Bridging The Financing Gap For The Marginalised : Microfinance Uplifting Bangladesh’s Social Fabric And Economy

Written By Syed Md. Rakeen, Team MBR

Microfinance has established itself as one of the bedrocks of financial inclusion in Bangladesh. While formal banking channels shied away from lending to marginalised communities, microfinance institutions have leapt ahead by catering to the unbanked and rural households of Bangladesh. The current advancement of financial inclusion in Bangladesh can be highly attributed to microfinance institutions or MFIs. Their innovation and expansion of services in serving the underserved population and marginalised communities of Bangladesh, especially those living in rural and isolated locations with little access to traditional financial services, has aided in alleviating poverty and strengthening the socio-economic status of Bangladesh. NGO MFIs have connected financial services to the communities by opening branches and field offices across all districts, facilitating people’s access to loans, savings accounts, insurance, remittances, and other financial goods. NGO MFIs have created and provided tailored financial solutions to meet the unique requirements and conditions of low-income people and communities. They have created microloans that have adjustable payback periods, are sensitive to changes in seasonal revenue, and are in line with the cash flow patterns of borrowers who work in seasonal jobs like agriculture.

According to the Microcredit Regulatory Authority, the loan disbursements of microfinance rose from BDT 45,600 crore in FY12 to BDT 191,800 crore in FY22. In the fiscal year 2021–22, Microfinance institutions demonstrated commendable performance by disbursing a staggering BDT 226,007 crore in loans while receiving BDT 85,036 crore in customer savings. The implementation of government stimulus packages to offset the adverse effects of COVID-19 has helped borrowers keep their businesses upright during difficult times. Existence of MFIs across Bangladesh

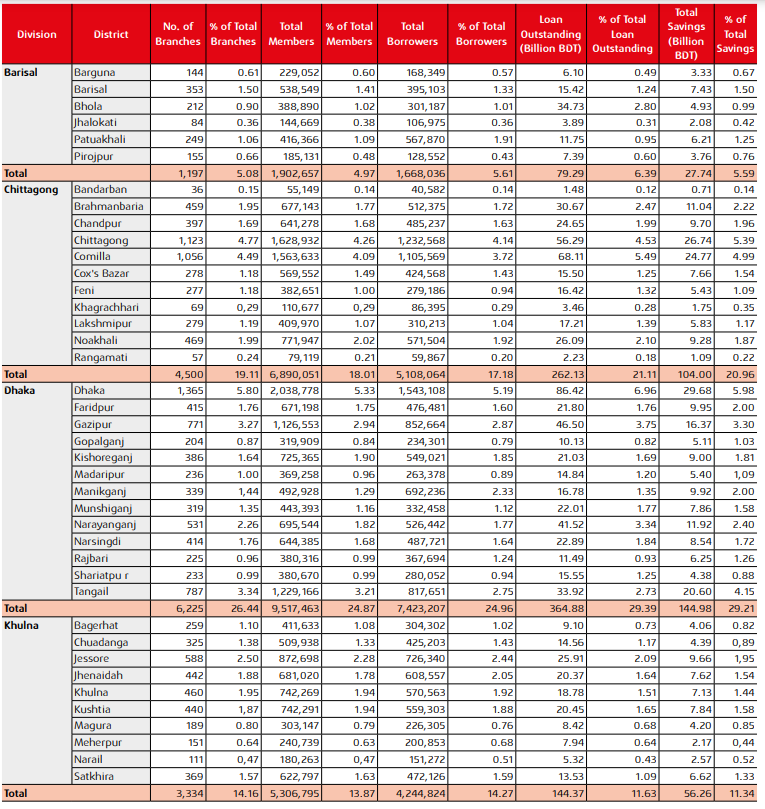

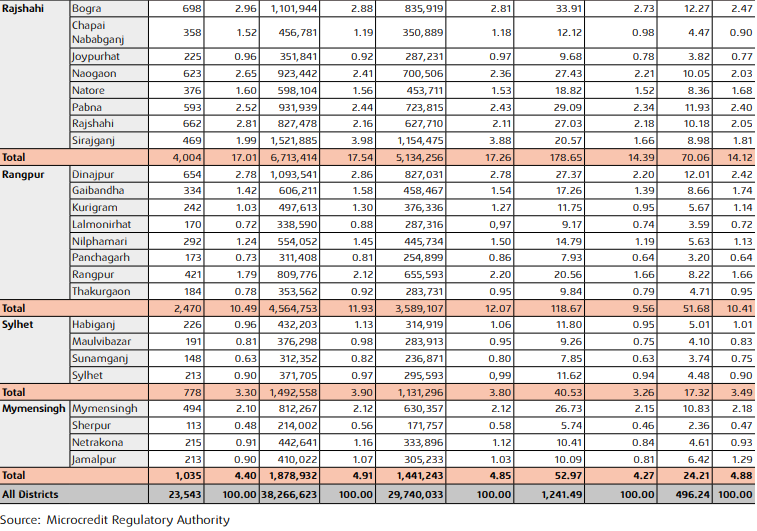

The microfinance institutions have spread their wings across various outskirts of the country, with a total of 739 MFIs and 23,543 branches currently operating under the licence of the Microcredit Regulatory Authority (MRA) as recorded until June 30, 2022. The huge successes of these organisations led them to open a further 2,588 branches in both rural and urban areas during FY2021–2022, widening their net and reaching every underserved community in Bangladesh. A comprehensive division and district-wise distribution of branches, members, borrowers, loan outstanding, and total savings are given below:

Table 1: Division and District-wise Branches, Members, Borrowers, Loan Outstanding, and Savings

Contribution of MFIs in Bangladesh

Several microfinance institutions have popped up in Bangladesh ever since the inception of Grameen Bank in 1983. Apart from Grameen Bank, the top 10 performing microfinance institutions are BRAC, ASA, Bureau Bangladesh, TMSS, Society for Social Service, Jagorani Chakra Foundation, Padakhep Manabik Unnayan Kendra, United Development Initiatives for Programmed Actions, Sajida Foundation, and Palli Mongal Karmosuchi. These institutions have demonstrated significant impact and effectiveness in providing financial services to underserved populations, particularly in the field of microfinance. Their contributions have been widely recognised, and they continue to play a crucial role in promoting financial inclusion and reducing poverty-stricken households.

In general, microfinance institutions operating in Bangladesh provide financing and microfinance support in six distinct categories of loans: microcredit for self-employed activities, microenterprise loans, loans for the ultra-poor, agricultural loans, seasonal loans, and loans for disaster management. Microcredit is often defined as loans reaching up to a maximum of BDT 50,000; loans beyond BDT 50,000 but less than BDT 1 million are classified as microenterprise loans.

Despite several microfinance institutions partaking in microcredit programmes, only ten significant microfinance institutions and Grameen Bank account for 87% of the sector’s total deposits and 81% of its total outstanding loans, as reported by Bangladesh Bank. Approximately 30 million impoverished people directly benefit from microcredit programs. Through the financial services of microcredit, low-income households are engaging in various income-generating activities.

Enhancing the Socio-Economic Status through Microfinance

While microfinance helps to avail financing support from MFIs, its contribution has a deeper underlying impact on the marginalised community of Bangladesh. The business development of rural regions can largely be attributed to MFIs’ disbursement of loans while ensuring financial sustainability in the process. Poverty alleviation and empowering marginalised communities have radically transformed the economies of rural regions, with MFIs increasing their attempts to expand their microfinance portfolio. Their successes have exceeded the performances of formal banking channels in many parameters, with the Microcredit Regulatory Authority (MRA) reporting that the annual turnover of this sector is estimated to be around BDT 1.60 trillion while the loan recovery rate stands at an astonishing 98%, of which 91% of the borrowers are women.

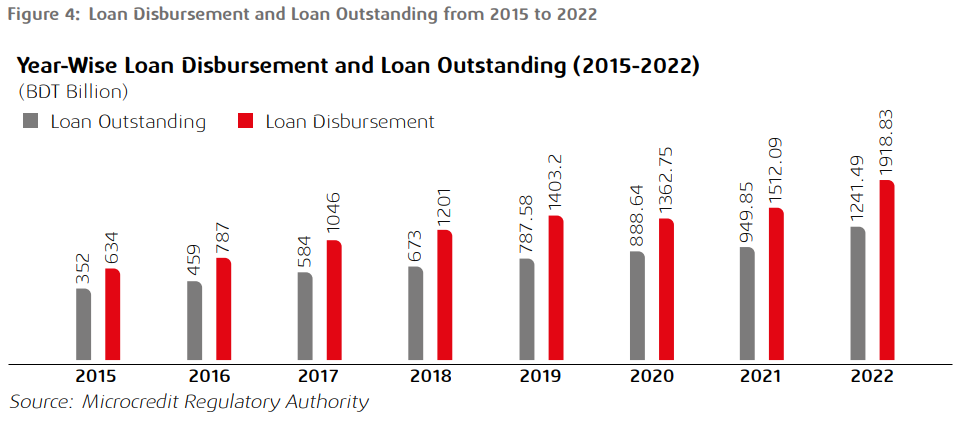

Moreover, the activities of these MFIs also contributed to the generation of employment opportunities for around 207 thousand individuals. In the fiscal year under consideration, microfinance institutions distributed a total of BDT 1,918.8 billion to their clients throughout the country. This enormous disbursement played a crucial role in bolstering the overall growth of the country’s gross domestic product (GDP) and furthering financial inclusion efforts.

Microfinance Areas of MFIs

Microfinance institutions are actively contributing to the socio-economic development of the country by disbursing microloans in the cottage, micro, small, and medium enterprise (CMSME) sector. The CMSME sector primarily consists of the following subsectors:

Loan Disbursements and Outstanding of MFIs

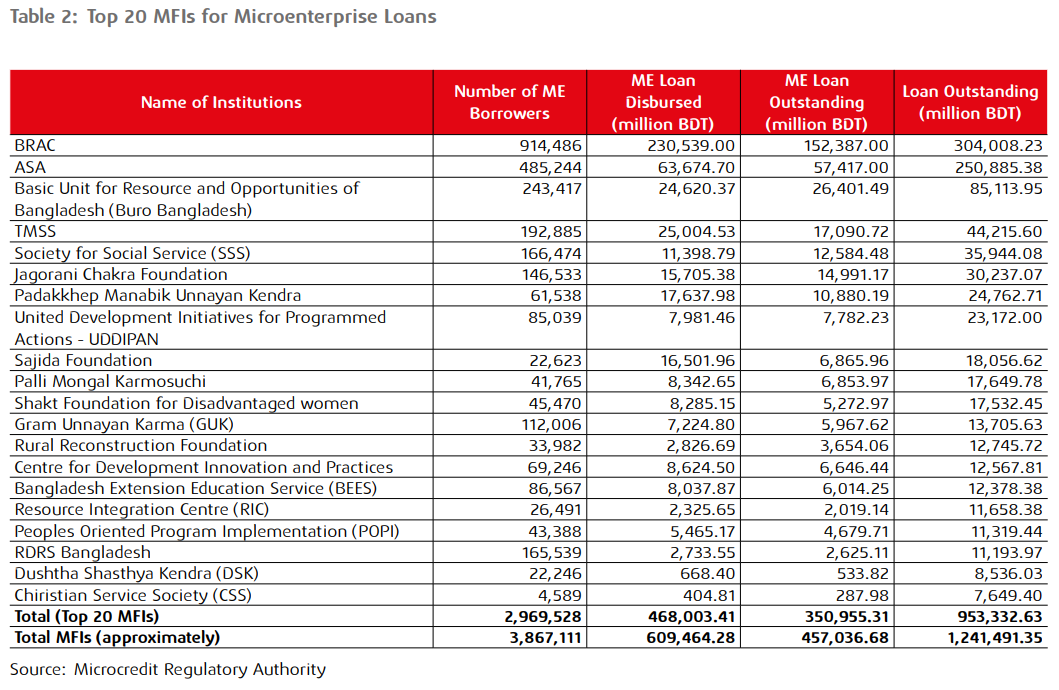

In the year 2022, a total of BDT 468 billion was disbursed by the top 20 microfinance institutions in a bid to support microenterprises. Among these MFIs, BRAC contributed 49.26% of the disbursed amount, while ASA contributed 13.61%. In the year 2022, the total loan outstanding of the top 10 microfinance institutions amounted to BDT 953.33 billion. Among these, the Micro Enterprise (ME) sector accounted for BDT 350.95 billion. In the fiscal year 2021–22, it was observed that licenced microfinance institutions played a significant role in extending financial services to about 38.26 million individuals belonging to marginalised segments of the population. This outreach was made possible through the operation of 23,543 branches across the country.

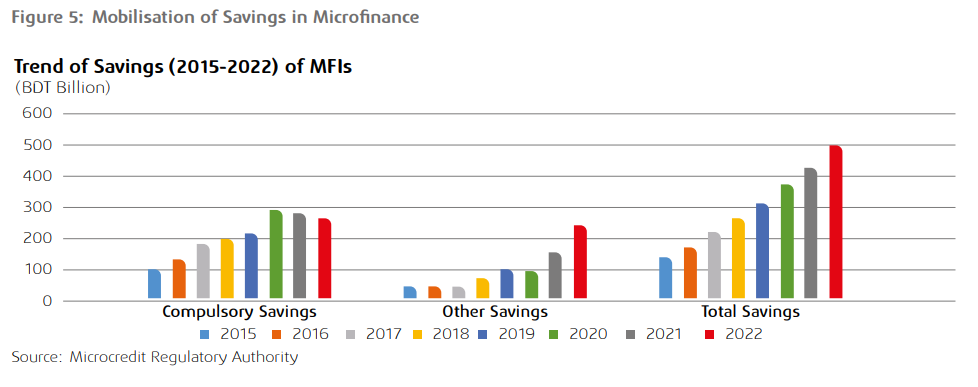

Mobilisation of Savings for Depositors

Apart from microfinance loans, savings collected from clients are one of the leading microfinance products from MFIs. Mobilising savings can assist MFIs in broadening and improving their outreach. The poorest households, in particular, could depend on savings before they possess a legitimate claim for credit. Furthermore, public deposits are a more stable source of funding than other options like donor organisations or lines from the central bank. This steady financial source can increase lending operations, helping the underprivileged in the process.

Microenterprise (ME) Loans of MFIs

The threshold for qualifying as a microenterprise loan lies between BDT 50,000 and BDT 1 million. These businesses were categorised and reorganised according to the 2016 Industrial Policy set by the Ministry of Industries (MOI) and the Government of Bangladesh. Businesses were broken down into many groups, which included controlled, high-priority, large, medium, small, micro, handicrafts, high-tech, and creative research industries. MFIs played an immense role in microbusiness segmentation due to their strong relationships with their clients. The current rule of MRA states that MFIs are permitted to disburse up to 50% of their loans to microenterprises. Recently, the Asian Development Bank (ADB) approved a USD 200 million loan to help microenterprises thrive in Bangladesh, especially the ones led by women, along with the regions with high exposure to climate disasters. Table 2 represents the microenterprise landscape of the top 20 MFIs in Bangladesh in terms of their borrowers, loan disbursements, and loan outstanding.

The Central Bank's Role in Fostering Microfinance Growth

Bangladesh Bank has stepped up its efforts to enhance financial inclusion in Bangladesh by facilitating access to microcredit through a digital loan scheme. The allocation for the digital loan scheme targeting the underprivileged population has been augmented to BDT 500 crore. The surge in loan uptake can be attributed to an escalation in demand for such financial products, primarily driven by the aim to enhance digital banking services within the socioeconomically disadvantaged and marginalised segments of the population within the nation. As per the circular issued by the central bank, it has been stipulated that scheduled banks shall have the authority to extend loans through digital channels, including but not limited to internet banking, mobile applications, mobile financial services (MFS), and electronic wallets. The duration of the loan shall not exceed six months, as stipulated by both the financial institution and the borrower.

In pursuit of the objective of establishing Digital Bangladesh, the central bank has introduced a refinancing scheme. This scheme has been devised to facilitate the provision of digital microcredits at a reduced interest rate. Its primary goal is to ensure the accessibility of small loans, incentivise banks to participate, and mitigate their funding expenses.

Access to Nano Loans through Digital Means

The advent of mobile financial technology has facilitated the initiation of commercial lending to the informal sector. This service has facilitated Bangladesh's foray into the realm of digital microfinance. The loan programme offered by bKash is available to eligible users who meet the specified criteria. These individuals have the opportunity to borrow at an interest rate of 9%, with the amount ranging from BDT 500 to BDT 20,000. The loan's maximum repayment duration has been determined to be three months. Besides, the loan allocation process is facilitated by an artificial intelligence system that employs a comprehensive analysis of individuals' historical bKash transactions to ascertain their eligibility. The bKash application offers the option to "re-register" individuals who have previously completed the traditional know-your-customer (KYC) registration process and have subsequently become users of bKash. The acquisition of this loan does not necessitate the submission of any documentation, the identification of a nominee, or the provision of a guarantor.

Women's Empowerment through Microfinance

As mentioned earlier, microfinance loans boast a near-perfect 98% loan recovery rate, of which 91% are women. This underlines the importance of microfinance in empowering women to build their own businesses and gain financial independence. The emergence of women's entrepreneurship in Bangladesh can be attributed to the proactive measures taken by the government, including the implementation of various initiatives like microfinance programmes and skill development training. Women have displayed an enhanced capacity to initiate and establish their own entrepreneurial ventures, secure steady employment opportunities, and contribute significantly to the overall growth and development of the national economy. Improving financial literacy holds the key to helping build on the continued success of women's involvement in banking, savings, and investment opportunities. This, in turn, may lead to improved accessibility and utilisation of financial services in Bangladesh.

Tackling Challenges for Microfinance Growth

The attainment of financial sustainability poses a significant hurdle for numerous nongovernmental microfinance institutions (NGO MFIs). High-interest rates present a challenge when providing affordable financial services to low-income people, especially in remote areas. The perpetual challenge faced by nongovernmental microfinance institutions revolves around striking a delicate balance between ensuring the affordability of interest rates for their clients while simultaneously covering operational expenses and sustaining financial viability. Besides, digitalisation, unskilled workers, the fund shortage of small and medium MFIs, and financial literacy contribute to the challenges as well.

Instances of over-indebtedness among borrowers, where borrowers avail loans with the intention of fulfilling their repayment obligations, can lead to financial distress and subsequently diminish the positive outcomes associated with microfinance interventions. The mitigation of this challenge necessitates the implementation of responsible lending practices, the establishment of adequate client protection mechanisms, and the provision of effective credit counselling.

According to the Financial Stability Report 2022 published by the Bangladesh Bank, the nonperforming loans (NPL) of the microfinance sector experienced a significant increase from BDT 4,528 crore in the fiscal year 2020-2021 to BDT 8,370 crore in 2021-22, witnessing an alarming 85% year-on-year rise in NPLs in 2021–22. Rural households are more vulnerable to this economic turmoil; hence, certain measures are needed to shield the marginalised community during economic shocks.

Microfinance institutions have played an instrumental role in alleviating poverty, increasing employment opportunities, and developing CMSME businesses in Bangladesh. In general, Bangladesh is widely recognised as the pioneer of microfinance and currently ranks as one of the largest microfinance sectors in the world. According to the Daily Star, microfinance institutes in Bangladesh disbursed around BDT 900 crore each day and BDT 2 lakh crore each year in 2022. However, persistent problems such as economic shocks, high-interest rates, and limited employment opportunities in rural areas lead to struggles in the repayment of loans. The adoption of digital microfinance has the potential to eliminate the aforementioned problems through faster disbursements. This, in turn, will lead to lower operational costs and interest rates, resulting in attracting more clients. Then again, NGO MFIs can be credited for their massive contribution to ensuring financial inclusion and catering to the underserved population. Their continuous strides towards women's empowerment, financial inclusion, literacy, and development programmes have uplifted the socio-economic state while curbing the poverty rate in rural households and marginalised communities in Bangladesh.

Bridging The Financing Gap For The Marginalised : Microfinance Uplifting Bangladesh’s Social Fabric And Economy

Microfinance has played an instrumental role in enhancing financial inclusion, employment opportunities, and poverty alleviation in Bangladesh. The significant presence of CMSMEs in Bangladesh prompted a rapid rise of microfinance institutions (MFIs) across the country, with 739 MFIs and 23543 branches currently operating under the licence of the Microcredit Regulatory Authority (MRA). During the fiscal year 2021–22, loan disbursements of microfinance reached staggering figures of BDT 226,007 crore, while customer savings stood at BDT 85,036 crore.

The continuous innovation and expansion of microfinance services have facilitated the availability of microcredit and microenterprise loans to the unserved and underserved marginalised community of Bangladesh. The MFIs have flourished in that regard, with annual turnover figures reaching BDT 1.60 trillion while maintaining a near-perfect 98% loan recovery rate, of which 91% of the borrowers are women.

The microfinance sector is met with a fair share of challenges, with high-interest rates and economic shocks largely affecting the financial sustainability of MFIs. Nevertheless, the massive contribution of MFIs towards women’s empowerment, financial inclusion, and poverty reduction has elevated the socio-economic status of Bangladesh and reinforced the belief in the future success of microfinance.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View