The Next Level of Financial Inclusion: Entering the Digital Banking Era

Written By Syed Md. Rakeen, Team MBR

The dream of creating a cashless economy has taken another gigantic step with the formulation of ‘Guidelines to Establish Digital Bank’ by Bangladesh Bank to help guide opening up digital banks in the financial systems of the country. With the deadline extension for applications for digital banks, several financial institutions have entered the fray and lined up to make headway towards digitising banking services and bringing the unbanked population under the banked population umbrella. Digital banking refers to the execution of all online activities pertaining to conventional banks, with the head office being the only physical presence of that particular financial institution. Services, including payments, transfers, savings, credits, insurance, and even securities, are all predicted to go online, offering competitive fees and favourable interest rates for borrowers. The increasing adoption of Mobile Financial Services (MFS) and internet banking services is a promising blueprint for the potential of digital banks’ success. With 47% of the population in Bangladesh remaining unbanked, digital banks can help foster financial inclusion and are expected to play a pivotal role in serving the unserved and underserved population.

The Global Landscape of Digital Banks

COVID-19 acted as a catalyst for the increasing adoption of digital banking services, with banks of different sizes experiencing a massive spike in digital transactions. Wells Fargo, an American multinational financial services company operating in 35 countries and serving over 70 million customers worldwide, oversaw a 35% increase in remote check deposits and a mammoth 50% growth in online wire transfers during the pandemic, as per a report by Deloitte. According to Statista, a leading statistics portal based in Germany, India registered the highest number of digital banking users globally in 2022, with an incredible 295.5 million users, over 70 million more than the US, which sat second on the list. Germany ranked first among the European countries with 51.4 million digital banking users. So far, digital financial services have been successfully implemented in over 80 nations, achieving significant levels of adoption and utilisation. Consequently, many previously marginalised and neglected individuals from low-income backgrounds are transitioning from relying solely on cash-based transactions to engaging with formal financial services.

Eligibility to Establish Digital Banks

Bangladesh Bank has put forward guidelines to set the minimum capital requirement for a digital bank at BDT 125 crore, while for conventional banks, it has been set at BDT 500 crore. As per the guidelines, an individual sponsor of a digital bank is required to hold at least BDT 50 lakhs in shares. Some important features of digital banks include the use of agents of traditional banks or MFS providers as well as the existing ATM, CDM, and CRM networks to facilitate transactions. They are allowed to offer innovative payment solutions such as virtual cards, QR codes, or other technologically advanced products to streamline customer transactions. They will refrain from offering over-the-counter (OTC) services and will not possess any physical branches, subbranches, windows, agents, automated teller machines (ATMs), cash deposit machines (CDMs), or cash recycling machines (CRMs) under their ownership. Automated artificial intelligence (AI)- driven dispute resolution mechanisms will be there to resolve everyday disputes arising from transactions. They will implement AI-based credit scoring systems to extend loans to various sectors.

Digital Banking Services in Bangladesh

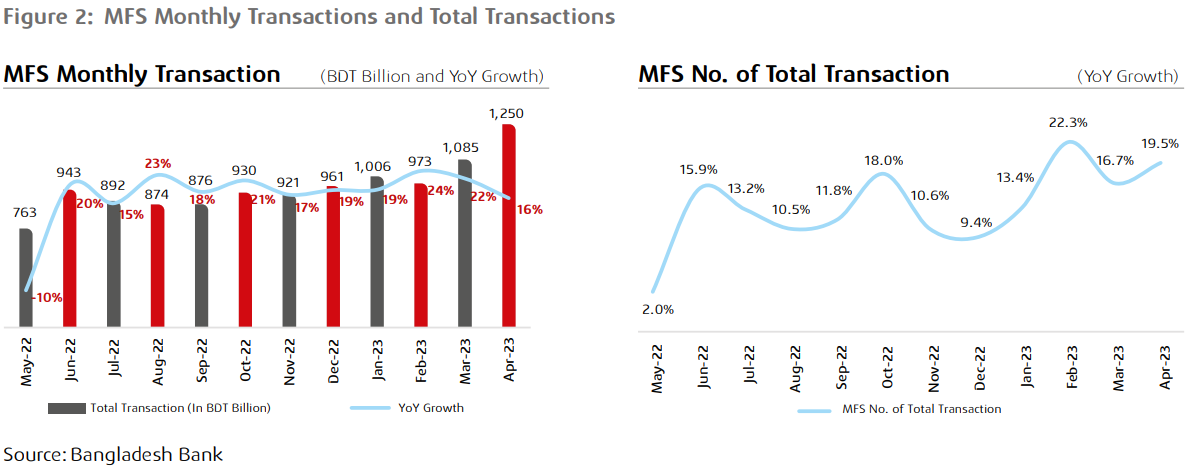

The availability of smartphones and MFS have acted as the most significant enablers of digital banking services in Bangladesh. This has altered the landscape by facilitating the integration of previously excluded and underserved demographics, particularly those from lowincome households, into financial services. The introduction of bKash in Bangladesh has radically transformed how people transfer money and reshaped conventional forms of fund transfers. Numerous banks followed suit with their digital banking services, facilitating transactions and speeding up the transfer of funds. The latest report by Bangladesh Bank stated that the daily average transactions of Mobile Financial Services (MFS) exceeded BDT 32 billion, and the figures indicate a growing trend, with MFS transactions registering a year-on-year growth of 19.5% in April 2023 compared to April 2022. Internet banking transactions registered a year-on-year increase of 16% in April 2023.

A recent uprising of fintech startups has led to the arrival of numerous digital banking services in Bangladesh in a bid to seize at least a small piece of the massive untapped market.

Promoting Financial Inclusion through Digital Banking

While the widespread adoption of branch banking, agent banking, and MFS has significantly enhanced economic activities, a large population remains unbanked due to the lower internet penetration rate in Bangladesh, which is currently only 38.9%, as reported by Datareportal. Data from the World Bank revealed that only 53% of the individuals in Bangladesh are part of the formal financial infrastructure. Taking bank accounts and credit cards only into account, the figure stands at around 20%, while the rest belong to MFS. Through digital financial inclusion, Bangladesh can mitigate expenses and vulnerabilities associated with cash-based transactions, including but not limited to losses, thefts, and various financial crimes. The transition from mere account access to active account utilisation represents the subsequent phase for economies where a significant portion of the populace possesses accounts. This phenomenon is observed in countries such as China, Kenya, India, and Thailand, among various others. The economic growth of these nations was driven by implementing reforms, fostering private sector innovation, and promoting the accessibility of affordable accounts, such as mobile and digitally- enabled payment options.

Besides, the United Nations Sustainable Development Goals (SDGs) identify and the World Bank (WB) confirm financial inclusion as a key driver of a country’s sustainable economic growth as it ensures access to useful and affordable financial products and services for individual and organisational entities in the form of transactions, payments, savings, credits, and insurances.

Potential Entrants to the Digital Bank Ecosystem

Upon the introduction of digital banking policy guidelines by the central bank, approximately 20% of traditional banks in Bangladesh are poised to establish digital banks in order to enhance their market penetration across the entire nation, effectively attracting and retaining technologically inclined customers without the need for physical infrastructure. A total of 10 banks have formed a coalition of strategic initiatives to form a consortium named Digi10 Bank PLC, while Bank Asia and Brac Bank have expressed their interest in becoming sponsors for two digital banks. Out of the 10 banks, The City Bank, Eastern Bank, Mutual Trust Bank, Mercantile Bank, National Credit and Commerce Bank, and Pubali Bank are planning to allocate capital towards the establishment of a digital bank. Additionally, Dutch-Bangla Bank and Trust Bank are expected to join this consortium. Moreover, bKash, Nagad, and Banglalink are also preparing to launch digital banks, with their applications for digital banks looming large with every passing day.

Bringing CMSMEs under the Banking Umbrella

Within traditional banking, around 6.94 milliomn enterprises can be classified as unbanked or underbanked. Based on the Financial Stability Report 2022 released by the Bangladesh Bank, the net outstanding investment in the CMSME sector of both the Banks’ and NBFIs’ amounted to BDT 2,093.92 billion as of June 2021, in comparison to the total outstanding advances of BDT 11,514.71 billion. This figure represents 18.18% of the total outstanding financing that banks and NBFIs have allocated to the CMSME sectors. The impending arrival of digital banks can bring forward changes that can foster financial inclusion for the underserved and unserved populations, and its successes can translate to the flourishing of financial institutions, which, in turn, can increase economic activities in Bangladesh.

Leapfrogging through Challenges for Financial Inclusion

Despite the immense prospects of digital banking, it comes with a lot of challenges for both banked and unbanked populations. The digital literacy of Bangladesh remains significantly low, and it may be proven to be a barrier to exploiting the full potential of digital banks. But the upward trajectory of digital literacy among individuals is currently experiencing a notable expansion. The insufficiency of digital infrastructure constitutes an additional detrimental factor in this particular instance. A robust internet connection is a prerequisite for facilitating seamless digital transactions. In order to facilitate the transition towards a cashless or digital society, the cost of producing digital products such as smartphones must be reduced to foster financial inclusion.

The declining proportion of conventional banks can threaten the employment of currently employed and aspirant bankers. Traditional banks incur higher operating costs due to their need to maintain physical branches and employ a substantial workforce. Conversely, digital banks typically enjoy lower overhead expenses, potentially enabling them to offer more competitive fees and superior interest rates. Furthermore, digital banking customers can acquire virtual debit cards, which are a secure and convenient means for engaging in e-commerce transactions. Digital banking institutions can offer numerous personal loan services by harnessing technological advancements to optimise loan approval and disbursement procedures.

However, even with the convenience of self- service options, many customers may place importance on personalised interactions and seek guidance from physical confrontation when dealing with intricate financial decisions. In that case, conventional bank employees can play an advisory role by engaging in the tasks of cultivating and sustaining customer relationships, providing personalised financial guidance, and facilitating complex transactions.

Over time, the banking industry in Bangladesh has undergone significant changes as a result of new technologies and innovations. Although the widespread adoption of traditional banks is still visible, digital banks are expected to make up the ground and can gradually push conventional banking towards obsolescence by presenting customers with a more convenient and accessible banking alternative. Additionally, serving the unbanked population can experience a much-needed boost owing to the convenience, time savings, and cost savings of availing the services of digital banks. In the grand scheme of things, bringing the unbanked population under the banking umbrella can lead to flourishing economic growth amidst economic uncertainties. By implementing various economic instruments such as credit guarantees, first-loss capital, tax incentives, or refinancing schemes, the government can effectively introduce incentivization mechanisms within targeted sectors. This approach entails accessing sectors with the aim of mobilising supplementary capital, such as health, climate, education, food security, alternative energy, and circularity. Additionally, it involves facilitating financial accessibility for underserved enterprises and communities. The establishment of a fund of funds aimed at providing financial support to micro-entrepreneurs and underserved communities, coupled with the development of a standardised verification and monitoring system for these investments, will contribute positively to the overall trajectory of financial inclusion and make giant strides towards a ‘Smart Bangladesh’.

The Next Level of Financial Inclusion: Entering The Digital Banking Era

A revolution in the financial services industry of Bangladesh is in the offing with every passing day, with several banks, MFS, and telecom companies gearing up to invest in digital banks through both individual investments and a consortium. The extension of the digital banking application deadline has prompted almost 20% of the traditional banks in Bangladesh to apply for a digital banking licence in a bid to increase their market penetration and bring the unbanked population under the banking umbrella. With an unbanked population of 47% in Bangladesh, digital banks hold the key to enhancing financial inclusion and extending digital banking services to the underserved and unserved population.

The rapid adoption of MFS and internet banking services has laid the groundwork for digital banks to potentially thrive, as evident by the MFS transactions, which registered a year-on-year growth of 19.5% for April 2023 relative to April 2022. The ease of availing MFS services facilitated the financial inclusion of the unbanked demographic, which mostly consisted of low-income households. The unserved and underserved populations were the biggest beneficiaries of such services, owing to convenience, cost and time savings.

Undeniably, the exponential adoption of MFS among low-income households in the last decade serves as evidence for the potential success of digital banking services. These services can effectively replace conventional banking services, which could lead to more competitive rates and reduced operating costs. This, in turn, can help create a conducive business environment for both banked and unbanked communities where digital banks can accelerate financial inclusion and economic growth of Bangladesh with the vision of bringing the majority of the population under a cashless economy.

Md. Shah Jalal

Editor

IDLC Monthly Business Review

Download View