TallyKhata

Shahadat Khan, Ph.D. Founder and CEO, TallyKhata

Interviewed By Raiyan Rabbani

Team MBR

Dr. Shahadat Khan is the founder and CEO of TallyKhata. He is the Co-chairman of BASIS Standing Committee on Fintech & Digital Payment. Dr. Khan has more than 31 years of experience, including university teaching, research and innovation, product development, and building IT-based solutions for social development. Dr. Khan started his career as a faculty member of the computer science and engineering department, BUET. He is a Canadian Commonwealth Scholar and received his Ph.D. degree from the University of Victoria, Canada. He is a frequent speaker at industry conferences and panels, holds 16 patents, and has published many articles in journals and technical magazines. He has traveled to more than 40 countries and is a hobbyist wildlife photographer. . Team MBR was in a conversation with Mr. Shahadat Khan, Founder and CEO, TallyKhata, to learn about his inspirations and vision behind TallyKhata.

Raiyan Rabbani: Since it was launched in 2020, TallyKhata has been providing an app-based digital platform for bookkeeping solutions for MSMEs in Bangladesh. Would you kindly share with us how you came up with this idea?

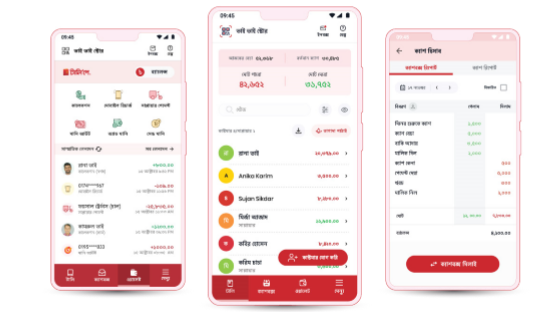

Shahadat Khan: TallyKhata is the leading digital platform. It provides bookkeeping, digital wallet and business loan services to small businesses through a simple and easy to use mobile app. Idea of TallyKhata came very interestingly. I was having a conversation with my school friend in Khilgaon, my native place. Discussing the culture of buying and selling products on credit. He had three receipts with him. One thing got my attention. Mudi shop owner made a mistake in the calculation and just lost 700 taka. That moment clicked an idea in my mind. If the shopkeeper used software, he could avoid such business loss. They use smartphones. Mobile app can solve their problem. Returning to the office, with the team we started building the solution TallyKhata for small businesses in Bangladesh.

Raiyan Rabbani: TallyKhata has successfully acquired more than 4.6 million users within a time span of slightly more than two years since its inception. What are the factors which have driven such outstanding growth within a short period of time?

Shahadat Khan: We launched TallyKhata during the Covid pandemic, and received impressive acceptance from the market. TallyKhata is the fastest growing platform for small businesses in Bangladesh. We see a few factors that help to prove it as a marketfit product. Firstly, small businesses are able to enlist their customers, record due sales and collection and send the digital invoice through SMS. This creates an Aha moment, when they find that this transaction SMS removes all sorts of disagreements with customers. Secondly, it’s an easy-to-use app in Bengali language. Simple dilam-pelam (give and receive) interface is used avoiding complex debit-credit so that the last mile less educated users can use it for bookkeeping. Thirdly, users’ transactions are secured for lifetime. So they are tension free about losing data. Moreover, TallyKhata is free and can be used without internet connection.

Raiyan Rabbani: Visa has recently selected TallyKhata to join the 2022 cohort of its Visa Accelerator Program in Asia Pacific. How is this collaboration going to help TallyKhata come up with more innovative solutions for MSMEs?

Shahadat Khan: We are proud that TallyKhata is the first Fintech from Bangladesh in this program. It’s an elite cohort of five startups from APAC. We designed the first end-to-end digital loan product with the Mutual Trust Bank in collaboration with Visa and launched to a limited number of users. We observe that small businesses face lots of challenges to get loans from banks in a traditional way. They need to provide lots of business documents, proof of business turnover etc. Also need to visit the bank branches several times. It is hassle some and time consuming. Our innovative solution will reduce all the pains. Users’ business transactions recorded in the TallyKhata are used to assess their credit eligibility. Bank can approve the loan in less than thirty minutes. We hope we can collaborate with more banks and financial institutions and scale this solution.

Raiyan Rabbani: TallyKhata plans to offer digital credit solutions for MSMEs in partnership with banks and NBFIs. To help assess the creditworthiness of MSMEs, TallyKhata will generate credit scores based on transactions and activities on the app. What are your thoughts regarding the reliability of such methods, as MSMEs are exposed to many risks which require subjective judgment?

Shahadat Khan: Everyday users record 1.8m transactions in TallyKhata platform. We use advanced artificial intelligence to analyze this data. Different businesses have different trends and patterns of recording transactions in terms of amount, entry time, location etc. Sometimes users give few entries on a trial basis. We consider the appropriate entries that match with the benchmark as per shop type and filter out outliers. We along with banks and other financial institutions have cross checked our data science outcome by visiting a number of TallyKhata users and found satisfactory. Based on TallyKhata generated credit score, we have provided loans to few users through banks. We found the result very satisfactory and there is no defaulter.

Raiyan Rabbani: Users get to enjoy the bookkeeping solutions provided by TallyKhata for free. How does TallyKhata make money out of the services it offers? Would you kindly share with us the revenue streams of TallyKhata?

Shahadat Khan: Digital adoption is always challenging especially when it is offered to a segment who are not tech savvy. They are so used to traditional ways. Though they feel that they are losing and not growing properly, they do not take initiative to upgrade themselves. Knowledge gap is the key here. So we decided that we will offer the TallyKhata app free so that users can trial it. We have two other services for them. Digital wallet and business loan through financial institutions. We hope these two service verticals will provide the estimated revenue.

Raiyan Rabbani: TallyPay has recently been launched as a digital wallet and payment service for individuals and MSMEs. How is this going to help improve the solutions TallyKhata provides?

Shahadat Khan: Our users mostly keep due sales records in the TallyKhata platform. Using TallyPay wallet, users can collect those due from their customers’ Nagad or debit/credit card. Customers do not even need to visit the shop. Users can send payment links. Customers will go to the link and can pay the desired amount. Beside this, our users can earn more by selling mobile recharge to their customer base. We are also working on a more wallet related solution that will help to increase our users’ earnings.

Raiyan Rabbani: MSMEs are the lifeblood of the economy of Bangladesh. What are your views regarding the impact TallyKhata has created in the MSME sector?

Shahadat Khan: More than 12 million msMEs contribute around 25% of our GDP. This sector employs more than thirty million people. But they always remain underserved. They do not get access to loans easily. They are not aware of how to improve their business. No affordable modern tools and technology for them. TallyKhata platform is trying to improve their situation. We are already able to digitalize their bookkeeping habits. We have also built a large database of this sector that can be used for credit scoring real-time.

Raiyan Rabbani: What are the challenges TallyKhata is currently facing in the way of its smooth operations and business expansion? How is it planning to overcome those obstacles?

Shahadat Khan: While TallyKhata and bank are trying to assess credit eligibility of this segment, mostly we found no CIB record. We need to build a comprehensive credit information bureau (CCIB) to get a real-time CIB report of this sector. This will require initiative from both the government and private sector. In many countries there are private CCIB. It will reduce the bad loans and good borrowers will be benefited since they can avail loans at lower interest rates.

CERAMICS INDUSTRY IN BANGLADESH: RISING AMIDST CHALLENGES

With a total market value of over 6,000 crores, the ceramics industry in Bangladesh has been one of the country’s fastest-growing manufacturing industries. Thanks to sustained economic growth and increasing urbanisation, the industry meets 85% of domestic demand and has the potential to become the country’s largest export industry in the not-toodistant future. With domestic sales increasing by 20% per year on average, export sales increasing by 26% per year on average in the last three years, and total production capacity increasing by around 200% in the last five years, the industry is poised for future success.

The industry benefits from rising incomes, rapid urbanisation, and duty-free access to some international markets. There is still much to be done to address the problems this industry is facing, such as uninterrupted power and gas supplies, which are essential to continue competing in global markets. If Bangladesh’s ceramics sector can get over the obstacles, it has every chance to develop and increase its contribution to the nation’s foreign exchange earnings. It stands to see what the future holds for this industry.

Md. Shah Jalal

Assistant Manager

IDLC Finance Limited

Download View