SUPPLY CHAIN FINANCE: OPTIMIZING FINANCIAL FLOWS IN BANGLADESH

Tanvir Shawkat, Senior Manager & Head of Supply Chain Finance, Corporate IDLC Finance Limited

The growing popularity of supply chain finance has been largely driven by the increasing globalization and flexibility of the supply chain, especially in large corporates. Although it actually refers to several different solutions, at its most basic it allows both the buying company and the supplier to improve their working capital in a crucial financial crisis. Henceforth, there are abundant opportunities to enter into the era of technology backed supply chain financing in Bangladesh. The market of supply chain finance of Bangladesh has the potential to grow 20 times from current size.

Overview of Supply Chain Finance

By definition, supply chain finance is a financing solution which aims to lower the financing cost and improves the efficiency of both the buyer and the seller involved in a transaction. Supply chain finance connects buyers and sellers with a financial institution, which helps the supplier to lower the financing cost and to improve efficiency. And, here the financial institution is known as a factor. It can also be named as supplier finance as it gives the supplier an opportunity to receive the payment early on their invoices. Supply chain finance gives short term credit which helps to optimize the working capital and also the liquidity of both the parties.

Typically, supply chain finance is an arrangement where financial institutions offer a lower financing cost to suppliers based on their credit rating. It offers flexibility to the buyer with the early payment discounts or to prolong the payment cycle. On the other side of the coin, suppliers get the flexibility of getting paid early through the financial institutions deducting the fee which is lower than a traditional loan and in terms of early settlement no fee is charged. Supply chain finance gives the supplier the opportunity of freeing up their working capital so that they can use the money more in operations. Supply chain finance comprises of 3 parties. The first one is the buyer or the anchor, the second party is the supplier and the third party is the financial institution acting as media between the buyer and the supplier. As supply chain financing provides benefits to both the parties, it is a win-win situation for both the supplier and the buyer.

Basically, there are 2 types of supply chain financing, Factoring and Reverse Factoring.

It is a type of supply chain financing in which businesses sell their accounts receivables or invoices to factors. It is commonly referred to as accounts receivables factoring or invoice factoring. In this arrangement businesses sell their invoices for funding their cash flows. It funds manufacturer’s working capital so that they can buy raw materials or finished goods in order to build inventory or fulfill large orders. Financial institution gives supplier a trade credit, and factors act as an intermediary between anchor/buyer and its suppliers. Factoring allows to access the fund which is tied up in accounts receivables. The corporate entity places a purchase order to its supplier, supplier will deliver the goods to the corporate anchor and then supplier will send the bill to the financial institution which shows that the order is accepted by the corporate buyer. Financial institution discounts the bill amount submitted by the supplier and pays the supplier. Finally, FIs get payment assignment from the buyers/anchors.

It is a type of supplier financing that large corporates can use to offer early payments to their supplier based on approved invoices. It is not like bill discounting where a supplier wants finance against his/her receivables. Reverse factoring allows the buyer to reduce the risk of any disruption in their supply chain as their suppliers are financed by the factor. Typically, at a lower interest cost than what factors usually offer.

Other than factoring and reverse factoring, there is another type of supplier financing which is known as distributor financing. Distributor financing is a form of financing where distributors submit their lifting order from manufacturing company as a collateral to financial institutions. Based on their lifting orders, financial institution agrees on an agreement of paying for the product for the distributor. The distributor will repay to financial institution within the agreed time period.

Global Overview & Practices

In today’s globalized business environment, which is characterized by high levels of competition, firms around the world struggle to find ways to cut costs while maximizing the efficiency of their working capital so that they do not fall behind the current market developments and ensure their viability. The concept of supply chain finance is one of the most promising tools for financing firms. The most important factors that led to the development of supply chain finance are,

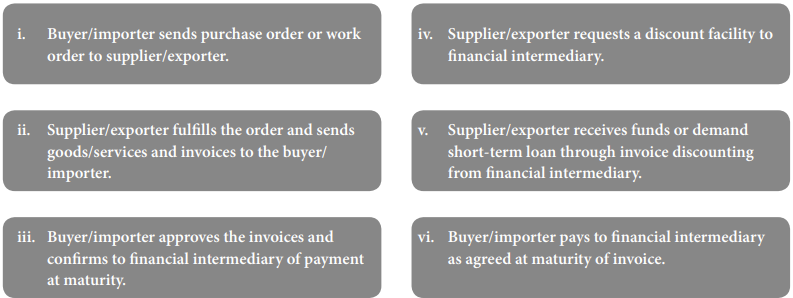

Supply chain financing requires the involvement of a supply chain financing platform and an external finance provider who settles supplier invoices in advance of maturity date of the invoice. The supply chain finance process has some steps. These are the steps usually followed in the global supply chain finance processes where technology plays a vital role. The steps are as follows,

Around the world, reverse factoring is more popular form of financing as it cuts down the cost of big corporates, which motivates them to arrange a financing option by themselves for their supplier so that the supplier can keep on supplying goods to meet large volume demands. Since both the buyer benefits from being able to extend their payment terms, and the supplier is receiving payment earlier; it has become a preferred method of financing for both sides of the manufacturing chain. The advantage of reverse factoring is that the corporates do not have to increase their debt. They are getting a flow of working capital to continue to function and meet their customers, vendors and employees’ needs.

Digital supply chain finance using block chain technology is more popular around the globe. Blockchain technology is a one of the leading innovation in the finance industry. Blockchain technology records encrypted transactions in a ledger that is distributed to network members over a period of time. Each transaction record is entered into a data block and then each block is linked to the previous block using encryption and hashing functions. In general, there are two types of blockchain data access control mechanisms based on the involvement of network members in the consensus process. The first mechanism, a public blockchain, is a blockchain in which every transaction is publicly accessible but users can remain anonymous. The second mechanism is a blockchain with permissions, where network members must have permission to join the consensus on the network. Permissions or access control are controlled by a blockchain consortium or one particular organization or private blockchain. Blockchain technology can also help improve security, service levels, reduce maintenance costs and ensure product authenticity.

Blockchain is a type of shared database that stores data in the blocks that are linked together via cryptography. The use of blockchains for supply chain finance accelerates cash flow for all parties involved. The blockchain technology architecture promises a supply chain data storage method with secure, irreversible and transparent access because the database is decentralized to many parties so that its authenticity can be evaluated consistently. This process allows decentralization of data so that no party can claim ownership of the supply chain data as their own.

Current Market Size in Bangladesh

Globally, supply chain finance is a growing source of external financing for corporations and SMEs. Supply chain finance is a win-win opportunity for all stakeholders in the supply chain ecosystem- the corporates, their suppliers and factors. Small and Medium Enterprises (SMEs) lack access to the credit and liquidity they require for their daily working capital needs. Supply chain finance allows SMEs to access credit at a lower cost with minimal documentation

and lesser collateral. The current market size of supply chain finance is approximately BDT 4,000 crore including the banks and the NBFIs. But, it has the potential to grow as the opportunities are huge. But, the current market size is still very low in the context of Bangladesh due to lack of penetration of FIs.

Supply chain finance is really popular around the globe including in our neighboring countries. Countries like India and Sri Lanka provided supply chain financing business with policy backups and proper monitoring to increase accountability and ensure credibility. In Bangladesh, the most popular form of supplier financing is factoring. Reverse factoring is not widespread because, the corporate entities are not willing to take the extra cushion for the suppliers. In Bangladesh, there are huge opportunities for supply chain finance and the regulatory bodies are encouraging to invest in this sector. Supply chain financing has the potential to become the cash cow, as the revenue generating sectors are more here. As a result, the banks and NBFIs are trying to capture the market of supply financing. At present, we can see that the commercial banks are also entering in the supply chain financing. They are targeting the ready-made garments sector, large corporates, MNCs, poultry industry, pharmaceutical industry, telecom industry and SME sector. Financial institutions have already penetrated the market.

Penetration of Banks and NBFIs in Bangladesh Market

Supply chain finance is a trip-art solution between the buyer (mostly multinationals) and a Financial Institutions (FI), which allows suppliers to join a programme to discount their receivables to the FI which is delivered to and accepted by the buyer. The solution provided by the FI is that they will make an arrangement with the buyer and the supplier so that supplier can get enough fund to continue production.

Supply chain finance was introduced in Bangladesh by IDLC Finance Limited in 1999. In 2006, United Finance Limited and LankaBangla Finance Limited entered the market of supply chain finance. IPDC Finance Limited and Eastern Bank Limited started their supply chain operation with a small portfolio of supply chain finance, although it was discontinued after a while. After 2016, commercial banks started to introduce this facility and created small portfolio of their own. In 2017, IPDC Finance returned to the market with new strategy with a vision to capturing the lion’s share of the market. IPDC is the first in Bangladesh who have introduced digital supply chain financing using block chain technology. During the pandemic, IPDC has outperformed in supply chain finance market.

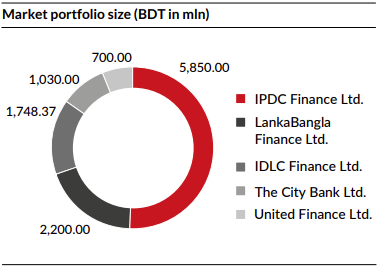

Bangladesh has abundant opportunities in the market of supply chain finance. The market will foresee a tremendous growth in a few years. The current portfolio size of Bangladesh comprising all the banks and NBFIs is around BDT 4,000 crore where IPDC is leading in the market.

Supply chain finance is cheaper than any other form of traditional financing because FIs fix price based on the risk exposure for every loan. For further security,FIs do have other mechanism to minimize risk from supplier financing.

Supply Chain Finance in IDLC

Supply chain finance was introduced in Bangladesh by IDLC Finance Limited in 1999, at a time when it was an unchartered financing territory for the FIs. IDLC gives the buyer the competitive advantage by providing them a secured loan which improves their balance sheet performance, fulfills their working capital need, and expands their business opportunities. The management of IDLC aspires to touch BDT 500 crore landmark in next 3 years and has the vision to become the market leader within next five years. The current portfolio size of IDLC is BDT 1,748.37 mln. The products that IDLC offers are,

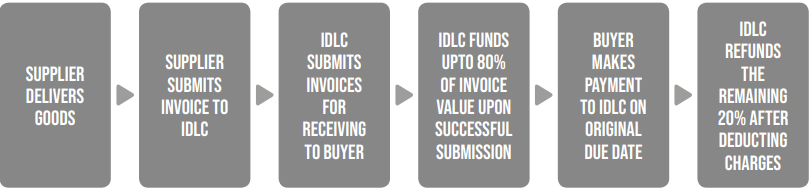

Factoring/Bill Discounting: Factoring process starts with submitting the invoice to IDLC from supplier end and IDLC would pay up to 80% of the invoice amount after successful submission. And, after that buyer will repay to IDLC on the due date. After the repayment of the loan, IDLC will refund the remaining 20% after deducting all the charges.

The first feature of factoring is the loan tenure will be 1 year from the sanction date. IDLC will provide maximum 80% of advance financing against verified invoices and the loan limit will be justified with the sales. The credit period will be decided based on the supplier’s cycle of cash flow.

Reverse Factoring: Reverse factoring is when directly the suppliers of the corporates approaches to IDLC for financing to their supplier so that they can get a payment discount. Supplier will submit the invoice to IDLC and IDLC will pay 100% of the invoice amount to their supplier. And thus, it will create a loan for initial supplier and the supplier would repay the loan within the due date. And the tenure of the loan will depend on the business modality. All the charges will be paid from the initial supplier’s end.

MOU Based Factoring/Bill Discounting: This product is offered to the large corporates to provide working capital to their nominated 15 of 32 Payment assignment Provides product lifting order Work order submission to factor Submits lifting order IDLC verifies work order with buyer Verifies the order and Advance Payment IDLC advances upto 60% of invoice value Lift goods Delivery of goods/ services Payment within the credit period Payment directed to IDLC on invoice maturity suppliers. The facilities of MOU based factoring will be same as regular factoring. The main difference between MOU based factoring and factoring is the memorandum of understanding between corporate and IDLC. Corporate will take all the responsibility of the loan, as the suppliers are nominated by them. For MOU based factoring, IDLC will pay 100% of the invoice. Corporates will repay the loan within the due date and all the charges will be paid by the corporate.

Distributor Financing: For distributor financing, distributor will submit product lifting order to IDLC. After that, IDLC will verify the lifting order and will pay advance to the distributor. Distributors will repay the loan within the credit period.

For distributor financing, loan limit will be finalized based on corporate suppliers’ comfort and sales of the distributor. The loan tenure will be same as factoring. The main difference with factoring is distributor financing offers 100% advance payment to the buyer on behalf of the distributor and there is a security requirement for 2 mln and above.

Work Order Financing: Work order financing is a method of financing which facilitates credit to contractors and suppliers to participate in tenders under government/semi-government organizations. IDLC will receive work order or payment assignments from the supplier and will verify. Depending on the verification, IDLC will offer up to 60% of advance financing against verified work orders and payment assignments from the buyer. Credit period is set based on the client’s cash flow cycle.

Apart from these, IDLC also caters lease, commercial vehicle financing (CVF), term loan, and stimulus loan to the existing factoring availing customers.

PEST Analysis

Political Factors:

1.Judiciary Independence: In the matter of commercial and business decisions, judiciary of the country is important to a large extent.

2.Political Governance System: Supply chain finance program can make strategies based on the stable political environment.

Social Factors:

1.Attitude towards Savings: If the average savings rate is high, it can be determined that at present the people of that country is spending less and if the savings rate is lower it does mean that spending is higher and that country is suitable for 16 of 32 business at this moment. The attitude toward savings rate can impact the type of consumption as well as the frequency and magnitude of consumption.

2.Demographic Trend: The demographic trend is one of the key factors in demand forecasting of an economy.

Economic Factors:

1.Fiscal and Monetary Policies: Fiscal and monetary policies will impact on the rates of the offered products of supply chain finance.

2.Price Fluctuations in both Local and International Markets: Supply chain financing program should consider the fact that at deficit levels of any country in an emerging economy can lead to rampant inflation and serious risks of currency depreciation.

3.Employment Rate: If the employment rate is high then it will impact supply chain finance in two ways – it will provide enough customers for supply chain finance products, and secondly it will make it expensive for SCF Program to hire talented & skillful employees.

4.Inflation Rate: The inflation rate can impact the demand of SCF Program products. Higher inflation may require SCF Program to continuously increase prices in line of inflation which could lead to lower levels brand loyalty and constant endeavors to manage costs. Cost based pricing could be a bad strategy under such conditions.

Technological Factors:

1.Level of Acceptance of Technology in the Society: Before launching new products, level of acceptance of technology in the society should be figured out.

2.Integration of Technology into Society & Business Processes: Digital solution in supply chain finance will increase the efficiency level of lenders and thus it will increase the market size of supply chain finance in Bangladesh.

3.Transparency & Digital Drive: Supply chain finance program can use digitalization of various processes to overcome corruption in the local economy

4.Empowerment of Supply Chain Partners: Supply chain finance program should analyze areas where technology can empower supply chain partners. This can help supply chain finance program to bring in more transparency and make supply chain more flexible.

Challenges and Way Out

Supply chain financing ensures that all parts of the manufacturing process can stay in sync. A delay in the production impacts the final sale of the products and could cost the manufacturer money from loss of sales. By receiving the payment ahead of time, the supplier can deliver their portion of the chain efficiently without any additional cost to the buyer. Although they are charged a fee for the cash in advance, this is small in comparison to what the price would be if they were to default on the commitment to produce entirely. Still a number of multinational corporations and local corporates are somehow not willing to come into this agreement with FIs and their suppliers.

Though supply chain finance has a huge potential in Bangladesh, but still the market is very small. The reason behind it is the lack of understanding about the concept of supply chain finance among all the parties. Not only the knowledge of supplier and anchor but also the factor is lacking of adequate knowledge of the products of supply chain finance. Corporates are also not coming forward in backing up their suppliers. That is why suppliers are suffering with the high interest rates. The suppliers are the SMEs who actually need funding to run their operation. But, as the products of supply chain finance are not being introduced to them properly and the corporates are not coming forward, the suppliers have to take fund at high rate. In Bangladesh, there is lack of regulatory guidelines in the area of financing. Insufficient laws and regulations have narrowed down the market of supply chain finance. Recently, Bangladesh Bank has issued guidelines on local factoring using digital platform.

Supply chain finance is one of the growing financing technologies which can reduce trade finance traffic. Some commercial banks in Bangladesh have recently introduced supply chain finance. Their target customers at present are regular suppliers, service providers of multinational corporations (MNCs) and large local companies. Reverse factoring might be a solution for the financing vehicle of Small and Medium Enterprises (SMEs) sector in Bangladesh. Government and central bank’s initiative, cooperation from MNCs and local corporates and FIs focus on this product can thrive the growth of SCF in Bangladesh.

The writer of the content is working as a Senior Manager & Head of Supply Chain Finance in IDLC Finance Limited and he can be reached at Shawkat@IDLC.com

Supply Chain Finance: Optimizing Financial Flows in Bangladesh

SUPPLY CHAIN FINANCE: Optimizing financial flows in Bangladesh

Supply chain finance is deemed as a win-win opportunity for all stakeholders in the supply chain ecosystem- the corporates, their suppliers and the factor. Rather than waiting on its large customers to pay invoices, the supplier can submit invoices to financiers for early payment. In turn, this provides immediate access to liquidity which can help the supplier keep operating in a “business as usual” environment in any business climate. These along with factors such as proper fund utilization, authenticity of cash flows of borrowers, etc. have garnered much popularity in the country for this particular financing vehicle.

IDLC Finance Limited pioneered and introduced supply chain finance in 1999. Despite its commencement 23 year back, this particular segment of finance is yet to live up to its potential. The clear concept of supply chain finance is still absent among customers in our country. Additionally, the corporate buyers lack interest in supporting their suppliers and as a result, the suppliers end up availing loans at a high rate.

From regulatory point of view, Bangladesh does not have any specific policy guideline or legal framework for supply chain finance. Nor there is any legal framework for the security of the payment for these products. Hence, for this segment to thrive, the driving force needs to come at policy levels. Meanwhile, corporate buyers have to come ahead and support their suppliers by means of reverse factoring.

RIFAT ISHTIAQ KHAN

Manager

IDLC Finance Ltd