Empowering the SMEs: The Instrumental Role of Lenders in Bridging the Financing Gap

Akhlaqur Rahman Sachee

There was a time when formal lenders such as banks and non-bank financial institutions (NBFIs) were not willing to lend to cottage, micro, small, and medium enterprises (CMSMEs). The CMSMEs had to rely on self-arranged funds or informal lenders. However, the scenario has changed a lot since targets for loan disbursement for CMSMEs were set for banks and NBFIs in 2010. Many banks and NBFIs now have a special focus on the CMSME sector, and the changed scenario has enabled CMSMEs to access much-needed finance from formal lenders. As per a report published by the United Nations in October 2023, the CMSME sector contributes 25% of the country’s gross domestic product (GDP). As per the latest economic census published by the Bangladesh Bureau of Statistics in 2013, there were 7.82 million enterprises in the CMSME sector. As of 2013, the enterprises in the CMSME sector generated employment for 24.50 million people.

Formal lenders in SME financing

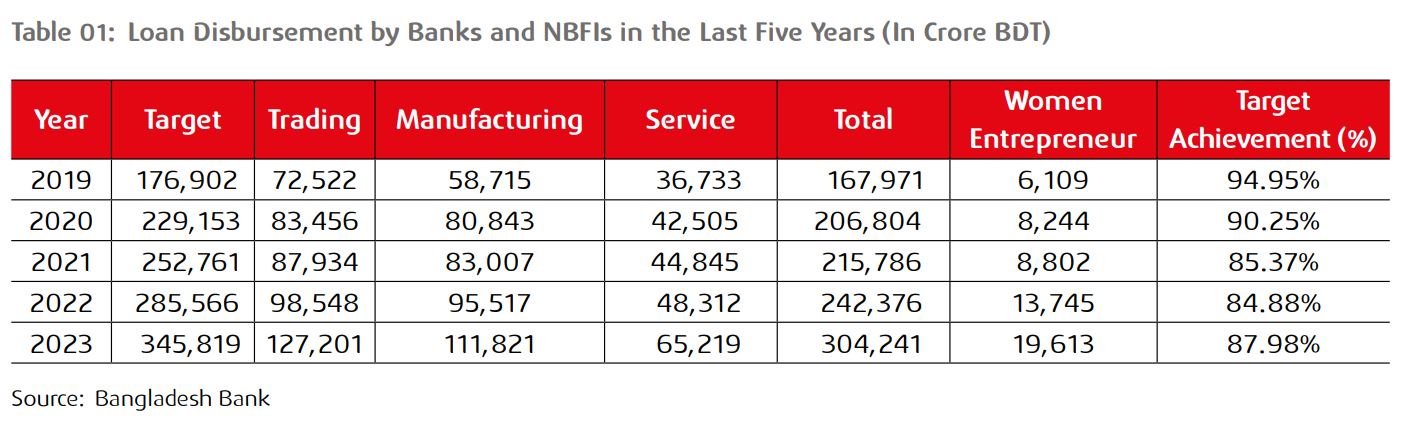

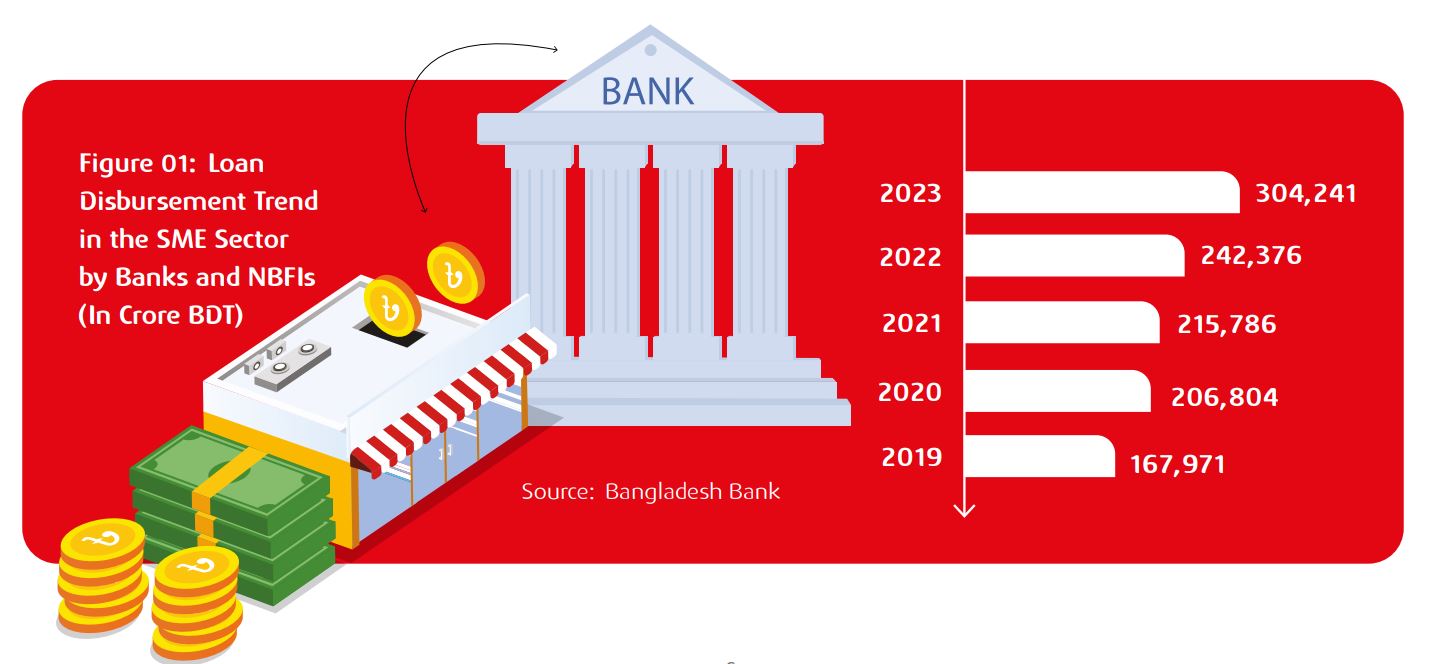

As per the central bank data, loan disbursement in the CMSME sector amounted to BDT 224,103.87 crore in FY2022-23. In the October 2023–December 2023 quarter, 369,016 enterprises were financed, and the total disbursement amounted to BDT 64,841.99 crore. By the end of December 2023, total outstanding in the CMSME sector stood at BDT 304,241.45 crore, which experienced 7.55% year-on-year growth from the outstanding by the end of December 2022, which amounted to BDT 282,896.54 crore. However, one of the biggest challenges in financing SMEs is a lack of collateral, which formal lenders are attempting to address. The central bank data demonstrates that 121,017 out of the 369,016 enterprises were financed without collateral in the October 2023–December 2023 quarter, which is approximately 32.80%.

As per the ADB Asia SME Monitor 2023, 14.2% of the total MSME loans disbursed by the banking sector in 2022 were non-performing loans. A report published by the World Bank in 2019 stated that a financing gap of USD 2.8 billion exists in the MSME sector in Bangladesh, and 60% of the woman-led MSME lack access to finance. The report stated the absence of collateral as one of the key reasons for banks and NBFIs to stay away from the SME sector.

MFIs in SME Financing

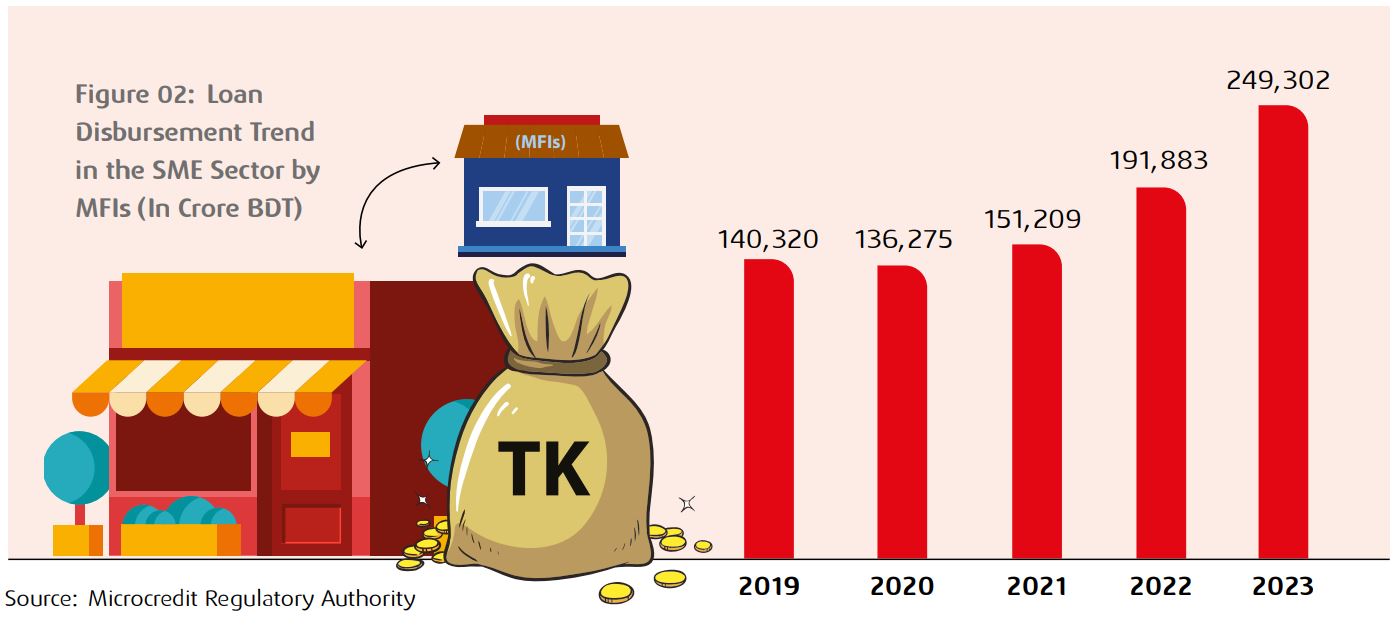

Microfinance institutions (MFIs) in Bangladesh have played a crucial role in bridging the financing gap in the SME sector. As per the annual statistics of the Microcredit Regulatory Authority published in June 2023, microfinance institutions licensed by the Microcredit Regulatory Authority disbursed loans amounting to BDT 249,302 crore in FY2022-23.

As of June 2023, 5.15% of the total loans disbursed by microfinance institutions were non-performing loans.

Challenges Faced by Formal Lenders in Financing the SME Sector

There are a set of unique challenges that banks and NBFIs face while financing in the SME sector. The challenges have been discussed below.

Lack of Collateral: SME owners usually do not have much valuable land that they can offer to banks and NBFIs as mortgages. On the other hand, as banks and NBFIs deal with the money of the depositors, the securities of the loans they disburse are of their primary concern. If SMEs do not offer mortgages, settlements of the default accounts become complicated and time-consuming in cases of default. From a risk management perspective, banks and NBFIs find it more comforting when they receive mortgages as securities.

Lack of Authenticity of Financial Data: Banks and NBFIs seek the financial data of SMEs when they appraise them for offering credits. Credit assessment is a data-driven process that requires authentic data as input. But the bookkeeping of SMEs is not that organized. When it comes to SMEs, there is hardly any way to validate the data regarding sales, receivables, inventories, payables, expenditures, and so on. As a result, it becomes difficult for banks and NBFIs to appraise SMEs.

Informal Borrowing: If any individual enjoys any financing facility from any bank or NBFI, it is reported in the Credit Information Bureau (CIB) report. However, a large portion of the SMEs are unbanked, and they avail loans from microfinance institutions. Loans from the microfinance institutions are not reported in the CIB report. Hence, there is a risk of burdening the SMEs with liabilities, as officials of banks and NBFIs are unable to trace the facilities to microfinance institutions.

Absence of Documentation: Applying for the licenses and keeping the licenses updated involve time-consuming and costly processes. Hence, SME clients are not that motivated to apply for all the licenses that have been declared mandatory by designated authorities to apply for loans from banks and NBFIs. As SMEs usually do not have the licenses ready, banks and NBFIs face many difficulties while financing them.

Narrow Market Access: SMEs usually cover small geographical areas. Their suppliers and customers are located in closer proximity. Lack of efficient logistics does not allow them to leverage business opportunities at remote locations or abroad. Due to narrow market access, it is difficult for SMEs to grow their revenues and cut their costs.

Lower Shock Absorption Capacity: SMEs have lower shock absorption capacity. In cases of macroeconomic instability, SMEs are not able to absorb the shocks like large businesses can. Hence, SME portfolios become impacted in the event of economic shocks.

Challenges Faced by SMEs

SMEs lack access to finance because of the aforementioned challenges that banks and NBFIs face in financing them. Apart from lack of access to finance, there are quite a lot of other challenges that SMEs face.

Higher Interest Rate: According to a circular published by the central bank in May 2024, SMART has been suspended and interest rates have been made market-driven. Since October 2023, the weighted average interest rate of scheduled banks has kept rising. Apart from the facilities under the refinancing schemes, the cost of financing has become very expensive for SMEs.

Poor Logistical Support: SMEs operate in small geographical areas. They cannot expand their businesses beyond their territories because of poor logistical support. Maintaining fleets of their own is very expensive for SMEs. On the other hand, rented transportation adds to costs. Often, SMEs fail to generate cross-district revenues, let alone cross-border revenues.

Lack of One-Stop Services: Often, the SMEs that are manufacturing in nature require lots of licenses, such as trade licenses, environmental clearance certificates, fire licenses, and so on. For these licenses, they have to pay visits to different desks. Licensing would have been much easier if there were one-stop services.

Lack of Forward and Backward Integration: SMEs rely on other business for sourcing and distribution. They cannot ensure forward integration and backward integration. Often they fail to select the right suppliers and the right distribution channels. Inefficiencies are found throughout the supply chain.

Lack of Technological Literacy: SMEs do not leverage technologies primarily because of a lack of digital literacy. Technologies can get the same job done at lower costs and with fewer efforts. SMEs fail to take advantage of technologies and never catch up with the large businesses that employ all the state-of-the-art technologies.

Lack of Skilled Human Resources: SMEs usually do not have the capacity to hire skilled manpower. Skilled workers cost more, but they offer higher productivity and efficiency. SMEs fail to reap the benefits of hiring skilled manpower.

Solutions to Address the Challenges

To address the challenges faced by the formal lenders and the SMEs, the solutions provided below may turn out to be effective.

Scorecard-Based Assessment: As formal lenders face difficulties financing SMEs due to the insufficiency of documents, robust scorecards can be developed to assess the creditworthiness of the borrowers. Banks and NBFIs may examine their respective SME portfolios and identify the factors because of which SME accounts become non-performing. Based on the identified factors, scorecards can be developed to make credit decisions. The documents that do not impact the creditworthiness of the borrowers can be omitted from the documentation process.

Cash-flow-Based Financing: As SME borrowers often fail to offer collateral to formal lenders, formal lenders need to reengineer their assessment processes. Determining the loan amount based on the market value of collateral is not going to work for SME borrowers. Rather, proposals to finance SME businesses should be assessed based on their cash flows.

Hub and Spoke Model: As SME businesses require close monitoring, the banks and NBFIs may follow the hub and spoke model to closely monitor the SME clients. Decentralised sourcing and credit operations will help to ensure efficient sourcing, faster credit decision-making, and better customer service.

Electronic Know-Your-Customer (KYC) Process: Electronic KYC can now be performed by ensuring the national IDs, photos, and fingerprints of the clients. Electronic KYC is faster, more authentic, and verifiable.

App-based Bookkeeping: SME borrowers should be encouraged by formal lenders to ensure a structured bookkeeping process. Apps can be very useful in this regard. Transactions and bookkeeping via the app will help the formal lenders verify the authenticity of the financial data.

B2B Marketplace for SMEs: SMEs prefer to operate within a specific geographic area. There may be suppliers in distant locations, sourcing from which may be more efficient. However, SMEs often fail to connect with suppliers located at distant locations. Hence, a B2B marketplace may be helpful in this regard.

Training: Formal lenders may organise trainings for their SME clients to raise awareness among them and equip them with the necessary expertise. It will enhance their brand images and help create a potential SME client base.

Technologies SMEs Can Leverage for Better Creditworthiness

There are multiple startups in the country offering solutions that SMEs can leverage to make themselves more creditworthy.

TallyKhata: Since it was launched in 2020, TallyKhata has been providing an app-based digital platform for bookkeeping solutions for SMEs in Bangladesh. TallyKhata provides digital wallets and QR codes for SMEs, allowing their customers to make payments from any bank or mobile banking app. It has more than one million active users. TallyKhata plans to offer digital credit solutions for SMEs in partnership with banks and NBFIs. To help assess the creditworthiness of SMEs, TallyKhata will generate credit scores based on transactions and activities on the app.

SMEVai: SMEVai Technologies Limited is a cloud-based platform offering one-stop business solutions to make SMEs bankable in Bangladesh. The company adopts a ‘tech and touch’ approach, where it leverages technology with a hint of human expertise. It provides solutions to the primary business requirements of SMEs, namely accounting, marketing, legal, and training services. It envisions empowering 100,000 SMEs within the next five years.

The instrumental role of lenders in bridging the financing gap for SMEs in Bangladesh cannot be overstated. Lenders have the power to unlock the full potential of SMEs, driving economic growth, job creation, and poverty alleviation. By recognizing the unique needs and challenges faced by SMEs and actively working to address them, lenders can not only empower individual businesses but also contribute to the overall resilience and dynamism of Bangladesh's economy. Thus, fostering a symbiotic relationship between lenders and SMEs is not just a financial imperative but a moral imperative, ensuring inclusive and sustainable development for all stakeholders involved.

Empowering the SMEs: The Instrumental Role of Lenders in Bridging the Financing Gap

In Bangladesh, small and medium-sized enterprises (SMEs) contribute only 25% of the country's GDP. However, this sector represents more than 90 percent of total business entities in Bangladesh and generates employment for 24.50 million people. According to a World Bank estimate, there is a USD 2.8 billion financing gap in this sector in Bangladesh, which is a major impediment to the country's growth potential.

Banks and other financial institutions have an enormous opportunity to offer innovative financial products and services to SMEs. However, there are several critical factors that are working as deterrents to SME financing: lack of collateral, lack of authenticity of financial data, informal borrowing, absence of documentation, narrow market access, and lower shock absorption capacity of the SMEs.

In the challenging terrain of SME financing, innovative initiatives such as the introduction of electronic KYC, providing transaction-based financing, and the adoption of financial technologies are crucial. Moreover, fostering a collaborative and responsive lending ecosystem is essential for unlocking the full potential of Bangladesh's SME landscape. By catering to the specific financing needs of SMEs, lenders can unlock new avenues for growth, innovation, and employment generation, ultimately contributing to the country's economic prosperity and social well-being.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View