Beyond Banking: A Deep Dive into BaaS

Md. Faruk Hasan

Banking as a Service (BaaS) has the potential to completely overhaul the way financial services are provided in Bangladesh, where traditional banking has struggled to serve the massive unbanked population. Only 52.81% of adults in Bangladesh had access to formal financial services in 2021, according to the World Bank's Global Findex Database, highlighting the urgent need for innovative solutions to drive financial inclusion.

In the fast-paced realm of finance, technological advancements have sparked a revolution, reshaping how we interact with money and banking services. Among the myriad innovations, BaaS stands out as a transformative concept that is redefining the traditional banking landscape.

Understanding Banking as a Service

Banking as a Service, often abbreviated as BaaS, is a concept that has gained significant traction in recent years, propelled by the rapid digitisation of financial services and the growing demand for seamless, user-centric banking experiences. At its core, BaaS represents a paradigm shift in the way financial services are delivered, enabling non-bank entities, such as FinTech companies and non-FinTech businesses, to offer core banking services to their customers without the need for a banking license.

The fundamental premise of BaaS lies in the integration of non-bank entities with traditional banking infrastructure through Application Programming Interfaces (APIs). These APIs serve as the conduit through which businesses can access essential banking functions, such as account management, payment processing, and lending services, seamlessly embedding them into their own product offerings.

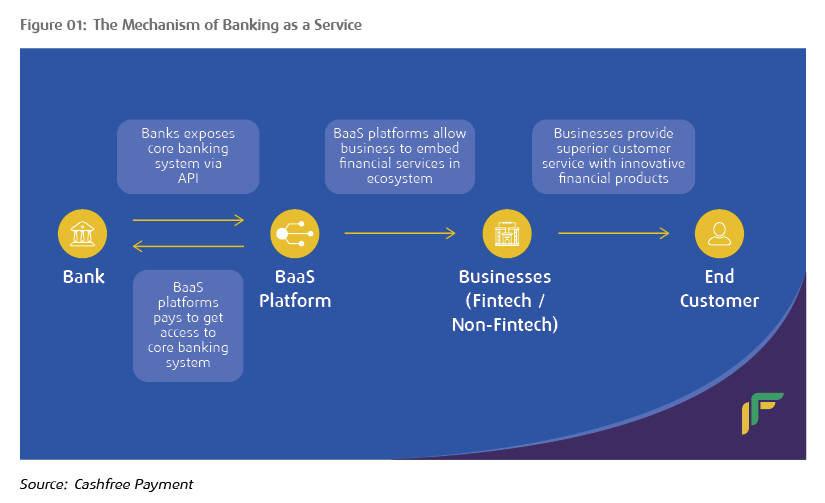

The Mechanism of Banking as a Service

To comprehend the mechanics of BaaS, it is essential to dissect the roles of the key players involved.

i. The Bank: Traditional banks, along with newer digital banking players, serve as the foundational pillars of BaaS. These institutions provide the necessary infrastructure, including banking licences and core banking systems, which form the backbone of the BaaS ecosystem. By exposing their core banking functionalities through APIs, banks enable non-bank entities to leverage their infrastructure and offer financial services to their customers.

ii. BaaS Platform: Acting as intermediaries, BaaS platforms facilitate seamless communication between traditional banks and non-bank entities. These platforms, often referred to as middleware, ensure secure data transmission and compliance with regulatory standards. By offering API-based solutions, BaaS platforms empower businesses to integrate banking services into their applications and products without the need for complex infrastructure development.

ii. FinTech and Non-FinTech Businesses: At the forefront of the BaaS revolution are FinTech companies and non-FinTech businesses that interact directly with end customers. By leveraging BaaS platforms, these entities can offer a wide array of financial services, ranging from digital payments and lending to wealth management, without being burdened by the regulatory complexities of traditional banking. Through seamless integration with BaaS platforms, businesses can enhance their product offerings and deliver tailored financial solutions to their customers.

BaaS's main objective is to make it possible for companies to provide banking services to their clients without needing to get their own banking licenses. Utilizing the infrastructure and regulatory adherence of well-established financial institutions frees up businesses to concentrate on providing cutting-edge financial services and solutions that are customized for their target markets. BaaS offers a special chance to close the gap between the underserved and the banking industry in this era of digitalization. BaaS extends the reach of financial services to even the most remote areas of the nation by empowering non-banking entities, like FinTech companies and even retailers, to seamlessly integrate banking services into their platforms and products by leveraging the power of technology and partnerships.

Adoption of BaaS in Bangladesh

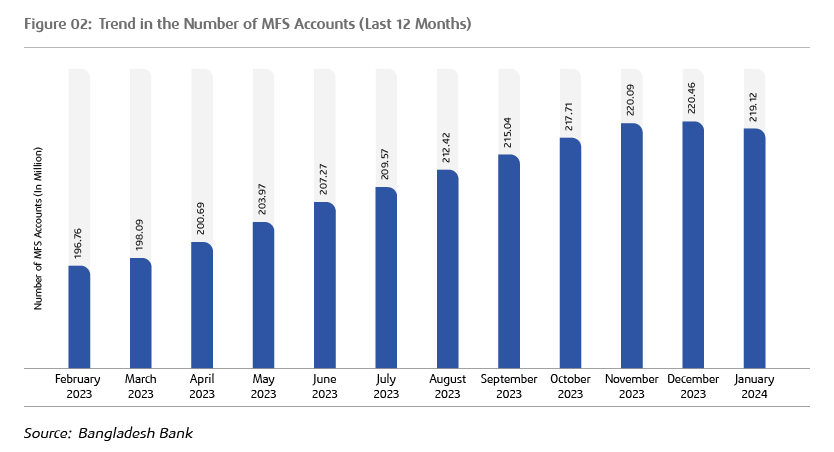

The potential impact of BaaS in Bangladesh is substantial. Statistics by the central bank of Bangladesh on the mobile financial services (MFS) industry reveal that the number of registered MFS accounts stood at a staggering 219.12 million as of January 2024, with bKash, the pioneering mobile financial services provider, accounting for the majority market share. This widespread adoption of mobile financial services underscores the readiness of the Bangladeshi population to embrace digital banking solutions, paving the way for BaaS to thrive. Moreover, the burgeoning FinTech ecosystem in Bangladesh is a testament to the growing demand for innovative financial services. As per a report published in The Business Standard, there are at least 198 FinTech startups. BaaS presents these FinTech companies with opportunities to leverage the infrastructure and regulatory compliance of established banks, enabling them to introduce cutting-edge financial products and services tailored to the unique needs of the Bangladeshi market.

Bangladesh's entry into the digital lending era is exemplified by the collaborative efforts of The City Bank, a prominent private commercial bank, and bKash. After a year of testing under Bangladesh Bank's supervision, the ‘digital nano loan’ was commercially introduced on bKash's platform in 2021. Since then, users of the bKash app have obtained nano loans from The City Bank totaling BDT 7 billion.

According to Prothom Alo, 245,000 bKash customers have availed this collateral-free nano loan 0.70 million times. Many of these customers have taken this hassle-free, instant, and affordable loan multiple times. By guaranteeing credit availability, the primary goal of this digital loan program is to expedite the financial inclusion of the nation's impoverished populace, particularly women and those residing in rural areas. About 24% of these clients are female as of 2023, while 55% of all borrowers reside in rural areas. Customers of bKash who have completed their e-KYC via the bKash app are deemed qualified for this loan from The City Bank, in accordance with directives from the central bank. An automated credit assessment system determines the customers’ loan eligibility and amount based on their transactions in their bKash account and The City Bank's credit policy. With just a few taps, eligible customers can quickly obtain a nano loan from The City Bank, with amounts ranging from BDT 500 to BDT 20,000. Customers can apply for this loan without having to visit the office, sign any paperwork, or even have a nominee or guarantor.

Adoption of BaaS among the Regional Peers

Bangladesh's neighbouring country, India, has been at the forefront of BaaS adoption, with several notable examples. According to Stellar Market Research, the Indian BaaS market was valued at USD 12.67 billion in 2023, and the total BaaS revenue is expected to grow at 13.20% from 2024 to 2030, reaching nearly USD 30.19 billion.

In 2013, BaaS was introduced by Yes Bank and RBL Bank, which made multiple APIs available. Afterwards, a number of banks debuted their API developer portals and hubs, including Barclays, J.P. Morgan, Wells Fargo, and Citi. All of the country's main private banks, including HDFC, ICICI, and Kotak, currently offer APIs, while a number of BaaS FinTech startups, including Zeta, Setu, and Yap, are expanding quickly thanks to increasing funding. As major banks started to make their APIs available, a new group of challengers and neobanks emerged, focusing primarily on digital banking. Paytm and Open are arguably the most noteworthy success stories in the Indian retail banking sector.

Perks of BaaS

The BaaS model presents a wealth of benefits for banks, non-bank businesses, and end-customers alike.

For Banks:

⬤ Increased sources of revenue through API-based transactions and partnerships.

⬤ Cost savings by leveraging third-party solutions and expertise.

⬤ Enhanced customer insights and personalisation capabilities.

For Non-banking Businesses:

⬤ Ability to bypass complex banking regulations and licence requirements.

⬤ Innovative financial solutions for customers.

⬤ Increased customer trust and loyalty by leveraging the brand reputation of banks.

For End-customers:

⬤ Access to a wider range of user-friendly, integrated financial services.

⬤ Improved customer experience and seamless interactions.

⬤ Greater financial inclusion and access to credit for underserved populations.

Unlocking the Full Potential of BaaS in Bangladesh

As the nation continues to embrace digitalization and cultivate a conducive environment for fintech innovation, BaaS is poised to play a pivotal role in driving financial inclusion, fostering entrepreneurship, and accelerating economic growth. To fully capitalise on the benefits of BaaS, Bangladesh's financial industry must take a proactive and collaborative approach. Banks should prioritise the modernization of their core banking systems, transitioning to a more modular and API-driven architecture. This will enable them to seamlessly integrate with BaaS platforms and offer their services to a wider range of businesses and customers.

Regulators, too, have a crucial role to play. By establishing a supportive legislative framework and nurturing a conducive environment for FinTech innovation, they can pave the way for the widespread adoption of BaaS in Bangladesh. This includes developing robust digital infrastructure, incentivizing talent development programmes, and ensuring a streamlined regulatory environment that encourages collaboration between banks, FinTech firms, and technology providers.

A strong digital infrastructure, talent development programmes, and a legislative environment in favour of BaaS would be necessary for its successful implementation in Bangladesh. Working together, regulators, banks, FinTech firms, and technology suppliers must play their respective roles to overcome obstacles and realise the full promise of BaaS.

The author is working as a data scientist at IDLC Finance PLC. and can be reached at farukmd@idlc.com.

Battery Industry in Bangladesh: Powering Up the Nation on the Go

The lead-acid battery industry, which has grown three to four times in the last decade and is valued at BDT 10,000 crore currently, serves a wide variety of purposes without which portability and mobility would have never been a possibility. Solar panels, easy bikes, battery-run rickshaws, passenger transports, commercial vehicles, IPS, UPS, and telecommunication towers—all these either run on batteries or require batteries as power storage. The fact that the lead-acid battery industry exported around USD 29 million worth of batteries on average in the last five fiscal years makes the industry a potential contributor to our foreign exchange earnings as well.

It is not unknown that the industry faces controversies due to the unregulated manufacturing and recycling operations of some market players. Just like many other industries dependent on imports of raw materials, the rising dollar price has affected the industry adversely. On top of that, the potential emergence of the local lithium battery industry may bring additional challenges. However, policymakers should come forward to create a conducive business environment for this decades-old industry and regularise the unregulated players to minimise the associated environmental and health risks and boost the country’s tax revenues.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View