.5% growth y-o-y. Per capita steel consumption almost doubled in five years, amounted to 45 kg in 2017. Steel production capacity soared to BDT 30 lakh tonnes in FY 15-16, from BDT 10 lakh tonnes in the preceding fiscal. Thanks to these mega infrastructural projects, Bangladesh is now self-sufficient in billet production, when even five years ago, the country had to import half of the total billet requirement to feed the domestic market. On the other hand, the sale of cement, another prime construction material, registered 12% growth in 2018 y-o-y. Cement consumption in Bangladesh is mostly rooted in individual homemaking (40%), followed by mega projects (35%) and real estate sector (25%). The cement industry, however faces far more significant challenges in the import area, with countries (especially Vietnam) racking up the price of raw materials such as clinker. The market price of cement rose in the past 2 years, this coupled with the fact that there are 32 cement manufacturers in the country and the existence of intense competition among them, makes pricing a significant challenge.

Download View