Monetary Policy Statement 2019-20

Bangladesh bank has changed the monetary policy for the current fiscal year and this has been a big adjustment to the monetary programme for the current fiscal year. This has led to an increase in the public sector credit growth target to 37.7% but keeping the private sector credit growth target unchanged. Prior to this revised policy, the central bank had set the target of credit to private sector at 14.80% for the current 2019-20 fiscal year. This amendment in the policy by Bangladesh bank has circulation target from 12.5% to 13%. According to Bangladesh bank this has been done to boost the stock market and credit in private sector. The two key monetary policy inflation and targeted real GDP growth were achieved in FY19. In 2019 CPI inflation was at 5.47% which was below the targeted 5.60% ceiling, and real GDP growth of 8.13% which was higher than the targeted rate of 7.80%.

The revised monetary program for FY20 has caused a growth in the public sector borrowing from 24.3 per cent in the original monetary program to 37.7 per cent in the adjusted monetary program. Hence it has been reported that public sector bank borrowing this fiscal year reached Tk 51,740 crore as on January 9, 2020. This constituted 37.8 per cent growth relative to the stock of public sector debt to the banking system as on June 30, 2019 which is larger than the total increase in public sector borrowing implied by the revised 37.7 per cent growth target. Fiscal adjustments is important to enable financing of government spending only from revenues and external sources. The increase in government borrowing can create pressure on interest rates and inflation and the risk of increasing inflation is even greater if the increased borrowing is from the BB.

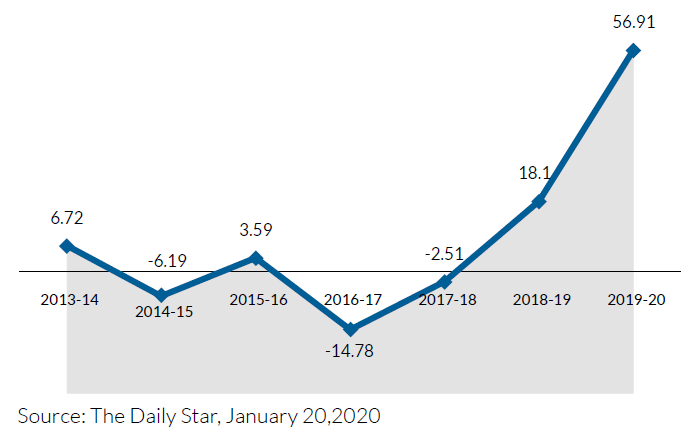

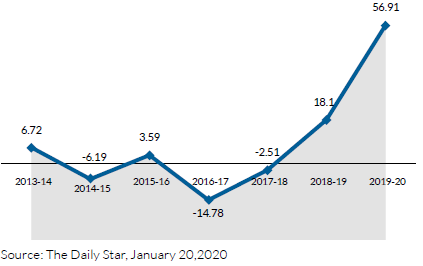

Public sector credit growth over the years

During 2019 the increased public borrowing from banks may have shrunk money available for credit to the private sector. This, along with incidence of NPLs and high rate of interest has deteriorated the rate of increase in private sector investment at the rate of 23.54 per cent during 2019. This has also constituted to the decline in private sector credit growth from 16.9 per cent in 2017-18 to 11.3 per cent in 2018-19.

It is evident that highest level of public borrowing previously was Tk 23,300 crore in fiscal 2010-11 and the next highest was Tk 22,500 crore last year. The large increases in bank borrowing last year as well as this year, clearly highlights rapid increase in domestic public debt and this public debt can have a great impact on the economic growth. Although the short-term, aggregate output can be boosted, but in the long-run, investment is reduced, thus reducing the economic growth. However there is another view which holds that the investment and economic growth are not affected because the private sector responds appropriately to make sure that the future generations do not have to bear any unreasonable burden of public debt.

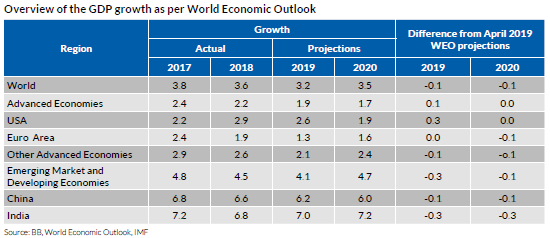

The World Bank has projected 7.2 per cent GDP growth for Bangladesh in the current fiscal year, FY 2019-20, while 7.3 per cent in the following fiscal year.

Bangladesh, the third-largest economy in the region, fared better than India and Pakistan, with the growth officially estimated at 8.1 per cent in FY2018-19, said the World Bank in its Global Economic Prospects.

It has been reported that Bangladesh Bank has implemented its monetary policy statement (MPS) for FY2019-20 with the hope to achieve the 8.2 per cent GDP growth keeping the inflation rate within 5.50 per cent.

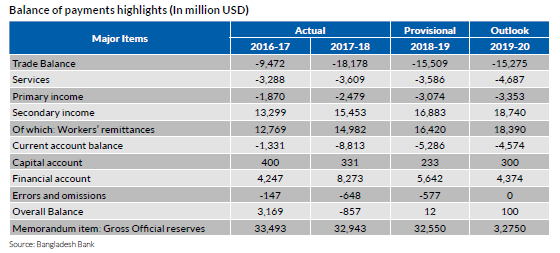

However, significant improvement in Balance of payment was also visible.

Monetary policy stance and monetary program for FY20

The monetary policy stance and monetary program for FY20 have been implemented with the objective of maintaining price stability and aiming for sustainable growth and development. The FY20 monetary program is based on the 8.2 percent real GDP growth and 5.5 percent CPI inflation. Bangladesh bank’s annual monetary program provide adequate opportunities for money and credit growth with aim of attaining the targeted nominal GDP growth.

Bangladesh bank is adopting a policy interest rate that is focused on monetary policy regime in which changes in policy interest rates will have cause a direct impact on the prices in the financial sectors. If this is properly implemented it will likely to result in increased efficiency in transmission of intentions of monetary policy.

Potential risk factors for attaining FY20 monetary program objectives

The domestic risk factor, the ongoing trade wars, geopolitical tensions and other uncertainties may fully or partly impair the attainment of FY20 monetary program objectives and outcomes.

Development of the Bond Market – A Pressing Need for this Growing Economy

“Bangladesh booms in a sluggish world economy, while economies slow for its South Asian neighbors; Bangladesh is hitting record growth rates”, is the statement of *The Diplomat on the accelerating growth of our economy. However, the wheel of growth will be continuously running only if it is fueled by continuous funding.

The financial sector of Bangladesh is mostly bank dependent but the appetite for fund is not always same under all the circumstances. In order to maintain stability in the economy, it is important to ensure the presence of both long and short term sources of funds. The global infrastructure outlook estimates that, currently we have an investment gap of $192 billion*. Considering the running mega projects and upcoming long term projects, long term nature of bonds investments with flexible structuring mechanisms & repayment structures might be the best fit to cater the capital expansions. Moreover, it is never a good idea to be largely dependent on banks since there are always risks of liquidity and mismatch. However, if countries with stable economies are considered, it can be seen that corporate bonds act as one of the most stable source of financing for the public sector, for example corporate bond market to GDP ratio is 150% in USA, 60% in China and 60% in Malaysia*. On the other hand, our government bonds outstanding would be worth about $17.2 Billion whereas corporate bonds outstanding is only $0.3 Billion*. Unfavorable policy support can be attributed for such lack of interest in this sector but absence of secondary market also plays a vital role too. A well-established bond market is not only beneficial for issuers and investors but also spreads investment risks across investors and intermediaries. Therefore, for a rapidly growing economy like ours, investment growth can play a crucial role.

* https://thediplomat.com

* https://outlook.gihub.org/countries/Bangladesh

* https://www.thedailystar.net

* https://www.adb.org/publications/asia-bond-monitor-november-2019