MUTUAL FUND: A GLOBALLY POPULAR INVESTMENT VEHICLE YET TO HAVE A STRONG FOOTHOLD IN BANGLADESH

MD. ITRAT HOSSAIN, CFA Investment Analyst, Portfolio Management and KAZI UMME SUMAIYA, CFA Investment Analyst, Portfolio Management IDLC Asset Management Ltd

Investment is the prerequisite for wealth accumulation. Traditional savings instruments like bank deposits hardly beat inflation and resultantly do not increase the real value of wealth. Higher return yielding investment securities like equities, bonds etc. can increase the wealth in real terms. However, investment in such risky securities require extensive knowledge, research and time, often out of the capacity of individual investors. Mutual fund has evolved to the investors’ rescue here by offering professional fund management service with the benefit of diversification and lower investment cost. Globally, mutual fund is one of the most preferred investment tool for investors. Though mutual fund was first introduced in 1980s in Bangladesh, the industry growth has been lackluster. It requires structured initiatives for the proliferation of the industry. This article intends to articulate the issues revolving around the development of the industry in Bangladesh. The discussion would start with a preview of global mutual funds industry, followed by a study of the explosive growth in Indian mutual funds industry, putting the local industry in a historical context and finally beckoning a way forward.

Global Mutual Fund Industry

The basic investment theme of mutual funds is pooling money from small investors and investing that fund across different asset classes, achieving diversification. The origin of such investment concept has been traced back in 1774 in Europe when a Dutch merchant Adriaan Van Ketwitch created an investment trust. The name of Van Ketwich’s fund, “Eendragt Maakt Magt”, translated to “unity creates strength”1. However, the first modern day mutual fund is said to be created in 1924 through the arrival of Massachusetts Investors’ Trust in Boston. The mutual fund industry has gradually developed since then through the introduction of varieties of mutual funds in terms of investment styles and evolved as one of the major investment tools of modern day in developed world. The global asset under management (AuM) stood at USD 89.0 tn as of 20192, which is higher than global equity market capitalization of USD85.0 tn3.

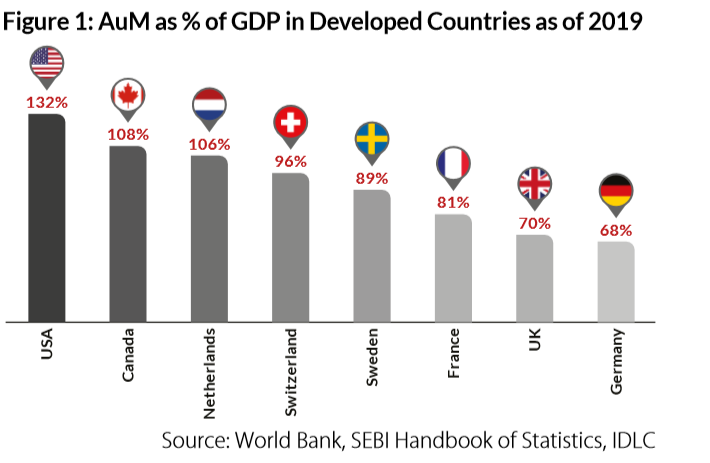

In developed countries the size of the industry in terms of AuM has sometimes become even larger than the economy itself. Figure-1 depicts the enormous size of mutual fund industry in developed countries in comparison to their economy as of 2019.

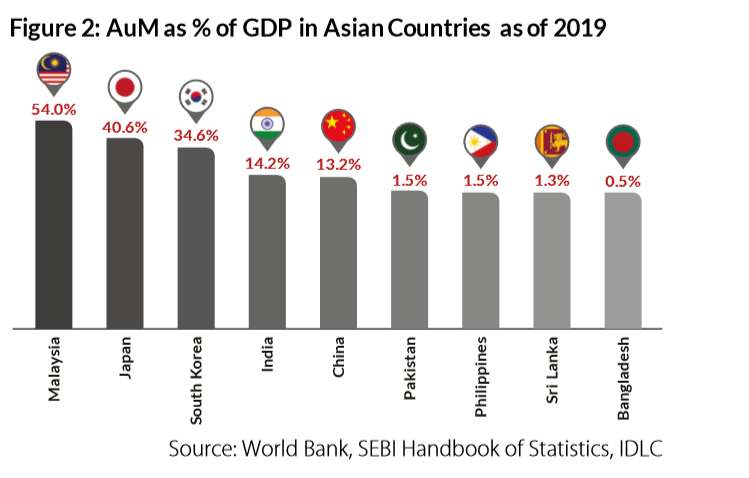

The largest mutual fund industry in the world belongs to United States of America (USA). USA saw a faster penetration of mutual funds in 1990’s. Only 5.7% of the households owned mutual fund in 1980 in USA, which dramatically increased to 45.7% by 20004. However, the penetration level has not changed much since then. As of 2019, 12.9% of the household financial assets is invested in mutual funds in USA, which is 20.1% in Canada.5 Among Asian countries, Malaysia (54.0%), Japan (40.6%), and South Korea (34.6%) have been successful in building a sizeable mutual fund industry compared to their economy. The southern part of the region is still lagging behind. However, India (14.2%) in this regard showed tremendous progress compared to its regional peers like Pakistan (1.5%), Sri Lanka (1.3%) and Bangladesh (0.5%) (Figure 2).

Development of Mutual Fund Industry in India, an Exemplary Case

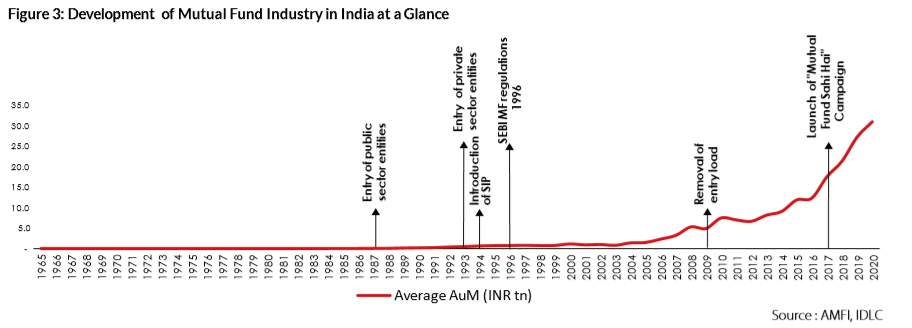

Even if India’s Mutual fund industry is still small as percentage of its GDP compared to the developed world, the progress the country has made so far in this industry is commendable. The industry started its journey in 1963 with monopoly of Unit Trust of India (UTI). Now, there are 44 asset management companies managing an average net asset size of INR 31.0tn (USD 433.48 bn) as of Dec 2020. It took the industry around 50 years to accumulate the first INR 10 tn, while the next INR 10 tn was amassed within 5 years6.

.

.

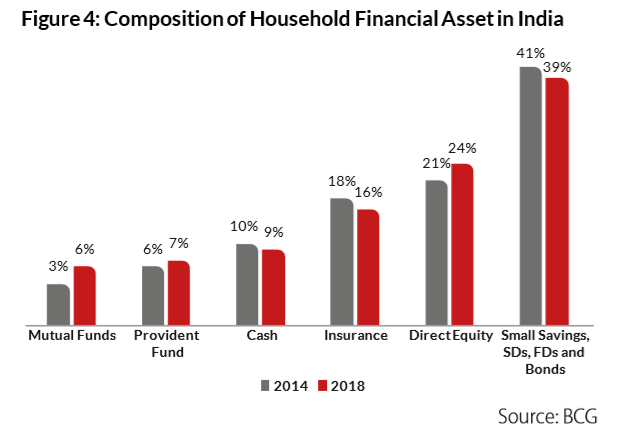

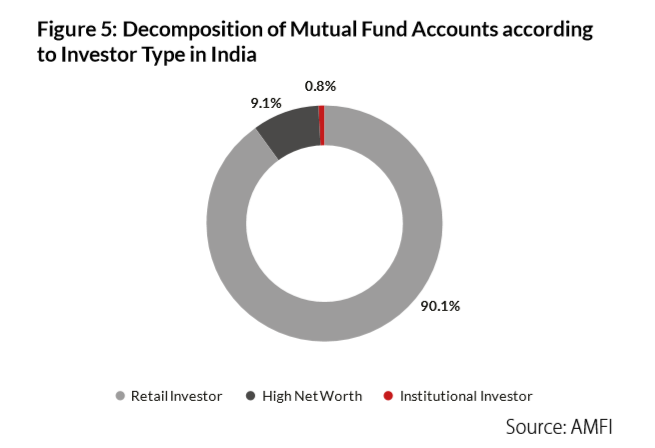

Figure 3 depicts the evolution of mutual fund industry in India marking the major events. The mutual funds AuM in India grew at a CAGR of 21.0% approximately during 2003-2020, riding on a number of stimulating factors like industry reform initiatives, introduction of innovative products catering to customer needs and mass awareness campaigns. All these factors led to increased penetration of mutual funds among Indian households, expanding the share of mutual fund in household financial asset to 6.0% in 2018 from 3.0% in 2014. During this period, mutual funds grew at a CAGR of 31.0%, highest among the other financial asset categories held by households (Figure 4)4. According to Reserve Bank of India, the share of mutual funds in household financial asset stood at 7.0% as of March 2020. Retail investors account for 90.1% of mutual fund accounts in India with an average ticket-size7 of INR 69,185 (USD 942.86) per account (Figure 5). Retail investors are also leading in terms of AuM by holding 53.2% of the total industry asset size as of February 2021. Equity mutual funds derive 88.0% of their assets from individual investors. On the other hand institutional investors dominate the liquid and money market schemes (84.0%), debt oriented schemes (61.0%) and ETFs (91.0%)8 .

The factors that contributed to the proliferation of mutual funds in India are summarized below:

Government incentives: Government of India (GOI) has provided tax incentives for investment in mutual funds for a long-time which attracted the investors to this industry. Dividend and Capital gains from investment in equity mutual funds held for more than one year were fully tax exempted till 2017 in India.

Systematic Investment Plan (SIP): SIP is believed to be a major driver of increased retail participation, which allows investors to start investment in mutual fund schemes with a ticket size of only INR 500.0. As of February 2021, mutual fund SIP accounts stood at 36.3 mn, mobilizing a total of INR 75.3 bn in that month alone. Total fund collected through SIP in FY’20 was INR 1.1 tn, which was INR 439.2 bn in FY’17; indicating a staggering 3 years’ CAGR of 31.6%.

Product variety: The asset management companies (AMCs) in India offers varieties of mutual funds focusing on different liquidity needs, return preferences, risk appetite and investment objectives of investors e.g. balanced funds, growth funds, different maturity based bond funds, money market funds, retirement savings funds, infrastructure funds, etc.

Presence of a structured and active association: The Association of Mutual Funds in India (AMFI), the association of all the registered AMCs in India was established in 1995 under the purview of Securities and Exchange Board of India (SEBI). The aim of the association is to develop the mutual fund industry on professional and ethical ground with a view to protecting and promoting the interests of mutual funds and their unit holders. The association has been vested with appropriate power to strongly regulate the industry of INR 31.0tn. No mutual fund agents, distributors and brokers are allowed to sell or recommend a mutual fund without a registration number from AMFI.

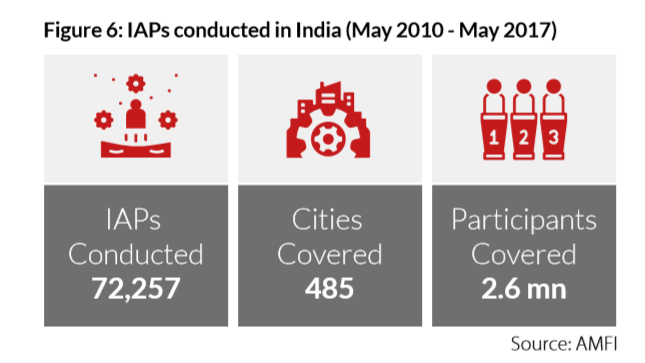

Robust awareness campaigns: SEBI has mandated that the AMCs need to spend 2.0 basis points of their total AUM for Investor Awareness Program (IAP), half of which (1.0 basis points) will be distributed to AMFI. AMCs have been conducting IAPs following a uniform structure as recommended by AMFI and are required to provide program schedule for each fortnight to AMFI in advance. AMCs in India has run 72,257 IAPs across the country in 8 years (Figure 6).

Mutual Fund Industry of Bangladesh, a Journey of 40 years

The journey of mutual fund industry in Bangladesh started in 1980 led by state owned Investment Corporation of Bangladesh Limited (ICB). For a long period of time ICB operated as the only asset manager in the country offering both Closed and Open end Mutual Funds. Following the economic liberalization in late 80s and 90s private sector participants entered the industry with a promise of specialized products. In order to achieve a perspective of the mutual fund industry, we have divided the history of development of the industry in three generations. The first generation mutual funds are those that came during 1980-1999. The second generation encompasses the time period of 20002014. The third generation funds came in 2015 and later. These generations are categorized by some common characteristics which will be discussed as we proceed.

First Generation (1980-1999)

During 1980 – 1999, a total of 10 mutual funds came into operation. 9 of those mutual funds were managed by ICB and only 1 by the then Bangladesh Shilpa Rin Shangstha. First ICB Mutual Fund was the first Closed end mutual fund launched in Bangladesh in 1980. On the other hand, the first Open end mutual fund was ICB Unit Fund, launched in 1981.

Though the first ICB Mutual Fund was under subscribed at the time of its floatation, the first generation of mutual funds were quite successful in terms of investors’ wealth generation.

The First generation mutual funds were mainly Closed end and did not offer any specific style to cater individual demand, given the early age of the industry. Yet, they played a vital role in creating a foundation for the industry in Bangladesh.

Second Generation (2000-2014)

The second generation funds mark an influx of private asset management companies, starting with Asset and Investment Management Services of Bangladesh Limited (AIMS). AIMs’ first mutual fund AIMS First Guaranteed Mutual Fund (AIMS1STMF) was the first mutual fund offered by a private sector firm in Bangladesh, in 2000. The fund was unique also in another sense that it was the only fund offering guaranteed capital protection.

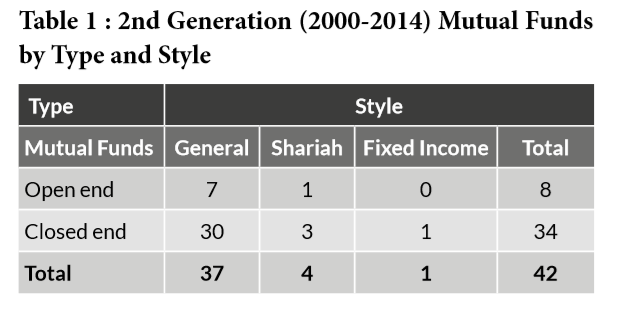

The Second Generation funds were mostly Closed ends. A total of 42 funds debuted during 2000-2013, 34 of which were Closed end funds (Table 1).

Although, most of the funds were of general style, 4 Shariah funds and 1 Fixed Income fund were launched during this period.

The second generation of mutual funds got a boost from the 2009-10 bull-run in capital market. At the peak of the market in 2010, 14 mutual funds debuted in a single year. Momentum in new mutual funds offerings slowed after the bull-run and number of new offerings declined every year up until 2015.

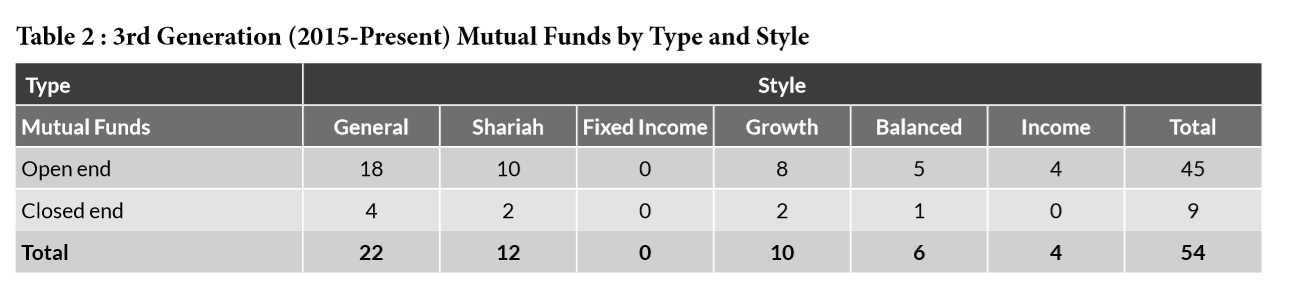

Third Generation (2015-Present)

From 2015 to onwards, mutual fund industry revived with a new vigor. The most defining characteristics of this generation is the proliferation of Open end funds and introduction of different style oriented funds. During last 6 years, 54 new funds came in already, whereas a total of 42 funds came in the entire span of 15 years of Second Generation. 45 of these funds are Open end, and 32 of the funds have some Style orientation (Table 2). Chronic undervaluation of Closed end funds were one of the key reasons for newer AMC’s orientation to Open end funds, while tapping new customer class incentivized adoption of various Styles.

Shariah has emerged as the most dominating among the styles with 12 new funds offerings, followed by Growth funds with 10 new offerings.

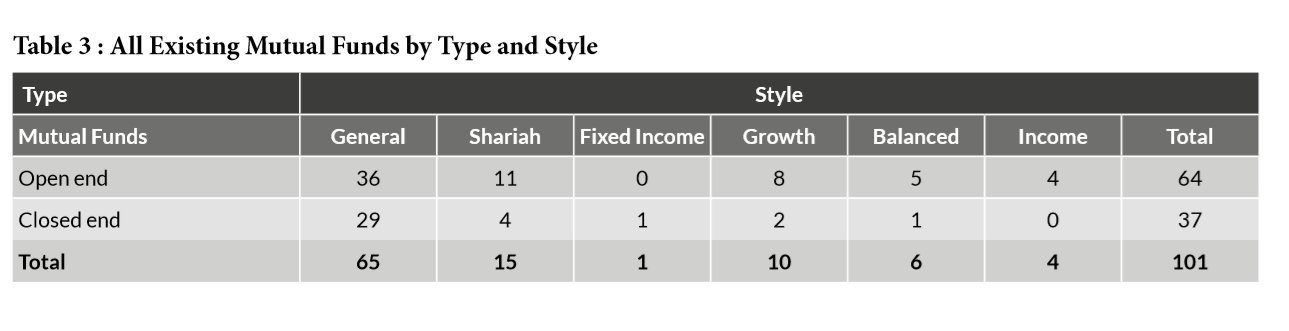

Number of Existing Mutual Funds

Overall, there are a total of 101existing mutual funds in Bangladesh, of which 64 are Open ends and 37 are Closed ends (Table 3).

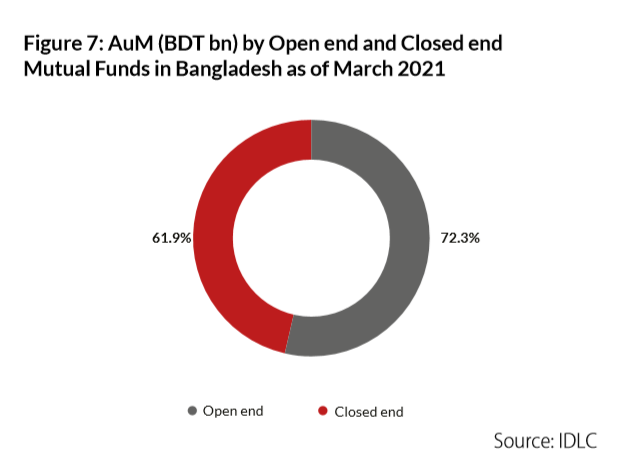

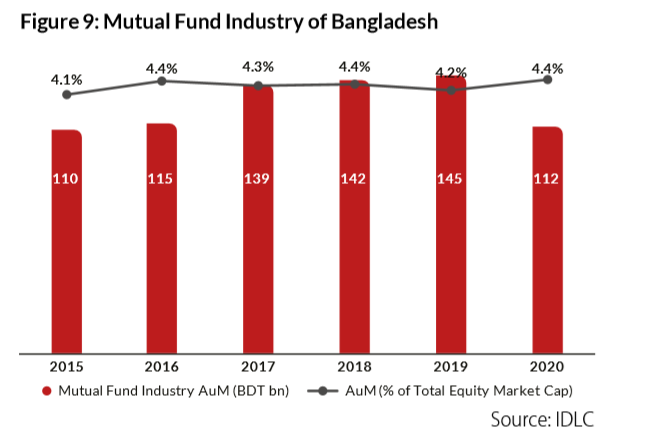

Industry AuM

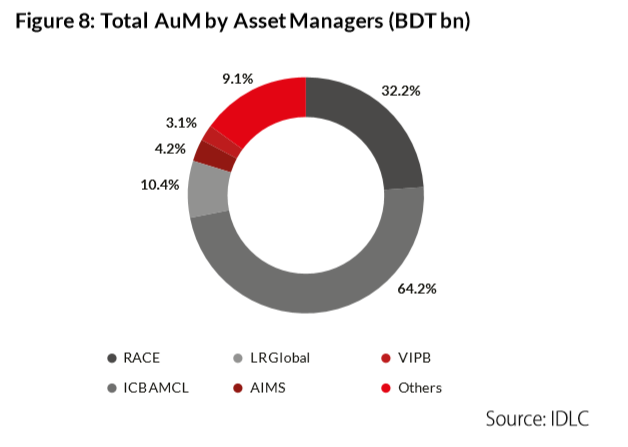

As of March 2021, there are 29 asset management companies who are managing a total sum of BDT 134.2 bn under 101 mutual fund schemes. ICB Unit Fund alone has an AuM of BDT 30.3 bn, while other Open end funds collectively have AuM of BDT 42.0 bn combined. The Closed end funds have an aggregate AuM of BDT 61.9 bn (Figure 7). ICB and ICB AMCL remain the largest asset manager controlling almost 50% of industry AuM.

Return Generation

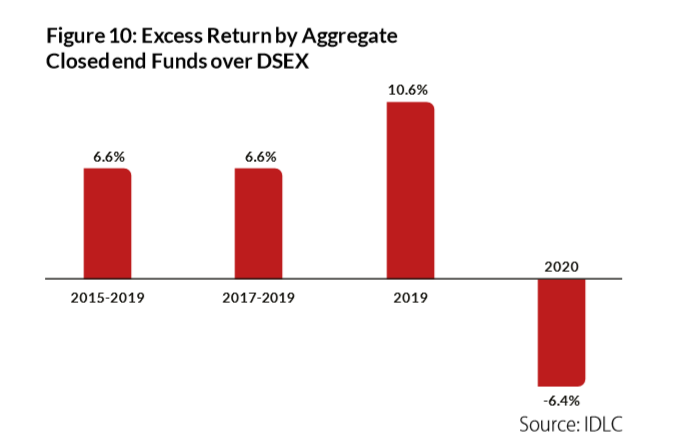

In aggregate,Closed end mutual fund industry has generated excess return over DSEX, justifying the benefits of professional fund management services.

During 2015-2019, Closed end funds in aggregate generated an excess return of 6.6% over DSEX. During the bearish market of 2018 and 2019, the funds generated an excess return of 8.6% and 10.6%, respectively; representing the industry’s capacity to offer value protection in tough times. However, the industry could not outperform the market during 2020. (Figure 10).

On an average, Open end mutual funds also generated excess return over the market return. During 2018 and 2019, all Open end funds generated an average excess return of 7.5% and 9.6%, respectively. In 2020, the Open end funds beat the market marginally with an average excess return of 0.4%.

Mutual Fund Industry in Bangladesh: The Way Forward

Mutual Funds industry is awaiting a takeoff. There has been a demand for a stable capital market product in Bangladesh for a long while. Innovative and prudent strategies from asset managers, their openness to learning curve and policy support can spark a boom in the industry.

We identify some key factors that could play a major role in putting mutual fund industry on a fast track.

1. Favorable Tax Regime: Globally, tax incentives have always worked as a major tool to push an industry’s growth. Currently in Bangladesh, income from mutual funds are tax free up to an amount of BDT 25,000 for Open end funds. Full tax exemption on both capital gain and dividend can be used as an incentive tool for the growth of mutual fund industry in Bangladesh similar to other countries. It becomes more beneficial in terms of government’s revenue collection if tax is imposed once the industry reaches the maturity stage. It will not only encourage the investors to direct their savings towards capital market, but also ensure market stabilization, promoting long term value oriented investing.

2. Product Diversification: With the economic development of Bangladesh, the financial fortune of its population is improving. With financial development and inclusion, demand for diversified and specialized financial productsis also growing. In addition to the existing equity market, a fully functional debt market is necessary for increasing the depth of the capital market. Globally, debt market is much bigger than the equity market and also is the major financing source of development projects of government. With a structured debt market in place, products like bond funds can be a major tool for channeling individual savings. In India, 48.7% of the total AuM of mutual fund industry comes from debt funds. Appropriate policy support is needed for the development of debt market and introduction of diversified investment products.

3. Popularizing Systematic Investment Plan (SIP): Systematic Investment Plan is a way of investing in a mutual fund scheme where the investor can invest a small sum of money on monthly basis for a fixed time period. As investors can start investing with a very small amount, it helps build a habit of investment from an early age and enjoy the benefit of compounding. It also helps defy market volatility through taka cost averaging benefit. SIP AuM accounts for 12.8% of the total AuM of India9. Couple of AMCs are already offering SIP in Bangladesh. Popularizing SIP with thorough communication on its benefits will help attract more people to invest in mutual funds.

4. A Strong and Active Association: The AMC industry needs a vocal and active association of asset managers. As the industry is still small in comparison to other market participants, the AMCs need to be unified to take the industry to the new heights. An active association can play a vital and strong role in creating investors’ awareness and work to complement the policy initiatives taken by Government and regulatory bodies. The association can actively run common investor awareness program for the overall growth of the industry. An initiative called “Mutual Fund Sahi hai” taken by AMFI can be an example here.

5. Encouraging Collective Growth: For the overall growth of the mutual fund industry, it is essential to build investors’ confidence in it by ensuring transparency in the industry and making investment hassle-free. AMCs can be evaluated based on a number of criteria e.g. fund performance, services provided, contribution to raising investment awareness, transparent disclosure etc. and can be assigned a rating accordingly. AMCs management fees can be tagged with the rating so that AMCs with best rating can be rewarded for their contribution to the overall industry growth. This will encourage healthy competition in the industry promoting quality growth as well as help the investors to take more informed investment decision.

A vibrant capital market is a precondition for a thriving economy. Through increased penetration of mutual funds individual savings can be channeled to the capital market under professional supervision. It will not only help the investors to reap the benefits of long term investment in capital market, but also ensure the quality of investment directed towards the market. By addressing the factors mentioned above with appropriate initiatives, greater penetration of mutual funds can be ensured with mutual funds grabbing a sizeable share in the households’ financial assets composition of Bangladesh.

1. Investopedia.com

2. Global Asset Management 2020: Protect, Adapt, and Innovate by BCG

3. CNBC

4. Statista.com

5. Data.oecd.org

6. Unlocking the INR 100 Trillion Opportunity - asset management industry in India by BCG and AMFI

7. Ticket size is computed as assets managed for a scheme category/number of accounts for that category.

8. Association of Mutual Funds in India (AMFI)

9. As indices scale new highs, SIP investments are on a roll- The Economics Times

MUTUAL FUND: A GLOBALLY POPULAR INVESTMENT VEHICLE YET TO HAVE A STRONG FOOTHOLD IN BANGLADESH

Mutual Fund: Potential to be popular household financial instrument in Bangladesh

Mutual fund is most preferred by the investors worldwide not only because of its higher return yielding nature compared to other household assets but also because it assists the investors by offering professional fund management service with the benefit of diversification and lower investment cost. Even though mutual fund was first introduced in 1980s in Bangladesh, the industry growth has not been very noteworthy.

In developed countries, the size of the industry in terms of Asset under Management (AuM) has sometimes become even larger than the economy itself. The largest mutual fund industry in the world belongs to United States of America (USA). As of 2019, 12.9% of the household financial assets are invested in mutual funds in USA. Among Asian countries, Malaysia (54.0%), Japan (40.6%), and South Korea (34.6%) have been successful in building a sizeable mutual fund industry compared to their economy. The southern part of the region is still struggling. However, India (14.2%) in this regard showed tremendous progress compared to its regional peers like Pakistan (1.5%), Sri Lanka (1.3%) and Bangladesh (0.5%). If the factors behind the tremendous progress of India considered, it can be observed that initiatives such as government incentive, systematic investment plan, product variety, Presence of a structured and active association etc. played a vital role.

On the other hand, this industry of Bangladesh is yet to boom. Innovative and prudent strategies from asset managers along with policy support can take this industry to a new height.

Sushmita Saha

Assistant Manager

IDLC Finance Limited