The Archive

Battery Industry in Bangladesh: Powering Up the Nation on the Go

The lead-acid battery industry, which has grown three to four times in the last decade and is valued at BDT 10,000 crore currently, serves a wide variety of purposes without which portability and mobility would have never been a possibility. Solar panels, easy bikes, battery-run rickshaws, passenger transports, commercial vehicles, IPS, UPS, and telecommunication towers—all these either run on batteries or require batteries as power storage. The fact that the lead-acid battery industry exported around USD 29 million worth of batteries on average in the last five fiscal years makes the industry a potential contributor to our foreign exchange earnings as well.

It is not unknown that the industry faces controversies due to the unregulated manufacturing and recycling operations of some market players. Just like many other industries dependent on imports of raw materials, the rising dollar price has affected the industry adversely. On top of that, the potential emergence of the local lithium battery industry may bring additional challenges. However, policymakers should come forward to create a conducive business environment for this decades-old industry and regularise the unregulated players to minimise the associated environmental and health risks and boost the country’s tax revenues.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Shattering Glass Ceilings: Women as Leaders of the Corporate World

The corporate landscape of Bangladesh is undergoing a transformation as diversity and inclusion are gaining overdue recognition. Women leaders are making notable strides, challenging traditional gender roles, and securing top positions in renowned corporations. This paradigm shift signifies a crucial step towards a more equitable and progressive work environment where talent and meritocracy prevail over gender biases.

Bangladesh is inching closer to achieving parity in tertiary education, meaning women are no less capable of achieving success in competitive arenas. Translating this gender parity to workplaces is what is required to ensure women's empowerment. However, despite advancements, the gender gap in workplaces remains, with women still underrepresented in decision-making roles. Hence, it's imperative to capitalise on women's capabilities by creating a supportive work culture that harnesses their talents and expertise.

Empowering women has impacts beyond just the corporates. It drives positive economic growth and serves as a beacon of inspiration for future generations. By advocating gender equality and fostering inclusive workplaces, Bangladesh can pave the way for a more prosperous and equitable society where everyone has the opportunity to thrive and succeed.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Self-Reliant Particle Board Industry in Bangladesh: A Sustainable Solution For Furniture And Office Décor

Development in the manufacturing and service industries says a lot about a country’s economic strength. Bangladesh, being a developing country, has a few manufacturing industries in which it has achieved significant value addition and self-sufficiency. The particle board industry is undoubtedly one of them. The abundance of raw materials and cheap labour have fueled the growth of this industry, and the industry has already created a market valued at more than BDT 5,000 crore.

The particle board manufacturing industry started its journey in the country in 1962 by Star Particle Board Mills Ltd., a concern of Partex Star Group. Now, several conglomerates are catering their pie in the industry. It is also noteworthy that the industry has created a conducive environment for small and medium enterprises to grow here. What is unique about the particle board industry is that it promotes sustainability by requiring fewer trees to be cut and recycling waste timber. Though the industry is growing exponentially, it is facing challenges due to the rising dollar price, as adhesives and some other chemicals still need to be imported. Moreover, rising energy costs are a big concern. However, the industry has all the potential to be a contributor to exports if it receives adequate policy support. We can surely expect a sustainable tomorrow with the growth of industries like the particle board industry.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Rechanneling Insurance: Dawning an Era of Bancassurance in Bangladesh

Bancassurance, the strategic collaboration between banks and insurance companies, is set to bolster the largely untapped insurance industry in Bangladesh. Prominent in Europe and some parts of Asia, bancassurance is defined as the symbiotic relationship between banks and insurance companies, where banks receive a commission for opening an avenue for selling insurance policies while insurance companies gain access to a massive network of clients through banking channels. With a penetration rate of a mere 0.5% and a market size of BDT 5,000 crore in Bangladesh, this synergy can serve as a powerful tool for increasing insurance penetration and financial inclusion in Bangladesh.

Developing economies necessitate the demand for insurance, with higher incomes translating to an increased insured population. Gradually, as more and more people avail of insurance policies and bring themselves under insurance channels, the premium size is likely to experience a decline and become affordable to the mass population.

The inadequate claims settlement ratio has held back the insurance penetration rate in Bangladesh to a large extent. Delays in settling claims after policy maturity, insufficient returns due to inadequate fund investment, and financial irregularities pose significant challenges for insurance companies. However, the handshake through bancassurance between banks and insurance companies is expected to foster a conducive environment and bring the uninsured population under the insurance umbrella, resulting in numerous opportunities.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Reinvigoration of Foreign Earnings: Strengthening the Remittance Corridor through Bangladesh’s Diaspora

Remittances are playing an instrumental role in acting as a catalyst for socio-economic development in Bangladesh. At this critical juncture, with a war-torn world economy and our dwindling foreign exchange reserves, increasing our remittances as a major source of foreign currency reserves is more crucial than ever before. As per the data of KNOMAD via the World Bank, Bangladesh received a substantial amount of USD 21.5 billion in 2022, primarily from migrants in the US, UK, Southeast Asia, and the Middle East, making Bangladesh the seventh highest recipient of remittance globally.

Recent times have brought some unexpected challenges, marked by fluctuating migration patterns and remittance figures. Despite a record 1.136 million migrants last year and 618,000 in the first half of this year, the anticipated increase in remittances did not materialise. Emigrants sent USD 2.199 billion, USD 1.973 billion, and USD 1.599 billion in June, July, and August 2023, respectively, followed by a 41-month low in September (USD 1.343 billion).

Factors such as migrant labour composition, recruitment expenses, and reliance on informal channels all contributed to this fall, prompting government intervention and strategic initiatives. Understanding the underlying mechanisms of the unexpected drop in remittance inflows is critical as Bangladesh strives to revitalise its remittance corridor for long-term growth. To ensure a prosperous future for Bangladesh and its diaspora, a concerted effort involving policy innovation, talent enhancement, and technological integration is required.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Steel Industry Of Bangladesh: Constructing A Compact Foundation Of Growth Amidst Economic Instability

Infrastructural development has taken centre stage in Bangladesh in the last decade, with several ongoing mega projects fueling the significant demand for steel. The industry has flourished largely due to the investment of large conglomerates, diversification of steel products, and enhanced production capacity. According to the World Steel Association, the total consumption of steel was approximately 7.4 million metric tonnes in 2022, while the production capacity of steel mills stood at around 9 million metric tonnes in Bangladesh.

The private sector investment brought a significant overhaul to the steel industry in Bangladesh in the early 1990s. Through a resilient growth pace, the current market size of the steel industry in Bangladesh stands at an estimated BDT 55,000 crore (USD 6.2 billion) as per The Business Standard. Moreover, per capita steel consumption is projected to rise from 45kg in 2022 to over 100kg by 2030, indicating a high growth spectrum. Approximately 60% of the manufactured steel is used in government projects, 25% is used by consumers as per The Business Standard, and the rest 15% is reserved for the private sector.

Though having high growth potential, the steel industry, along with its allied industries, has been grappling with challenges in recent times owing to several critical factors like currency devaluation, high inflation, and a high margin on LC opening. This, in turn, has translated to supply chain disruptions, logistical inefficiency, an energy crisis, and a rise in financing costs. However, the easing of the economic slump would dramatically turn the tide in the steel industry’s favour with the usual resumption of mega projects coupled with government policies. Undoubtedly, the steel industry will play a pivotal role in spearheading the industrial infrastructure in Bangladesh and transforming the country’s economic outlook.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Scripting Export Narratives: Leaving A Domestic Paper Trail In Global Markets

Bangladesh is currently in a precarious position due to rising import prices and dwindling foreign currency reserves. Amidst the uncertainties, the paper and paper products industry has emerged as a key source of foreign earnings in recent years, with the sector recording an 85% year-on- year growth during July-August of FY 2023- 24 relative to FY 2022-23.

The market size of paper and paper-allied products is estimated to be BDT 5,000 crore, with the industry comprising diverse paper products, including writing and printing papers, offset papers, newsprints, tissues, and packaging papers. The industry was largely boosted back in 2016, owing to the government’s cash incentive of 10% on receipts. Till now, Bangladesh has been exporting its paper-allied products to over 50 nations, including the United States and countries from Europe, the Middle East, and Africa.

As the world edges closer towards a paperless economy, the demand for writing and printing paper is expected to experience a sharp downfall, while the heavy reliance on paper pulp imports and its scarcity will trigger an increase in the prices of paper products. However, these challenges have been addressed adequately, as paper mills have invested in waste paper processing to reduce reliance on imported raw materials while prioritising product diversification to cater to foreign demands. An excellent opportunity awaits Bangladesh, as the decreased paper manufacturing of China, India and Japan can propel the paper industry to new heights and establish itself as one of the paper manufacturing hubs in the world.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Bridging The Financing Gap For The Marginalised : Microfinance Uplifting Bangladesh’s Social Fabric And Economy

Microfinance has played an instrumental role in enhancing financial inclusion, employment opportunities, and poverty alleviation in Bangladesh. The significant presence of CMSMEs in Bangladesh prompted a rapid rise of microfinance institutions (MFIs) across the country, with 739 MFIs and 23543 branches currently operating under the licence of the Microcredit Regulatory Authority (MRA). During the fiscal year 2021–22, loan disbursements of microfinance reached staggering figures of BDT 226,007 crore, while customer savings stood at BDT 85,036 crore.

The continuous innovation and expansion of microfinance services have facilitated the availability of microcredit and microenterprise loans to the unserved and underserved marginalised community of Bangladesh. The MFIs have flourished in that regard, with annual turnover figures reaching BDT 1.60 trillion while maintaining a near-perfect 98% loan recovery rate, of which 91% of the borrowers are women.

The microfinance sector is met with a fair share of challenges, with high-interest rates and economic shocks largely affecting the financial sustainability of MFIs. Nevertheless, the massive contribution of MFIs towards women’s empowerment, financial inclusion, and poverty reduction has elevated the socio-economic status of Bangladesh and reinforced the belief in the future success of microfinance.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Next Level of Financial Inclusion: Entering The Digital Banking Era

A revolution in the financial services industry of Bangladesh is in the offing with every passing day, with several banks, MFS, and telecom companies gearing up to invest in digital banks through both individual investments and a consortium. The extension of the digital banking application deadline has prompted almost 20% of the traditional banks in Bangladesh to apply for a digital banking licence in a bid to increase their market penetration and bring the unbanked population under the banking umbrella. With an unbanked population of 47% in Bangladesh, digital banks hold the key to enhancing financial inclusion and extending digital banking services to the underserved and unserved population.

The rapid adoption of MFS and internet banking services has laid the groundwork for digital banks to potentially thrive, as evident by the MFS transactions, which registered a year-on-year growth of 19.5% for April 2023 relative to April 2022. The ease of availing MFS services facilitated the financial inclusion of the unbanked demographic, which mostly consisted of low-income households. The unserved and underserved populations were the biggest beneficiaries of such services, owing to convenience, cost and time savings.

Undeniably, the exponential adoption of MFS among low-income households in the last decade serves as evidence for the potential success of digital banking services. These services can effectively replace conventional banking services, which could lead to more competitive rates and reduced operating costs. This, in turn, can help create a conducive business environment for both banked and unbanked communities where digital banks can accelerate financial inclusion and economic growth of Bangladesh with the vision of bringing the majority of the population under a cashless economy.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

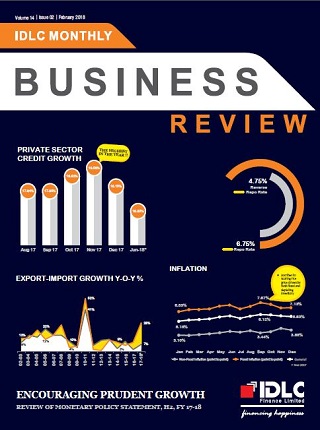

National Budget FY2023–24: Weathering the Economic Storm to Reach Macroeconomic Stability

Economic strife in recent times has led to a downturn in Bangladesh’s GDP growth owing to high inflation, slow growth in the private sector, and minimal growth in remittances. In a bid to reach macroeconomic stability, a national budget of BDT 7,61,785 crore was announced for the fiscal year 2023–24, with the budget comprising 15.2% of the GDP. The GDP growth rate has been targeted to reach 7.5%, while the annual inflation rate is expected to be 6% for FY 2023–24.

Meanwhile, Bangladesh Bank (BB) released a monetary policy statement (MPS) on June 18 with contractionary measures underlining the central bank’s objectives in curbing inflation. Many countries adopted a similar approach, with the United States, India, Thailand, and the European Union successfully managing to curtail their inflation significantly through demand reduction strategies.

As pointed out by economists, restoring macroeconomic stability remains pivotal for Bangladesh to bring some much-needed respite to the economy. Effective approaches to achieving the aforementioned target include the coordination of exchange rate, monetary, and fiscal policies to strengthen exports, curb inflationary pressure, increase tax revenues, and reduce fiscal deficits. With timely measures taken by BB to combat inflation through its contractionary monetary policy, economists and business leaders are hoping that both fiscal and monetary authorities work in tandem to reduce inflation significantly in the country. This will pave the way for Bangladesh to reach macroeconomic stability for future economic prosperity and continue the long journey towards a developed country by 2041.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Shades of Brilliance: A Deep Dive into the Paints & Coatings Industry of Bangladesh

The paints and coatings industry has consistently registered an annual growth rate of 6% owing to significant industrialisation, urbanisation, and economic development in Bangladesh. Synonymous with the beautification of structures, it also plays a crucial role in increasing longevity as well as protecting important infrastructure. As reported by Statista, a leading statistics portal based in Germany, the global market size of the paints and coatings industry was estimated to be USD 160 billion in 2021, and it is forecasted to reach USD 235 billion by 2029.

Generating a yearly revenue of around BDT 7 billion for Bangladesh, the sector currently employs over 100,000 individuals. The industry is largely dominated by multinational companies, with the lion’s share of the USD 471 million market size in Bangladesh, as per a global information source named Coatings World. An increase in per capita income coupled with rising consumption patterns in both urban and rural areas has given this sector a thrust to build on its already promising growth.

Increasing prices of raw materials in international markets and the depreciation of local currency have recently impeded the industry’s upward trajectory to a large extent. Despite the global economic turbulence, the industry can experience a sharp increase in the coming years through infrastructural development and the growing automotive and construction sectors. Certainly, economic recovery can help the industry rebound to its previous levels of growth and grow in stature in the future.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Recycling Industry of Bangladesh: Paving the Path towards a Greener Future

Waste generation has risen to alarming levels in recent years, with the World Bank reporting that the figure is expected to reach almost 3.88 billion metric tonnes by 2050. Population growth, the rapid urbanisation rate, economic expansion, and consumers’ indiscriminate consumption patterns are deemed to be the key reasons behind this ever-increasing waste generation. The state of our environment is a dire concern owing to the existing linear economic system (take-make-waste), and one of the most effective ways to combat this crisis is by championing the cause of recycling.

The rise in purchasing power of people in Bangladesh has led to increased consumption, eventually resulting in large-scale waste generation. Moreover, the informal recycling process is hindering the country’s efficient waste management, preventing Bangladesh from recognising its true potential in the recycling industry. However, adopting a circular economy, the alternative to the linear economic system, through waste elimination and replenishment of natural resources can not only unlock avenues for revenue streams but also pave the way for a greener future.

In a world of limited resources, recycling offers a beacon of hope and a tangible solution to mitigate the damage we have inflicted on our environment. By implementing a proper recycling process, Bangladesh can bolster its economic and environmental landscape by generating employment opportunities, promoting economic growth, and preserving natural resources.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Dairy Industry Of Bangladesh: Where Tradition Meets Innovation

The dairy industry has maintained a strong foothold as a promising sector in Bangladesh. Since the early stages, the industry has undergone massive development, as evident by its enormous market size at present, which is estimated at USD 2.47 billion by the Department of Livestock Services. Despite registering steady growth in the production of milk, the industry is still heavily reliant on importing milk to meet local demands.

In recent years, the industry has integrated modern technologies into dairy farming, with innovation now playing a key role in maximising milk production. Automation in dairy farming has enhanced the collection, processing, and production of milk, leading to economies of scale and minimising costs. Artificial insemination is helping to extract 225% more litres of milk from cow breeds in comparison with traditional farming. Additionally, leading industrial processors are diversifying their product offerings by offering variations of milk derivatives.

Though the industry has several hurdles to overcome, incorporating cutting-edge technologies with traditional practices will promote growth, increase production, and facilitate product diversity to meet changing consumer preferences. As the government aims to be self-sufficient in meeting domestic demand by the year 2030, encouraging innovation will be instrumental in reducing the import gap and boosting the dairy industry.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Breaking the Chains: Financial Independence is the Key to Women’s Empowerment

Financial independence is a crucial aspect of women’s empowerment because it enables women to take charge of their lives and make well-informed choices to build a better future for themselves as well as for their families, society, and the country at large. Research from the McKinsey Global Institute shows that the global GDP could grow by USD 12 trillion by 2025 if gender gaps are closed and women are given more economic power.

Women have been deprived of equal access to opportunities as their male counterparts throughout history. Despite comprising 60% of the workforce in the RMG industry of Bangladesh, the dearth of women at the industry’s management level is leading to gender inequality and poor work culture. The gender pay gap has left women with little savings and investments for the future, making them more exposed to economic instability.

Notwithstanding numerous hurdles, women in Bangladesh have made significant progress in recent years in climbing the corporate ladder and gaining leading positions. They have continually broken through boundaries and challenged societal norms. Bangladesh can pave the road to a more equitable and prosperous future for everybody by recognising the value of women’s contributions to the economy and society and giving them equal chances.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

The Sea's Bounty Awaits: Unlocking Bangladesh's Blue Economy

The blue economy concept has become an exhortation for sustainable development through the utilisation of ocean resources for economic growth, enhanced livelihoods, and employment while conserving the health of the environment. According to the United Nations (UN), the industry is worth between USD 3 and USD 6 trillion globally, with its strong ties to SDG-14 (Life Below Water) serving as a crucial reason for elevating this sector.

With around 710 kilometres of coastline, the blue economy offers numerous opportunities for Bangladesh, particularly in the sectors of fisheries, shipping, tourism, natural resources, and oil and gas. The blue economy has the potential to make a substantial contribution to economic growth and enhance the quality of life for the people residing in Bangladesh’s coastal regions.

Expanding ocean-centric industries will bring a new perspective to our economic prosperity. At the same time, the unplanned proliferation of economic activities will be the cause of marine ecosystem deterioration and biodiversity loss, causing significant harm to low-income coastal residents. Understanding and effectively managing the numerous facets of marine sustainability is crucial to reaping the sea’s bounty.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

Launch of Electric Vehicles in Bangladesh: Hitting the Road to Achieve the Dream of Zero Carbon Footprint

Despite being an integral component of our daily life, transportation accounts for 37% of the world’s carbon dioxide emissions due to its heavy reliance on fossil fuels. However, people are inclined towards electric vehicles (EVs), as reflected in a recent study, which shows EVs account for 8.57% of total automobile sales in 2021 globally, demonstrating the exponential growth potential of the electric vehicle sector.

The electric car industry in Bangladesh is on the rise, as growth of 154% in hybrid car imports from 3,296 units in FY18 to 8,366 units in FY21 has been observed. Increased fuel prices and lower maintenance costs have driven the increase in sales. This adoption has enabled new ventures and start-ups to focus on developing locally manufactured EVs.

Few to no charging hubs, high import duties and misconceptions around the EV currently stand as a roadblock to the bright prospects of this industry. However, it shows promise as the government progresses towards “Vision 2041,” which will enable electric vehicles to run the streets of Bangladesh in full swing.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View

CASHLESS ECONOMY: THE NEXT STEP OF DIGITAL BANGLADESH

Bangladesh is undergoing an unprecedented transformation in the way it conducts its financial transactions. With the rapid digitisation of the economy, cashless transactions are becoming increasingly popular. Recent data from Bangladesh Bank (BB) states that more than BDT 3,000 crore is being transacted through mobile financial services (MFS). Even the use of plastic money has increased exponentially, as is evident by the 24% rise in credit card debt over previous years.

This shift towards cashless or digital payments is driven by several factors, including the government’s goal of becoming a “Digital Bangladesh,” the increasing availability of digital banking services, and the growth of mobile money and e-commerce platforms. The FinTech industry is venturing more and more into cashless payment and transaction integration systems. As a result, the number of cashless transactions in Bangladesh is rapidly growing, and the country is on track to become a leader in digital payments in the region. Nevertheless, some critical issues need to be addressed to transform the country into a cashless economy.

Md. Shah Jalal

Assistant Manager

IDLC Finance Limited

Download View

CERAMICS INDUSTRY IN BANGLADESH: RISING AMIDST CHALLENGES

With a total market value of over 6,000 crores, the ceramics industry in Bangladesh has been one of the country’s fastest-growing manufacturing industries. Thanks to sustained economic growth and increasing urbanisation, the industry meets 85% of domestic demand and has the potential to become the country’s largest export industry in the not-toodistant future. With domestic sales increasing by 20% per year on average, export sales increasing by 26% per year on average in the last three years, and total production capacity increasing by around 200% in the last five years, the industry is poised for future success.

The industry benefits from rising incomes, rapid urbanisation, and duty-free access to some international markets. There is still much to be done to address the problems this industry is facing, such as uninterrupted power and gas supplies, which are essential to continue competing in global markets. If Bangladesh’s ceramics sector can get over the obstacles, it has every chance to develop and increase its contribution to the nation’s foreign exchange earnings. It stands to see what the future holds for this industry.

Md. Shah Jalal

Assistant Manager

IDLC Finance Limited

Download View

Pharmaceutical Industry in Bangladesh: The Next Export Frontier

The pharmaceutical industry, with a market value of more than BDT 275 billion, is one of Bangladesh’s fastest-growing industries, with leading companies like Square Pharmaceuticals Limited, Incepta Pharmaceuticals Limited, Beximco Pharmaceuticals Limited, and Renata Limited.

Download

View

CONSUMER ELECTRONICS INDUSTRY IN BANGLADESH: A SHIFT TOWARDS PERSONALISED EXPERIENCE

With a market value of BDT 20,000 crore, the consumer electronics sector is one of Bangladesh’s fastest-growing industries, with the majority of the product categories entirely import-dependent, although local companies are on the rise.With consumer preference for these foreign brands ever-increasing due to their ability to provide more reliable services, only a handful of local companies are able to cater to these needs. Despite the dependency on foreign brands, increased domestic production sparked a boom, as companies like Walton started exporting thanks to government initiatives. However, some policy contradictions require consistency in implementation. A big success factor of local companies is their ability to embrace innovation through the adoption of technology and integrate existing processes to deliver to customers a greater value proposition through a personalised experience. The result is that customers benefit from brand atomisation, which means relying less on foreign brands as well as greater availability of consumer data flow through various interaction points.With consumers demanding more convenience and innovative technologies, this will be the biggest challenge for local brands’ survival in the days to come, along with rising dollar prices and inflation, as they compete for these features with foreign brands as well.

Md. Shah Jalal

Assistant Manager

IDLC Finance Limited

Download View

FLOUR MILLING INDUSTRY IN BANGLADESH: FLOURISHING THROUGH AUTOMATION

Bangladesh is mainly a rice-consuming country, but flour is the second most important staple food in Bangladesh after rice, meaning flour is a crucial part of our national food security. Hence, flour milling plays a significant role in ensuring food sufficiency in Bangladesh. Though it started with a traditional milling process called “chakki”, now the industry is flourishing through automation.

According to the Bangladesh Bureau of Statistics Household Income and Expenditure Survey (HIES, 2005–2016), daily per capita wheat consumption was 12.08 g in 2005 and 19.83 g in 2016. This growing consumption pattern implies a higher demand for flour in Bangladesh. Moreover, urbanisation, the increasing popularity of fast food, and changing lifestyles have all increased the demand for flour over the years. In recent years, many fast-moving consumer goods (FMCG) companies have started exporting flour-based products, like bakery goods, in addition to serving the domestic market. One of the major challenges faced by the industry is high import dependency. Russia and Ukraine produce 30% of the world’s wheat. These two nations provide 40% of Bangladesh’s wheat imports. Shockingly, the current war between Russia and Ukraine has had a destabilising effect on the country’s wheat supply, causing price volatility and uncertainty. Clearly, the future of wheat and flour milling in Bangladesh depends on trade wars, agriculture policy, and the use of modern technologies.

The flour milling industry in Bangladesh has to become more productive by adopting efficient business models. Most i

Download

View

ISLAMIC FINANCE IN BANGLADESH: EN ROUTE TO NEW HORIZONS

Islamic finance, which adheres to Shariah principles, is one of the thriving segments of the global financial system. A recent report published by Refinitiv, one of the world’s largest providers of financial market data and infrastructure, postulates that the size of the Islamic finance industry is expected to grow from USD 3.37 trillion in 2020 to USD 4.94 trillion in 2025, representing an annual growth rate of 8% on average over the course of the next five years.

Bangladesh is one of the fastest-growing economies in the world. In line with other economic activities, Islamic finance in Bangladesh has also been witnessing robust growth. The country is among the top ten economies holding the highest Islamic financial assets and is growing above the global average growth rate.

Out of the USD 50 billion Islamic finance market, Islamic banking alone possesses a market cap of USD 48 billion, which indicates that the Islamic capital market, the Islamic insurance (Takaful) market and other areas of Islamic finance have not flourished to the extent of Islamic banking expansion in Bangladesh. Nonetheless, the recent issuance of Sukuk (Islamic bond) by both the public and private sectors, the gradual development of the Takaful market (Islamic Insurance), the penetration of Islamic microfinance to the doorsteps of marginalised people, and the advent of Islamic FinTechs indicate that other areas of Islamic finance have a bright future.

Considering the high market demand and growth potential of Islamic finance in Bangladesh, different financial institutions are trying to offer innovative Islamic financial products and services to their clients. Undoubtedly, this growth momentum of Islamic finance indicates that our financial ecosystem is en route to new horizons.

Md. Shah Jalal

Assistant Manager

IDLC Finance Ltd.

Download View

Mobile Phone Manufacturing Industry: Another ‘Made in Bangladesh’ Success Story

The invention of the mobile phone and mobile technology was groundbreaking. One gadget with so many capabilities is transforming the world by placing everything in the palm of our hands.

China, Vietnam, and India are the world’s leading manufacturers of mobile phones. Bangladesh joined those ranks through the hands of local tech giant Walton Group in 2017. Also, world-renowned companies like Samsung, Nokia, Vivo, and Xiaomi have started assembling and manufacturing operations locally in recent years.

Because of the government’s supportive fiscal policy throughout the journey, the mobile phone manufacturing and assembling industry, which began in 2017, is now capable of meeting more than 80% of local market demand. Furthermore, the industry is showing enormous export potential.

Howbeit, the mobile phone manufacturing industry seems to have high growth potential; the industry is facing a branch of challenges, i.e., import dependency for key components of mobile phones, lack of strong R & D facilities, and trading of unofficial handsets, etc. In addition to that, it has been proposed in the budget for the fiscal year 2022–23 to withdraw the existing 5% VAT exemption at the trading stage of mobile phone sets, which will affect the affordability of mobile phones consumers in Bangladesh.

Even after being faced with multiple challenges, it is undeniable that Bangladesh is the 9th largest mobile device market globally. The thriving mobile phone manufacturing industry in Bangladesh has almost all the right things going for it for another “Made in Bangladesh” dream to come true.

Md. Shah Jalal

Assistant Manager

IDLC Finance Ltd.

Download View

EdTech in Bangladesh: A Revolution in the Offing

EdTech in Bangladesh: A Revolution in the Offing

FROM THE EDITOR

In March 2020, the global Coronavirus pandemic resulted in shutdown of classrooms. Teachers and students opted for online classes in order to save academic years for millions of students across the country. EdTech start-ups such as 10 Minute School, Shikho, Shohopathi, which provided online platform for learning, started to thrive from that period of time. Funding in the EdTech industry which was around 0.16 mln in 2018 climbed to around 6 mln in 2022 and 89% of it is foreign funding. According to The Business Standard, 10 Minute School achieved 12 times growth in 2021 with 3.20 mln application users and the amazing part is that, majority of the application users are rural learners. Meanwhile, Shikho which is the country’s largest seed-funded start-up has its paid application users growing by around 140% since its inception. Needless to say, hence, a revolution in the EdTech industry is indeed in the offing. However, factors such as better internet connectivity across the country, greater and cheaper access to hand-held smart devices, more world-class education accreditation for online platforms, etc. should be addressed, to make the growth of this industry sustainable.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

Jute Industry of Bangladesh: Reclaiming the Lost Glory

Jute Industry of Bangladesh: Reclaiming the Lost Glory

FROM THE EDITOR

On March 6th, 2022, the country observed National Jute Day. The Ministry of Textile and Jute celebrated this day with the slogan ‘Sonali Asher Sonar Desh, Paribesh Bandhab Bangladesh’. Although this industry has lost much of its glory off late, as it has been battered by factors such as lack of diversification, inadequate local demand, mismanagement, corruption, etc., jute, which was synonymously referred as ‘the golden fiber’ is still the second export earning sector next to RMG. The sector has an average contribution of 3% in our export earnings and 1% in GDP. The demand for high-tech jute goods across the globe is huge and at times when the world environmentalists are echoing for environmental sustainability, jute can be a potential game-changer for our economy, if the industry can flourish to its potential. The jute industry of Bangladesh will get its glorious days back, if right focus and government support is given to this industry.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

Women in Tech Industry: Gender Equality, the Need of the Hour

We are witnessing an exciting tech-fuelled era which was dreamt of for decades. In times such as these, when the tech industry landscape is rapidly transforming the world, women are still struggling to secure their places in this industry. But, according to various reports, it is evident that diverse companies perform better, hire better talents, have more engaged employees, and retain workers better than companies that do not focus on diversity and inclusion.

Reports suggest that 25% female students studying at tertiary levels in Bangladesh enroll for Computer Science (CS) or Information Communication Technology (ICT), while 13% of them end up joining the ICT industry after completing their graduation in the related subjects.

The lack of women taking up tech-related degrees (STEM subjects) translates into the workforce, where at many tech companies, males form the overwhelming majority. This eventually leads to women experiencing prejudice and feeling like they do not belong. It is time we focus on the next generation of tech talents and make sure gender equality exists for the betterment of everyone. This means more flexible working arrangements, more women in leadership roles and more encouragement at an early age for girls and boys to chase whatever they are naturally interested in.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd

Download View

Supply Chain Finance: Optimizing Financial Flows in Bangladesh

SUPPLY CHAIN FINANCE: Optimizing financial flows in Bangladesh

Supply chain finance is deemed as a win-win opportunity for all stakeholders in the supply chain ecosystem- the corporates, their suppliers and the factor. Rather than waiting on its large customers to pay invoices, the supplier can submit invoices to financiers for early payment. In turn, this provides immediate access to liquidity which can help the supplier keep operating in a “business as usual” environment in any business climate. These along with factors such as proper fund utilization, authenticity of cash flows of borrowers, etc. have garnered much popularity in the country for this particular financing vehicle.

IDLC Finance Limited pioneered and introduced supply chain finance in 1999. Despite its commencement 23 year back, this particular segment of finance is yet to live up to its potential. The clear concept of supply chain finance is still absent among customers in our country. Additionally, the corporate buyers lack interest in supporting their suppliers and as a result, the suppliers end up availing loans at a high rate.

From regulatory point of view, Bangladesh does not have any specific policy guideline or legal framework for supply chain finance. Nor there is any legal framework for the security of the payment for these products. Hence, for this segment to thrive, the driving force needs to come at policy levels. Meanwhile, corporate buyers have to come ahead and support their suppliers by means of reverse factoring.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd

Download View

Startup Ecosystem: Prospects & Way Forward

Startup Ecosystem: Prospects & Way Forward

Growth in traditional drivers such as RMG, Agriculture, etc. along with pragmatic economic policies of the government have catalysed the tremendous growth of startup ecosystem in Bangladesh. Needless to say, 2021 was a year of recovery and progress for startups as Global Pandemic fasttracked technology adoption across various segments and the country got its first ever Unicorn, a Startup which has valuation of more than USD 1 bln, in Bkash.

In 2021, startups had raised USD 166 mln of total fund which was only USD 40 mln in 2020. Like most emerging markets, the growth of this ecosystem in the coming years is expected to be aligned with growth of E-commerce, logistics and payments segments. These sectors along with ridesharing, delivery solutions & consumer services attracted the deserving attention from foreign investors. Health-care, Foodtech and Education sectors also witnessed notable growth. Appreciatively, Bangladesh government also launched its own Startup Bangladesh, which is a USD 11.5 mln fund to support startups. It has already invested around USD 11.1 mln in 50 startups.

Startup Ecosystem in Bangladesh offers lucrative landscape of untapped opportunities. Remarkable growth can still be obtained in this ecosystem, if major segments such as garments, wealth management, insurance, micro financing, etc. can be addressed. Proper infrastructure, process and guidelines tailor-made for the Incubators, Venture Capitals and Angel Networks would encourage more investments. Resultantly, it would pave way for more global investors such as Tiger Global, Sequoia and Softbank, in the years to come.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd

Download View

HOUSING MARKET: RISING CONSTRUCTION MATERIAL PRICES AND ITS IMPACT

HOUSING MARKET: RISING CONSTRUCTION MATERIAL PRICES & ITS IMPACT

For a country such as Bangladesh which is ever growing in terms of population and GDP, meeting housing needs as per demand was always a challenge. In such perilous situation when housing supply was struggling to keep pace with the rapid urban growth, pandemic happened. Now, as the economy crawls back to normalcy amid the coronavirus pandemic, the surging prices of building materials is threatening the country’s housing market.

Cost of almost all the construction materials such as steel, cement, coal, and stone increased significantly owing to factors such as increase of freight charges, hike in fuel price, unavailability of cargo ship, etc. This has led to increase in the construction costs (which comprise of around 50% of any overall project), by around 20% and this upward trend of cost is expected to sustain till mid-2022. The cost of mega construction projects undertaken by the government such as Padma Bridge and Elenga Road Project has increased multiple folds due to surging material prices. It has also left many developers unsure about their future residential and commercial projects. Contractors of development projects are now hesitant to bid for their new projects and are demanding price adjustments for their ongoing projects.

The housing market, however, is in its phase of rebound, thanks to certain government policies such as lower interest rates cap for banks, reduction of registration fees, etc. Along with this, recovery of the overall economy will surely make this industry come back strongly.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

LIGHT ENGINEERING INDUSTRY: FORGING THE PATH FOR A BETTER ECONOMY

Light Engineering Industry: Forging the Path for a Better Economy

Bangladesh is witnessing promising growth of Light Engineering Industry (LEI) which has contributed 2% of overall GDP and has the potential to further boost the country’s overall export diversity. Our country has become a major player in the global apparels industry but export performance of Light Engineering Industry (LEI) has decreased by 14% in 2019-20 in comparison to the previous year. However, the government has taken some initiatives like deciding to set up 10 dedicated light engineering parks which will surely help this sector rebound in terms of export performance.

This industry which provides backward linkage of raw material support to almost all manufacturing sectors, continues to grow each year and produces a diverse range of products. Initially, light engineering enterprises emerged from the Dholaikhal and Jinjira areas in Dhaka. However, with time, different types of light engineering enterprises have spread all across the country.

Despite being an important sector in the country, the LEI continues to face a plethora of challenges including shortage of workers, lack of quality raw materials, modern technologies, access to finance, industrial facilities and policy support, etc. The LEI can help poverty alleviation by generating employment and increasing contribution to the GDP. Therefore, timely implementation and review of government policies for this sector should be carried out to help this sector overcome its major obstacles and grow to its optimum level.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

COMMERCIAL VEHICLE : ROLLING THE WHEELS OF ECONOMIC GROWTH

Commercial Vehicle Industry: Rolling the Wheels of Economic Growth

With the expansion of the manufacturing sector in our country, the demand for the commercial vehicles is on the rise than ever. Manufacturers of various goods and logistics companies are the end customers of commercial vehicles, as they require transportations to deliver goods to various points all over the country. Due to the countrywide shutdown, the industry suffered from negative growth for the first time in the last few years. However, the pandemic-stricken economy is reviving in tandem with the recovery of the commercial vehicle industry.

GDP of Bangladesh is projected to reach 340 billion USD in 2022. Keeping pace with that, the commercial vehicle industry is expanding by 15% to 20% every year. Fast track projects undertaken by the government to develop the roads and highways of the country are helping to sustain the growth. Technological advancements have touched this sector as well like many other sectors. Resultantly, technologies like GPS and smartphone apps like Truck Lagbe, GIM, Loop Freight etc. have already become widely available to city dwellers and have positively impacted the industry.

Needless to say that the success of trade and commerce of a country largely depends on its well-structured transportation system. Keeping that in mind, the government in collaboration with foreign investors is patronizing local assembly with the goal to manufacture commercial vehicles with locally sourced materials.

Like every other industry, this industry is also going through some major challenges. Congested traffic, unsafe roads, poorly trained drivers, high import duty etc. are some of major challenges that must be mentioned. Government initiative to formulate industry-friendly policies and proper implementation of them is highly required to help this potential industry flourish.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

The Local Textile Industry of Bangladesh: A Signature of Our Culture

The Local Textile Industry of Bangladesh: A Signature of Our Culture

Clothing is one of the basic needs of human life for survival that comes after food but it is more than an essential requirement as it represents the uniqueness

and identity of a nation. We have represented our heritage in the global stage through Jamdani and Moslin. With passage of time, our concentration moved

towards the RMG and we, through leveraging our competitive advantage of low cost production, have secured the third position in the world.

Although it is very common to associate the RMG sector with local textile industry, RMG is different from local textile. RMG sector is engaged in manufacturing

export oriented products while the local textile holds the aim to serve the native demand.

The local textile has to go through five distinctive steps to produce the finished goods. The process starts from import of cotton, and then we move to spinning which means the production of yarn. After producing yarn we move to the next step and it is weaving where grey fabrics are produced. Then we move to the fourth step where grey fabrics move into dyeing and printing factories and finally, we step into the final stair and it is the finished goods.

The size of local textile industry is immense and its market size is of USD 7 billion dollar. Although there is a trend of duplicating the design of neighboring

countries but our local brands, for example: Yellow, Sailor, Aarong, etc. are promising and we hope that in the near future we will cater our domestic market with own distinctiveness.

Nothing is beyond challenges and limitations, and our local textile industry also has certain challenges which range from scarcity of investment to reform of existing policies. Yet, we can see a prospective future of this sector, and proper nurture of this segment will let us set our footprint in abroad as well, after fulfilling the domestic demand.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd.

Download View

BANGLADESH GOING GREEN: GREEN BUILDING & LEED CERTIFICATION FOR ENSURING SUSTAINABILITY AND SAFETY

Green Building and LEED Certification: One of the many attempts to ensure sustainability in Bangladesh.

The spiraling concern for saving the environment and its resources has led many platforms to opt for the green building strategy, which takes into account

the environmental factors and efficient distribution of limited resources. Bangladesh has also stepped up in the initiative of Green building strategy, and at present Plummy Fashions, of Bangladesh, is thegreenest knit apparel factory in the world awarded by USGBC ( U.S. Green Building Council). Amongst the

numerous Green Building rating systems available, LEED certification is the most widely used rating system worldwide, as well as in Bangladesh.

Leadership in Energy and Environmental Design (LEED) has 110 credits in total, and consists of 4 levels of certification for industries, offices, retails, residential, and other building projects. LEED Certified buildings are on the rise globally, with the USA occupying the leading position in terms of projects and space. The LEED Certification process consists of four simple steps, starting with registering for a project online through their website.

Within a short time, the number of LEED-certified projects has risen above 160 in Bangladesh, this has led multiple banks and NBFIs, including Bangladesh

Bank, to come up with several financing schemes to help finance the green construction projects. Besides these, Green Transformation Fund and SREUP Financing Scheme (Program to Support Safety Retrofits and Environmental Upgrades in the Bangladeshi Ready-Made Garments Sector) have also come up with initiatives, specific to the RMG industry, to finance green building. Thus, these initiatives have allowed many clients to benefit from the low-cost funds.

With the availability of more funding options and awareness, there can be an upsurge in the number of green building projects in Bangladesh. With climate

change being one of the most heated issues in the contemporary world, it is time to train more experts in this field so that the new generation of professionals will understand the significance of the issue.

Bonnishikha Chowdhury

Executive Officer

IDLC Finance Limited

Download View

HEALTH-TECH IN BANGLADESH: ENSURING HEALTH CARE SERVICES AMIDST THE PANDEMIC

Health-tech in Bangladesh: Safeguarding the country’s health care sector with constant improvement

With the vision of Digital Bangladesh, the nation has set its foot on the path of digitization. Last year when the entire country saw an influx of Covid-19 cases, e-health allowed healthcare to reach the households of Bangladesh allowing patients to receive quality health services in the palm of their hands by ensuring

safety measures. Initiatives were taken in the past to establish e-health services in Bangladesh, however, due to lack of technological advancement imperceptible advancement were made. At present with a significant amount of the population having access to mobile phones and the internet has made the availability of e-health services feasible.

Exploiting the blessing of artificial intelligence several new health-tech platforms have emerged in Bangladesh. These platforms are not only standing by the side of the Covid-19 affected patients but also with patients who are afraid of visiting doctors for other health-related issues during the pandemic. Starting from helping patients with mental health issues, to connecting patients with their desired doctors who can provide them with online consultations, to providing medicines at the patients’ doorsteps and providing pharmacies in remote areas with the required medical supplies, to providing diagnostic test services at home, all of these have been successfully implemented in Bangladesh, by the youth over the past few years.

The government has not been sitting behind in exploiting technology for health care, countless approaches were initiated by the government in order to reach out to the patients. Online portals have been established to keep the people updated with the latest Covid news, chatbots are delivering health services by extracting information from health experts of renowned organizations. Awareness is being spread to each citizen by the means of social media. Similar approaches like Bangladesh have also been taken by our neighbors India, Pakistan, and Nepal. While the city dwellers are benefitting from all the advancements, the rural poor are still being a victim of the digital divide. Even though several approaches have been initiated in the rural areas, they still have a long way to go.

As Bangladesh is still on its way towards digital Bangladesh, countless bridges need to be constructed in order to fill in the gap in the fractured healthcare

system. According to experts, the emerging e-health platform provides a path for the socio-economic development of the country. Hence, with proper utilization of resources, the country will be able to level up the health care sector, especially in the rural areas.

Bonnishikha Chowdhury

Executive Officer

IDLC Finance Limited

Download View

REAL ESTATE SECTOR OF BANGLADESH: COVID 19 AND ITS AFTERMATH

Real estate sector: Thriving against all odds since its inception

The real estate sector of Bangladesh started its journey in the 1970s, with the concept of developing apartments, and has been climbing up the ladder ever since. At present, developing apartments has stretched to model cities, shopping malls, and commercial set-ups making the sector one of the key drivers of economic growth. The sector has managed to make a sizable impact in employment generation and directly adds on average nearly BDT 5.0 million to government revenue per annum.

The spiraling growth in population has made Dhaka and Chittagong into two of the most populous metropolitan cities in Bangladesh, for which they attract most of the projects. Bangladesh Bank estimates the housing finance demand for the fiscal year 2020-21 to rise compared to that of the previous year, with private banks holding the lions share in outstanding housing loans as of end of June 2020. The nationwide lockdown last year, acted as an obstacle to the growth of this sector, from which it is gradually recovering because of the enormous support from the government. Moreover, high liquidity which drove the lower interest rate in the banking sector also played a vital role here.

Many doors have opened for the booming real estate sector, for example, the development of new and spacious areas outside of Dhaka which calls for urban infrastructures in order to develop.The construction of new roads and railways will provide them with an opportunity to consider regions apart from the mainstream ones. The increasing rate of lower-middle-class people has led to a rise in demand for their homes. In addition to that as mentioned above support from the government, banks and NBFIs are also contributing immensely.

Unfortunately, the pandemic is not the only hurdle faced by the real estate. Mismanagement caused by few developers sometimes result in customer dissatisfaction. Minimal coordination between development authorities and disorganized urban planning exacerbates the situation. As a result, joint efforts from the government and industry players

are required to cater to the needs of the people. In addition, real estate should start stressing over lowcost affordable housing in order to accommodate the influx of lower-middle-income families.

Bonnishikha Chowdhury

Executive Officer

IDLC Finance Limited

Download View

Venture Capital and Start-Up Financing: Prospects in Bangladesh

Investing in innovation: Venture Capital and Start-Up Financing in Bangladesh

Bangladesh is enriched with all the features to be recognized as a great macroeconomic story. However, we are yet to utilize our story compellingly. If we consider our regional peers, we will observe that they have carefully nurtured their startup ecosystem to the point that they are reaping the benefits now and writing success stories like Gojek, Tokopedia, Meesho, CRED, and so on.

In Bangladesh, banks can specifically finance a new business to the extent that there are collaterals against which the debt can be secured but in today’s information-based economy most of the startups do not have collateral. Thus, Venture Capital (VC) exists to the rescue. The main idea of VC is to invest in a startup’s growth until it reaches a sufficient size and credibility so that it can be sold to a corporation, or institutional public-equity markets can step in and provide liquidity.

Bangladesh’s startup ecosystem has shown great breakthrough over the past decade, companies such as Bkash, Chaldal, Pathao, Shohoj, and Bdjobs are some prominent names who ventured into this space earlier in the decade. Moreover, during the pandemic, the startups of Bangladesh have stepped with their technology-enabled solution, and have solved multivariate problems.

Currently, the ecosystem is seeing an increasing number of startup-ups but not enough funding available locally. Fundraising in Bangladesh has always been relatively tough for the aspiring founders in the early stages even with considerable traction and proof of concepts.

Appreciatively, this is where the ecosystem got attention from foreign investors and the acceleration took place in specific sectors such as ridesharing, e-commerce, delivery solutions, consumer services, and payments. However, the government of Bangladesh also initiated its own public startup support wing, Startup Bangladesh with a 100 crore BDT (U$ 11.5Mn) fund to catalyze investments. To supercharge the startup ecosystem, they have conducted multiple competitions and boot camps as well. Startup Bangladesh has been actively investing in the ecosystem with 100+ startups receiving seed funds over U$ 1.5Mn+ over the past few years.

Mutual cooperation among different stakeholders is the ultimate way forward for the further development of this ecosystem. Entrepreneurs need to come up with innovative solutions to solve real problems with large market addressable markets. On the other hand, local angel investors and institutional investors also need to understand deeply how does a startup operate in order to achieve its goal of winning the market but not profitability. Finally, working closely with the government is essential in order to unlock foreign venture funds.

Bonnishikha Chowdhury

Executive Officer

IDLC Finance Limited

Download View

MUTUAL FUND: A GLOBALLY POPULAR INVESTMENT VEHICLE YET TO HAVE A STRONG FOOTHOLD IN BANGLADESH

Mutual Fund: Potential to be popular household financial instrument in Bangladesh

Mutual fund is most preferred by the investors worldwide not only because of its higher return yielding nature compared to other household assets but also because it assists the investors by offering professional fund management service with the benefit of diversification and lower investment cost. Even though mutual fund was first introduced in 1980s in Bangladesh, the industry growth has not been very noteworthy.

In developed countries, the size of the industry in terms of Asset under Management (AuM) has sometimes become even larger than the economy itself. The largest mutual fund industry in the world belongs to United States of America (USA). As of 2019, 12.9% of the household financial assets are invested in mutual funds in USA. Among Asian countries, Malaysia (54.0%), Japan (40.6%), and South Korea (34.6%) have been successful in building a sizeable mutual fund industry compared to their economy. The southern part of the region is still struggling. However, India (14.2%) in this regard showed tremendous progress compared to its regional peers like Pakistan (1.5%), Sri Lanka (1.3%) and Bangladesh (0.5%). If the factors behind the tremendous progress of India considered, it can be observed that initiatives such as government incentive, systematic investment plan, product variety, Presence of a structured and active association etc. played a vital role.

On the other hand, this industry of Bangladesh is yet to boom. Innovative and prudent strategies from asset managers along with policy support can take this industry to a new height.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

RESILIENT TURN AROUND OF SMES FROM THE ADVERSE IMPACT OF COVID-19

Recovery of the SME Sector: An Essential for Ensuring Economy’s Overall Survival

Like in most other nations, the outbreak of the COVID-19 pandemic was unprecedented and shook the Bangladeshi economy. One of Bangladesh’s most prominent industries, the fisheries and livestock industry, employing about 70% of the individuals in the rural areas was struck hard. The dairy farmers also lost around BDT 189 million daily during the lockdown. The disruption of activities in the transportation industry, broke down the supply chain of the construction industry as shipments were delayed. Traders could not operate for two months, causing the price of construction materials fell significantly. Similarly, the fixtures and furniture industry, which employs the second highest number of workers in the country after the RMG industry, lost 70% of its business due to the pandemic, causing 0.60 million worker to be laid off. The non-allopathic or alternative medicine industry on the other hand is one of the few industries to make profit from the pandemic as people turned to Ayurvedic products, Naturopathy and Yoga to boost their immunity. At the same time the demand for Homeopathy medicine saw a sharp rise as people visited Homeopathic practitioners to treat any symptom related to COVID-19.

On the other hand, disruption of activities in the food and food processing industry, resulted in decreased sales for super shops and local vendors, while online sales saw a huge surge. At the same time the price of important staples rose by 15-20%. The local textiles industry faced losses due to an increase in price of raw materials. The light engineering sector, like most other sector also suffered a huge loss as 90% of the workshops were forced to shut down. The situation improved for most business once the lockdown was lifted, with many business recording higher profits than the previous years. The government’s stimulus package worth BDT 5000 crore also fastened the recovery process.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

RICE MILL INDUSTRY OF BANGLADESH: PRESENT MARKET SCENERIO AND FUTURE PROSPECTS

The Rice Mill Industry of Bangladesh: Surviving throughout pandemic and bringing technological change

Corona virus has affected almost every spheres of life in the world including different businesses and industries where agricultural sector is not an exception. Rice is the most vital element of this agricultural sector. The average per capita rice consumption in Bangladesh stood at around 179.9 kg per year from 2016 to 2019, more than three times the world average. According to the USDA, approximately 500 million tons of rice were produced globally during 2019-2020. Bangladesh ranked fourth, contributing about 7% to the world production. Despite being one of the leading producers, Bangladesh cannot find a place among the top five rice exporters since its output is used to meet the domestic demand. Our domestic demand

has almost tripled since independence, causing us to somewhat dependent on imports to meet the demand.

Due to technological advancement and changing demands, the rice milling sector in Bangladesh has slowly shifted from the traditional “Dheki” or husking method of processing paddy to a more automated process. More than 12,000 husking mills had to shut down between 2012 and 2014 as they could not compete with the auto and semi-auto rice mills. Currently, 18700 public and private rice mills operate in Bangladesh, mostly in the North Bengal region. These mills broadly produce three categories of rice- Aus, Aman and Boro.

Since rice is a non-cyclical product, its demand is relatively inelastic. As such, the pandemic did not have much effect on the sector. Although the producers faced a temporary cash crisis during March and April due to the lockdown and limited banking hours, the situation improved from May and onwards. Handsome production and suitable government policies helped the producers to avoid any difficulty during the pandemic. Sales increased as people hoarded rice due to uncertainty, and different organizations procured rice for relief distribution. As a result, during the third quarter of 2020, the price of rice increased by BDT 5-7 per kg.

As technology advances, we need to use more modern technologies such as drones and field sensors in our farming process and adopt Climate Smart Agriculture (CSA) to boost our productivity. These need to be implemented almost immediately as we lose 1% of our cultivable land every year due to growing population demands. The government should also ensure proper financing and insurance facilities for the producers. Doing these will decrease our dependency on the RMG industry as our sole exporter and allow this industry to be a potential source of our export income.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

Impact of Covid-19 Pandemic on the Coastal Shipping Industry of Bangladesh

The Costal Shipping and Cement Industry of Bangladesh: Recovering from the Pandemic Wave

The cement industry of Bangladesh has beenrecognized as one of the fastest growing cement markets worldwide, with a double digit growth rate over the last decade, and an annual demand of around 33 million tonnes. This is owing to the construction of mega projects undertaken, and the constant infrastructural development on way to further develop the nation. Yet Bangladesh remains as one of the least cement consuming nations in the world

topped by China, India, Myanmar etc. The deadly wave of the Coronavirus, followed by lockdowns has had an adverse impact on an industry that employs over 10,60,000 people directly and indirectly. Disrupted supply chains, halted projects, and fluctuating exchange rates have made it challenging for cement manufacturers and exporters to maintain a smooth business flow as companies incurred losses and capacity remained underutilized. However, investors remain hopeful of the future as they approve fund to enhance the cement production capacity of Bangladesh.

As we speak of exports and imports, a crucial industry comes into focus – the Coastal Shipping industry of Bangladesh, which not only assists trade but plays a vital role in the inland waterway transport system. Lightering vessels,in particular, have played an important role in assuring safe offloading process from Mother Ships as ports in Bangladesh are not deep enough for many international ships to navigate through. Necessary lockdowns, to contain the virus, have forced trade levels down, allowing only drugs and other essential commodities to be traded. This put lightering vessel companies in a state of despair as they struggled to cover their overheads with minimal business activity. However, as lockdowns slowly recede and several mega projects start construction,the industry is showing promising growth prospects.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

Feed Industry of Bangladesh: Sustaining Covid-19 and Potentials in Upcoming Days

Feed Industry of the country: Surviving the Outbreak of COVID-19

The agricultural industry of Bangladesh remains of pivotal importance, contributing 13.35% to the GDP of the country. Out of this, 4.95% is contributed by poultries and fisheries, which would not have been possible without proper nutrition provided by the feed mills. This establishes the far-reaching importance that feed mills hold in ensuring quality output from the agricultural sector. Globally, the feed industry generates about US $400 billion from compound annual feed production of 1 billion tonnes. Over 130 countries are involved in the production process or sale of feed which generates employment opportunities for many.

In an obvious attempt to contain the virus, governments all over the world, introduced lockdowns, limitations on travel and business opening hours. All of these has had an unnerving impact on the feed industry alongside many others. Lockdowns and logistical blockages have created movement restrictions, halting business activity. And no just that, even rumors concerning the spread of coronavirus through poultry and other meat consumption has had a significant impact on the industry’s turnover. Supply chain disruptions leading to a loss in dairy and meat products have affected the feed market as well. Disruptions in the supply chain created wastage despite high demand in the markets, and trade halts have stopped raw materials from coming into the country which had severely impacted the feed mills industry and its stakeholders.

However, lockdowns have given a lot of people time to reflect on many decisions and directed them towards taking healthier steps, for instance. The increased consumption of meat, alongside growing awareness about livestock nutrition has led to an expansion of the market size of feed and feed additives globally. In Bangladesh, commercial feed production experienced a near 25% growth over the last decade. A number of feed mills were established to meet the upsurge in feed demand and the local market expanded subsequently, with poultry feed holding the most market share, followed by fish feed and then cattle feed.

With the world slowly stabilizing after the impact of the pandemic, the only hope is to look ahead into the future towards a prosperous local and global feed industry, and a safer and healthier world.

Sushmita Saha

Assistant Manager

IDLC Finance Ltd.

Download View

STEEL & RE-ROLLING INDUSTRY OF BANGLADESH: STRENGTHENING COUNTRY’S INFRASTRUCTURAL DEVELOPMENT

Steel and Re-Rolling industry: fast paced recovery from pandemic on the cards

The Steel and Re-rolling industry, one of the prominent growth drivers of Bangladesh, has had its fair share of hit by the Covid-19 pandemic. This has been reflected on numbers as world crude steel production recorded a 3.2% decline compared to figures recorded in the same time period last year. As a developing nation with increased focus on to infrastructural development and lined up mega projects, Bangladesh sees massive growth potential in the Steel industry. With a market size of around BDT 450 billion the local Steel market employs nearly 1 (one) million people directly or indirectly across the country. The market has been growing at a rate of 15%- 20% for the past 2 years and contributes largely to the country’s GDP. However, the market for steel is turning into a perfectly competitive one from an oligopolistic structure as small players are now gaining efficiency and reaching competitive levels of their larger peers such as AKS, BSRM, KSRM etc. With the growth of the smaller companies, it is safe to say that the challenges that come with surviving in the Steel industry – such as, abundant supply of power and gas, availability of raw materials etc. are being well taken care of.

The Steel industry strategically runs on overcapacity. It is seen that the utilization is around 75% of total capacity which came down to 40% due to the pandemic wave. The prices of raw materials and finished goods are also seen to fall. However, as a resilient nation, Bangladesh is adapting fast to the new challenges that came with the pandemic. And, as we look towards a new normal, companies in the Steel industry must work in collaboration with regulators in order to sustain the growth and maintain the level of efficiency reached prior to the pandemic.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

DELIVERY SERVICES AMIDST PANDEMIC : SAFEGUARDING CONSUMER DEMAND

Delivery Service to the rescue for consumer demand in a pandemic-driven world

A global event as prominent as the COVID-19 outbreak is likely to have an impact on the life style of people all over the world. Thus, a sudden change in consumer behavior is not surprising, rather rational. However, the success of a business depends on how fast and efficiently it can cope up with any unfavorable situation as risk is a fundamental element of any business. Before pandemic, the biggest vertical to deliver for logistic service providers of the country was e-commerce and f-commerce, covering around 60% of the whole pie which mostly consisted luxury products. After the corona virus outbreak, in no time the demand for grocery and essentials reached sky-rocket. The market leader, Chaldal was receiving 16,000 orders per day which was only 2,500 before pandemic. On the other hand, food delivery services dropped by 80% since all the restaurants were closed. However, when the whole country was staying inside home in order to minimize Covid-19 contamination, the logistics service providers were serving day and night to cater the sudden shift of the consumer demand. They responded to the situation swiftly by either extending their verticals or shifting their concentration to adjust the shift in market dynamics. As we are moving on with this new normal arrangements, the booming sectors must capitalize on this opening at once and focus on practices like consumer retention, that will make this growth more sustainable. On the other hand, a post COVID-19 boom for the verticals which are lagging behind, seems to be on the cards.

Sushmita Saha

Assistant Manager

IDLC Finance Limited

Download View

MICROFINANCE SECTOR OF BANGLADESH : IMPACT OF COVID-19 PANDEMIC AND POST PANDEMIC PROSPECTS

Assistant Manager

IDLC Finance Limited

Download View

B2C MODEL IN RMG SECTOR OF BANGLADESH: LEVERAGING THE GLOBAL E-COMMERCE PLATFORMS TO DIRECTLY SELL BANGLADESHI PRODUCTS TO END USERS

From “Made in Bangladesh” to “Brand of Bangladesh”: Global E-commerce Platform may Open up New Horizon of Opportunities for Local RMG Manufacturers

It has been 40 years since we are serving the global big brands with our products and designs with pride. However, we are still stuck in the back of the labels or tags and it is high time to level up our game and reach the consumers as a brand. The traditional B2B model may be convenient in many ways but after the Covid-19 break out, it showed us how largely it made us buyer centric. When buyers default, it directly hits our largest export earning sector which is apparently the earning source of 4.5 million people of the country. As of April 2020, global brands and retailers, who purchase clothing goods from Bangladesh, have cancelled & suspended work orders worth $3.18 billion, which directly affected around 2.28 million workers and the dependents of their income. In this circumstances, B2C can be the perfect contingency plan for us to come out of the shadow of the buyers and establish our own market.