RESILIENT TURN AROUND OF SMES FROM THE ADVERSE IMPACT OF COVID-19

Credit Risk Management, SME, IDLC Finance Ltd.

The fisheries and livestock industry plays a vivid role in the economy of Bangladesh. The country is ranked amongst the top inland fish producing nations in the world. Currently, 143 fish farms are directly operating through government ownership and 1,038 firms are operating under private ownership and the livestock’s contribution to GDP stands at 1.43% in FY 2019-20. Conspicuously, the share of the animal farming sub-sector in GDP is trivial, yet this sector provides employment opportunity to more than 70% of the rural and small households.

Cluster Definition

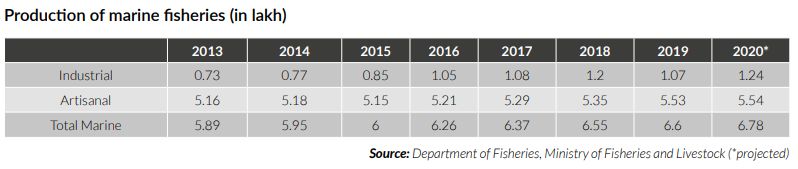

The production sources of fisheries can be classified into three sources.

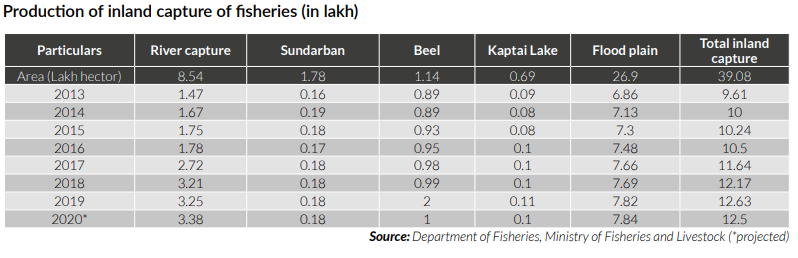

1.Inland capture of fisheries

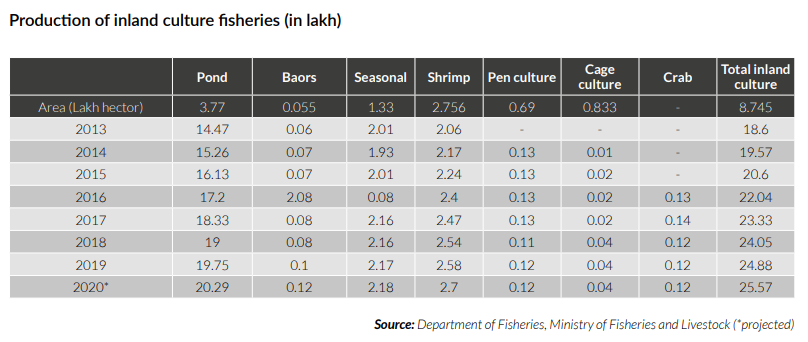

2. Inland culture of fisheries

3. Marine fisheries

Impact of COVID-19

COVID-19 had a significant impact on fisheries’ products. The price of the fish dropped significantly in the first few weeks of April when the government had declared a nationwide lockdown. At the lowest point of crisis, the price of a kilogram of pangasius, one of the highest consumed fish, in Mymensingh’s retail markets had plummeted from BDT 120/kg to BDT 50/kg. Many fish farmers in Kishoreganj, Mymensingh and Netrokona were unable to sell fish due to the unavailability of transportation. Moreover, in the northwest region of the country, hatcheries reduced their production by at least 30-40%. The dairy farmers also faced severe transportation issues for delivering the daily produced milk. Dairy farmers approximately incurred a loss of BDT 189 million every day during the pandemic crisis.

Path to Recover and Future Prospects

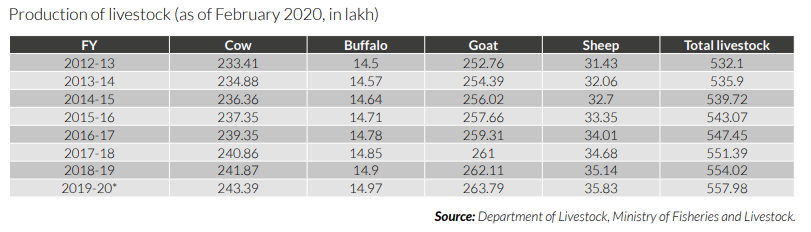

Even after all the setbacks, the Prime Minister of Bangladesh declared in July 2020 that the fish production had increased by 50% in 11 years. People now consume 62.58 grams of fish against the daily demand of 60 grams per capita. Moreover, in 2020, Bangladesh registered a total output of 4.4 million tons of fish. Similarly, the production of livestock products has increased and the per capita availability of milk and meat rose to 165.07 ml/day and 124.99 gm/day respectively in FY2019-20. The following segment highlights some of the initiatives taken from the part of the government to recover the loss occurred due to the crisis.

-Providing financial assistance stimulus package of BDT 5,000 crore for livestock, fisheries and agro-based rural enterprises at 4% interest rate.

-The government has set aside BDT 3,190 crore for the livestock and fisheries sector in the proposed budget for the fiscal year 2020-21, which is 26% higher than the budget for the previous fiscal year.

The prospects of the fisheries industry are very delightful. In September 2020, Bangladesh achieved the second spot among the highest freshwater fish producing countries in the world. If Bangladesh can capitalize on its whole marine boundary, then the marine production of the fisheries will see a sharp increase. The international market is another untapped opportunity for Bangladesh. This could open a massive market for fisheries’ products. Bangladesh also has a bright future in livestock industries as several steps like- providing one stop services, vaccination facilities and other initiatives have been taken which ensures a good future prospects forthe fisheries and livestock industries.

The commercial vehicle market refers to vehicles used to transport goods and passengers. It includes trucks, buses and coaches etc. The country being a flat plain, all three modes of surface transport, i.e. road, railway and water are widely used in carrying both passengers and cargo. It is estimated that mechanized road transport carries about 70% of the country’s total passenger and cargo volume.

As the economy was growing very fast [growth rate forecasted (FY 2020) by World Bank was 7.2%] before the countrywide lockdown (due to COVID-19), the increase in economic activities created a huge demand for different types of motorized vehicles and accessories. Later, during the post lockdown era, the government has forecasted GDP growth of 5.2% FY 2020 and this resulted in the reformation of economic activities. The economic activities lead the demand of cars, motorbikes, commercial vehicles and vehicle accessories in Dhaka, Chittagong, Jashore, Satkhira, Kushtia, Bogra and Sylhet.

Impact of COVID-19

The automobile sector had incurred losses worth BDT 6,000 crore in the three months of COVID-19 countrywide lockdown as per the statement of Bangladesh Automobiles Assemblers and Manufacturers Association (BAAMA). During the lockdown period, importing, trading and manufacturing of vehicle accessories were closed; transportation services were almost closed (excluding basic need goods transportation) that led to around 90% decrease in sales of vehicle accessories. Even personnel who were directly involved in this sector including owners of trucks and servicing industries (workshop and light engineering), employees (drivers and helpers) had fallen in a crucial situation.

Market Insights

-The sales of commercial vehicles are increasing fast in Bangladesh with at around 35 %

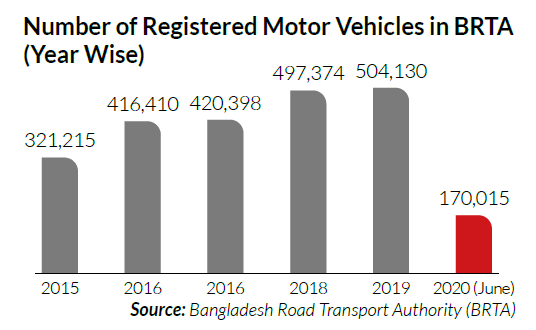

-Around 35,000 commercial vehicles such as buses, trucks, auto-rickshaws, cargo vans, human haulers, pickups and tankers were sold on an average every year since 2017, way higher than the 2,000 rate 10 years ago, according to data from Bangladesh Road Transport Authority.

-At present, the market size of commercial vehicles is about BDT 4,200 crore whereas it was about BDT 2,000 crore a decade ago.

-Runner Automobiles is taking preparations to invest BDT 433 crore to set up an automobile assembling and manufacturing plant inside Bangabandhu Sheikh Mujib Shilpa Nagar from Bangladesh Economic Zones Authority (BEZA) to grab a share of the rapidly growing commercial vehicle market.

-The plant is expecting to create employment for around 350 people having different skills, this includes automobile engineers and technicians.

-Rangs Motors Limited, Ifad Autos Limited and Nitol-Niloy Group are assembling commercial vehicles of Indian Mahindra and Mahindra, Ashok Leyland, and Tata respectively.

Path to Recover and Future Prospects

Duty free spare parts import facility:

If the government allows duty free import of automobile components and spares, it would be possible to run the existing buses, trucks and three-wheelers for one year with the help of low-cost repairs which would reduce the import cost of vehicles during the pandemic.On the other hand, as our export earnings got hit hard during the pandemic, it will be difficult for us to spend dollars to import vehicles at this moment and only the duty-free import of spares can be the appropriate alternative for the sector to save foreign currency. Eventually, the duty free import facilities will empower this sector to produce automobile components in the country within a year.

Registration of three-wheelers:

A policy regarding the registration of three-wheelers and allowing them to ply on the roads may have instrumental contribution in the economy, especially in post lockdown era as huge number of people are now living in the countryside. The livelihoods of at least 20 lakh people depend on three-wheelers. Before implementing this type of policy, Bangladesh Road Transport Authority must implement a standard fitness checking procedure for public transport to reduce the accidents.

Along with several other countries, vaccination against Covid-19 has been successfully rolled out in Bangladesh. Notable megaprojects including the Padma Multipurpose Bridge, the Payra Deep Sea Port, and the Karnaphuli River Tunnel are going to be successfully completed. This will increase demand for local road transport as regional trade will increase; the cargo will also need to be brought to Dhaka and other cities throughout the country. The Karnaphuli River Tunnel will connect southeastern Bangladesh to the Asian Highway Network. These will mainly impact the demand for heavy vehicles, such as trucks.

The most crucial demand driver for the commercial vehicle market is the economic growth of businesses. Especially the manufacturing sector, which directly impacts business confidence and thus the usage of transport by businesses. In Bangladesh, cargo commercial vehicles are mainly used for the transportation of RMG products, construction materials and commodities.

The demand for steel, cement and other construction material in Bangladesh is mainly driven by infrastructure projects in commercial, housing and public sector. The public sector can be further broken down to implementation of the government’s annual development plans and infrastructure projects. After the effect of COVID-19 pandemic, future of this sector looks bright for the large manufacturers mainly due to higher demand from several ongoing government development projects such as construction of Padma Bridge, implementation of metro rail, nuclear power plant construction in Rupnagar etc. However, the growth potential for small and medium size enterprises got delayed as the private construction projects slowed down after pandemic.

There are around 400 steel mills in Bangladesh with a total production capacity of around 8 million MT. Currently major steel producers are AKS, BSRM, KSRM, GPH, Anwar, Rani, SSRM etc. However, comparatively smaller re-rolling mills are located in Narayanganj. There are 37 active cement factories in Bangladesh and more than BDT 30,000 crore has been invested in the industry. Major players are Crown Cement, Shah Cement, Premier Cement, Confidence Cement, Bashundhara Group etc. In Bangladesh, the annual consumption of paint currently stands at about 180,000 tonnes with the presence of over 45 operational entities: Berger Paint and Asian Paint among the key players. Large players of these construction materials mainly fulfill the demand of private development projects by providing exclusive dealership to the traders nationwide. Trader of steel, cement, paint and other construction materials are available in all the districts and unions of Bangladesh. However, there presence is higher in the large cities due to greater demand.

Impact of COVID-19

During the pandemic lockdown, public transport, markets and almost all other economic activities were completely shut down in an effort to curb the spread of Covid-19. As a result, the entire supply chain was disrupted as shipments were delayed, raw material imports were halted and all logistics were frozen. Consequently, the construction projects of private sector were completely stopped. Traders of construction materials could not operate their business for two months during the core lockdown period. As a result, prices of the construction materials went down significantly and the traders faced tremendous loss.

Path to Recover and Future Prospects

Due to pandemic, industry insiders had a fear that they will face 30% lower profits from the JulyDecember period of 2020. However, the reality is different as profits camemainly due to higher demand from government development projects. Meanwhile, all listed steel mills booked higher profits while multinational Berger Paints also witnessed higher profits in the period. Large corporations minimized their loss mainly by lowering their operational cost. Consequently, traders of construction materials are projected to recover from the loss as they cater the demand 55% of individuals, real estate companies and developers. Sales volume significantly increased during the last quarter as the demand for construction material increased as all development activities resumed. Rural demand is also bouncing back as all rural economic activities are going on in full swing. The government’s incentive package of stimulus loans and single digit interest rate also had a positive impact on the sector.

Immediately after pandemic, price of the key component of construction materials such as steel and cement went down. However, price of steel has already increased and price of cement is projected to rise shortly as construction works are back to normal. Despite Covid-19, prospects for overall growth in the trading sector is bright for the country in terms of increasing demand due to urbanization and real estate development especially in Purbachal, Bashundhara and Uttara. However, uncertainty in price fluctuations due to imports of raw materials, fuel, logistics, and foreign exchange rate fluctuations are definitive challenges forthe industry.

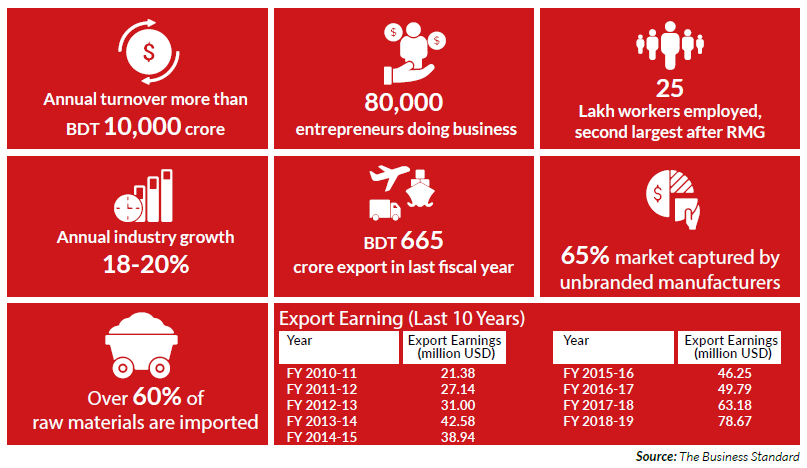

The furniture sector is one of most promising sector in Bangladesh which deploys second largest workers after the RMG sector. It has been experiencing around 20% growth per year and its contribution in GDP is around 0.40%. The growth of this sector is being stimulated by the local and international demand for furniture. Local growth of furniture is being influenced by the overall economic prospect and increasing per capita income of people of this country while international growth derived from cost advantage.

Furniture industry has employed over 25 lakh workers and more than 80 thousand entrepreneurs are involved with this business. Though 93% percent of the goods are consumed locally, the export value of this sector was BDT 665 crore in last fiscal year.

The sector has experienced around 18-20% annual growth over the past decade. The annual turnover size of the market is BDT 10,000 crore. Even though the industry has over 80000 entrepreneurs, the market is still dominated by unbranded furniture that account for 65% of total market share.

As perthe study of Palli Karma-Sahayak Foundation (PKSF 2013) around 99.88% of firms involved in the furniture business are micro and small. These enterprises are scattered all over Bangladesh while big players are mostly located in major cities like Dhaka, Chittagong, Sylhet, Narayanganj, Manikganj, Bogra, Barishal which are densely populated and the demand for furniture is high. There are some areas in Dhaka where furniture factory cluster can be identified such as Mirpur, Sutrapur, Badda, Shajahanpur, Panthapath, Shyampur, Chankharpul, Gandaria, Madanpur. There are few big companies located at Savar and Gazipur.

Impact of COVID-19

COVID-19 has hit hard the furniture makers of our country, specially the unbranded ones which comprise 65% of the total firms involved in this sector. Overall sales of furniture and home decorative sector has declined by 70% which ultimately resulted in job cuts. Since furniture items are not basic needs, people tend to save money for theirlives and livelihood during this difficulttime and are reluctant to buy lavish items.

As per the recent research titled “Post- Covid-19 Jobs and Skills in Bangladesh” performed by a2i, around 0.60 million workers have been laid off in this sector and it predicts this number will be 1.0 million if this situation prolongs.

Mr. Selim H Rahman, chairman of Bangladesh Furniture Industries Owners Association (BFIOA) articulated that there are two types of firms in the sector, organized and unorganized. As majority of them are unorganized, small and scattered across the country, they are the ones who borne the most loss and many employed in this sector lost their jobs.Big players of this sectors are suffocating too. One out of three to four companies are unable to export goods due to travel restrictions imposed to impede the spread of virus.

Path to Recover and Future Prospects

-Imposing limitation on furniture import during post pandemic period to project the interest of local manufacturer.

-Government should encourage automation of production for local manufacturer by reducing VAT on modern equipment or solution like CAM (Computer-Aided Manufacturing) and CNC (Computer Numerical Control).

-All kind of artificial wood and wood alternative are procured from abroad. Government should provide incentives or subsidy to local manufacturers so they can produce wood alternatives locally.

-Since design plays an important role in furniture industry,training on specific items like polishing, engraving and wood carving should be arranged.

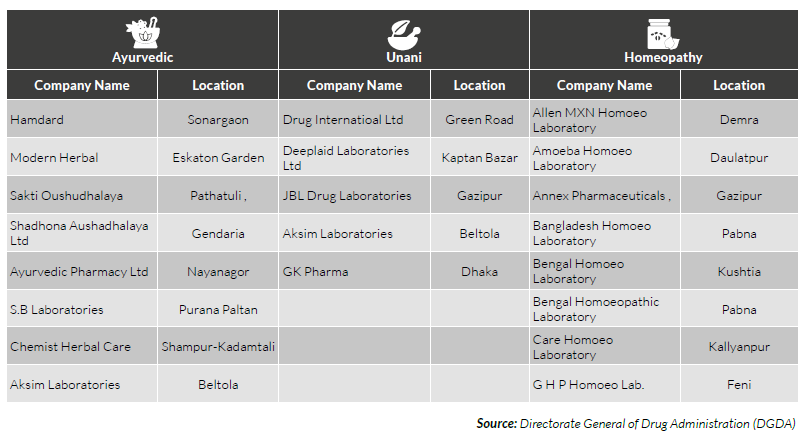

Non-allopathic or alternative medicine is commonly practiced and appreciated for a variety of purposes across the globe. For millions around the world, herbal remedies, traditional treatments and traditional practitioners are the primary source of healthcare as they tend to be more affordable than allopathic health services and are also known to deal with the relentless growth in chronic noncommunicable diseases. In Bangladesh, a flourishing market exists for alternative medical health care. Numerous medical systems are commonly used to fulfill healthcare needs. These include Ayurvedic, Yoga, Unani, Homoeopathy, Naturopathy, Acupuncture, Kabiraji, Hakimi and other folk practices.

As a nation with many rural societies, a significant portion of the population still seeks primary healthcare from traditional practitioners and native medicinal plants. In certain cases, influences such as the economy, society, faith, schooling and environment influence people’s attitudes toward various diseases. According to study, some people do use traditional medicine for particular illnesses, whether they are educated or not, wealthy or poor. Folk curing practices such as attending shrines or traveling to ‘shamans’ (persons who serve as an intermediary between the real and spiritual realms, using spells to treat illness) can still be identified. Location of some of the more famous alternative medical product producers are as follows:

Impact of COVID-19

As panic of the pandemic rose among the general mass, people were not sure what to make of the unprecedented situation. Given the relatively, new traits of the virus and the varying symptoms of the infected individual, medical personalities all over the world were not sure on how to treat the virus. As such it was claimed that prevention was the best way to protect oneself from the virus. Boosting ones’ immunity was seen as one of the major ways to prevent oneself from getting infected. As a result, the demand for non-allopathic remedies expected to boost ones’ immunity went up. These included mainly ayurvedic herbs such as Ashwagandha, Tulsi, Amla, Neem, Turmeric, and Ginger. At the same time, as individuals decided to undertake a healthier lifestyle demand for Naturopathy and Yoga also saw a sharp rise.

Path to Recover and Future Prospects

During the initial outbreak, as most infected were not sure how to treat themselves, a majority of the infected individuals decided to try homeopathy as a path for a cure. Homeopathy is based on the idea that substances that produce symptoms of sickness in healthy people will have a curative effect when given in dilute quantities. The homeopathic practitioners, however, had to warn the patients about the fact that homeopathy would have been effective in treating the symptoms during the early stages and that the patients had to be hospitalized if the symptoms got more serious. To summarize, the demand for alternative medical care saw an overall rise during the covid-19 pandemic.

According to some reports, Bangladesh’s regulatory frameworks for regulating the sales and practice of non-allopathic suppliers have been unsuccessful. Despite the strong demand for their services, they have no interaction with the government in order to obtain the funding they need or to be kept accountable. In Bangladesh, a significant majority of the population depends on the nonallopathic providers. Recognizing their function and incorporating them into the system would be more practical. Involving these informal providers could help the government meet its goal of universal health care by the year 2030.

The food grains and food processing industry is the central part of the agro-processing industry in Bangladesh which accounts for almost 1.7% of the country’s GDP. Albeit this sector has failed to achieve a higher growth rate compared to other industries, this sector still constitutes 8% of the country’s total manufacturing output as per The Financial Express.

Food grains are grains which are grown for human consumption such as rice, wheat, rye etc. Food processing is the manufacturing of food products and beverages. According to the International Food Information Council Foundation, food processing is the transformation of raw ingredients, by physical or chemical means into food or transforming food into other forms. Food processing produces marketable food products, by combining raw ingredients, which the consumers can easily prepare and serve. The food grains and food processing sector includes all naturally produced food grains and all types of

processed food.

Impact of COVID-19

The COVID-19 has had its implications on the food grains and food processing sector as well. The countrywide lockdown has disrupted the supply of food to both markets and consumers, both within and across borders. During the initial weeks of the lockdown, persistent transportation interruptions were negatively impacting the normal market operations. Customers could not get to the markets or feared entering. As a result, vendor businesses in public markets and super shop businesses in Bangladesh went down by almost 80-90% while online shopping experienced a huge surge in sales. The average price of important staples saw an increase of around 15-20% during the lockdown compared to the pre-lockdown prices. The price of rice alone saw a rise of more than 22% amidst the lockdown according to Food and Agriculture Organization. On the other hand, dairy products had to be sold by the farmers at prices lower than their production costs. The instability of the prices, along with lots of people losing their jobs, severely impacted the sustainability of SMEs in this sector during the pandemic.

Path to Recover and Future Prospects

Ensuring food security has been of utmost importance and priority for the government and relevant organizations. At the beginning of the COVID-19 pandemic, the government announced a stimulus package which included BDT 5,000 crore worth of soft loans at 4% interest with a 6-month grace period to multiple agricultural sectors. However, the crops and grains sectors were out of jurisdiction of this stimulus package. The government also eased Letter of Credit (LC) margins for raw materials, food grains and other essential products. Directives have been issued at different ports of entry so that food and allied products are given customs clearance on a priority basis. On top of that, no official restrictions were put in place for transportation of food products even during the lockdown phase.

In the coming days, food grains and food processing sector in Bangladesh is expected to rise because of population and income growth. However, Bangladesh needs to focus on food safety laws and standards to increase the value of food grains and food processing products.

(i) Rice Industry

Rice is the main crop and staple food in Bangladesh. Almost 70-80% of our cultivable land is used for rice production. Study shows that daily per capita rice consumption of our country was 367 grams in 2016 (The International Food Policy Research Institute).

Bangladesh is divided into eight divisions, among them the northwest part of our country: Rajshahi and Rangpur division contribute almost 35% of our total rice production. Due to less industrialization, the abundance of cultivable land, favorable weather etc. result in better rice production in these areas.

Rice mills play a vital role in the rice industry. There are two types of rice mills available in our country: modern or automated rice mill and traditional or husking rice mills. Automated rice mills operate all activities through a mechanical process whereas husking or traditional mills operate all activities manually. As consumption and production of rice increased significantly during the last two decades. At the same time, the commercial rice mills also increased. Now, many husking mill owners have replaced their mills with automated mills to increase their productivity. Automated rice mill’s output is much higher than the husking mills. Automated mills can produce 4 to 12 tons of rice per hour whereas husking mills can produce only 1 to 2 tons per hour.

Impact of COVID-19

Impact of COVID19 on this industry is very minimum as the Government has no restrictions to shut down. Moreover, during lock down period, rice mills encountered an excess demand of rice. Most of the people during that time, piled up the grocery including rice due to the uncertainty of future availability of daily food. The impact was positive as the sales revenue became around double during that period. Big millers took that as an opportunity. Though higher price of paddy made it difficult to maintain inventory management and cash flow but efficient millers managed it very well. As per the insiders, around 7% to 10% rice production was damaged due to flood amounted around 1.10 MMT to 1.60 MMT last year. Lower production tends to

higher price of paddy and rice as seen after flood in 2017. In 2017, to stabilize the market, Government of Bangladesh reduced the import duty of rice but import was 4 times higher than the actual damage. Authority has done the same to control the price of rice with better management. The major challenge for the millers/traders was to recover the receivable as the banking channel was also limited during that period. Furthermore, most of the retailers in Dhaka took this opportunity not to pay the dues on time.

The main challenge of import is to manage the import management properly. Excess import would adversely affect the farmers, small and medium sized millers though very few big millers (large access to finance) would be benefited. It’s been observed that the authority was very vigilant this time and they issue particular certificate with specific amount to import rice.

Path to Recover and Future Prospects

This industry has a good prospect in Bangladesh. If we look into the status of our neighboring country, India is exporting around 10% of its total production and earns a good export earnings. Whereas, our export earnings significantly depend on RMG which should be diversified by focusing on agro based industries and rice industry would be one of the best options.

(ii) Flour Industry

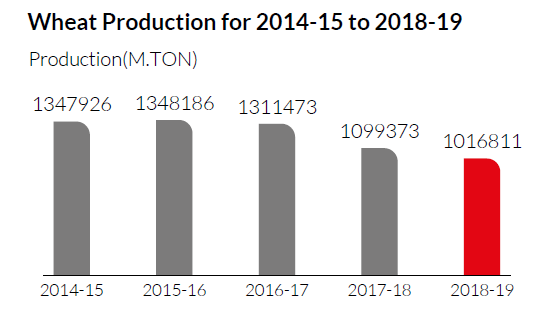

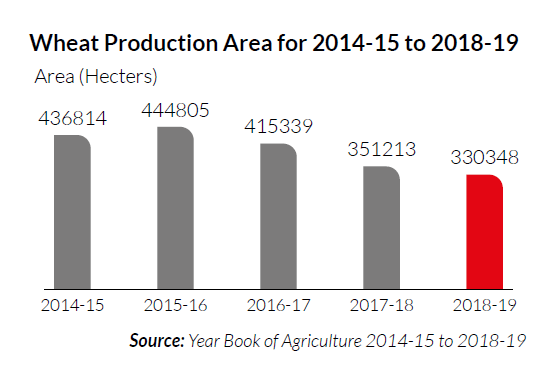

Wheat is the prominent food grain in Bangladesh after rice. The demand for wheat increases at a rate of 15% per annum in our country due to rapid urbanization, changing food habits and rising income. Currently, the country is producing only 1.1 million tons against the demand of 7 million tons of wheat. In this situation, there is no alternative to increase wheat production in our country. However, due to climate change, scarcity of land, and the onslaught of various diseases; wheat production in our country is declining at a significant rate every year. So, we have to depend on imports to meet the demand for wheat. Bangladesh is currently the fifth largest importer of wheat globally, and the import cost of this sector is USD 1.5 billion.

Wheat is mainly a winter crop planted from November to December and harvested from March to April. It has a good yield at relatively low temperatures. However, as a result of climate change, our country’s temperature is continuously rising, which is having a negative impact on wheat production. In 2016, some districts in the southern part of the country were affected by the fungal blast disease of wheat, which resulted in severe damage to wheat production.

Among the eight divisions of our country, the northeastern part of our country (Rajshahi and Rangpur Division) contributes almost 65-70% of our total wheat production. Lack of industrialization, the abundance of cultivable land, favorable weather result in better wheat production in these areas.

Impact of COVID-19

Impact of COVID19 in this industry was significant during the lock down as the supply chain was hugely affected by COVID19. More than 85% of domestic demand is met by importing wheat from abroad. Due to the lock down, import was halted and the price of wheat was higher compared to the industry average. Moreover, demand side was also affected by pandemic as we know; all restaurant, hotels, bakeries and other relevant parties were forced to shut down their business operation which made

the situation more difficult to sustain. Furthermore, higher price of raw material & susceptible demand made the industry participants vulnerable.

Path to Recover and Future Prospects

The Government’s decision of deferring loan payment and stimulus packages helps to stand in the ground. Presently, there is no problem in supply chain and demand side and participants of the industry are doing well though profitability shrunk due to higher competition and increasing price of wheat.

Textiles referto materials that are made from yarns, such as-fibers, thin threads or filaments which are natural or manufactured or a combination. Textiles are created by interlocking these yarns in specific patterns resulting in a length of cloth. Textile can be made through six processes which are Knitting, Felting, Weaving, Non-woven methods, Braiding, Knotting and interlacing. In Narsingdi and Narayanganj district, majority of local textile factories are producing weaving fabrics. The sector which produces grey fabrics is known as weaving sector. This sector mostly produces grey fabrics for wear like three piece fabrics, saree, shawl and some bedding items like bed sheet, curtain, cover etc. Weavers here mostly use Chinese and “Bangla” Power Looms to produce saree and three piece fabrics. For designing on these fabrics, they have to install another special type of machine which is called Dhobi or Jacquard-both are different depending on their usability. Also, to produce bed sheet, curtain and twill, fabrics- millers use different rapier machine.

Babur Haat of Narsingdi district is the major and oldest wholesale market of woven textiles in the country which has been running for around hundreds of years. There are about 3,500 different traders in the market. The market mainly trades for three days from Thursday to Saturday of each week. Woven clothing made in Narsingdi, Narayanganj districts and adjacent areas are sold from here. The products include one colored fabrics, printed fabrics, orna, saree, three piece, lungi, bed sheet, curtain, cover, etc.According to the Financial Express,thismarketis catering to around 70% of the country’s requirement for necessary cloth items and trades over BDT 10 billion weekly. Baburhat market is mainly famous for local cloth items. On the other hand, Madhabdi of Narsingdi district is the wholesale market of yarn and grey fabrics. Yarn traders collect yarn from different spinning mills of Narayanganj and Gazipur which are then sold to different textile millers. Grey fabrics traders collect grey fabrics from different millers of Chowala, Shalidha, Hasnabad, Golpaldi, Araihazar etc. which are then sold to different traders of Baburhat market. At first, the traders collect grey fabrics. Then, they outsource dyeing facility from nearby third party dyeing factories. After that they modify the items based on market demands. Other final products are also trade from Madhabdi, Narsingdi market.

Impact of COVID-19

During the lockdown period, almost all the textile mills and related trading concern discontinued their regular business activities. On the other hand, during that time, fabric traders who had products in their stock netted a good profit. Once the mills were reopened, the mill owners earned higher profit from their productions than the regular times. Import of yarn was slowed down due to COVID-19. Thus, yarn price jumped up to BDT 10 to BDT 25 per pound which resulted in BDT 3 to BDT 4 increase in grey fabrics price per yard. Price of different power loom machines also increased by 15-25% comparing to before pandemic price. As a result the price of final product also went up.

Path to Recover and Future Prospects

Millers and related business traders are expecting a good season in the upcoming Eid, as they could not collect most of their receivables on last Eid due to pandemic. After coming the vaccination, the situation has normalized a bit. People are now going out more and business traders are expecting more trades of local textiles which will hopefully bring a good profit this year.

Light Engineering (LE) is a very important sector for the development of a country. This sector provides the substitute of imported items. It supports various industries including agro based industries, construction and other manufacturing industries.

Recently the Government has decided to establish 10 dedicated light engineering industrial parks in the country (Dhaka, Narayanganj, Jashore, Bogra, Narsingdi, Munshiganj, Mymensingh and Madaripur), which also tells us that how important this sector is and its prospect.

LE basically deals with manufacturing a wide range of spare parts, castings, moulds and dices, oil and gas pipeline fittings and light machinery, as well as repairing those. Around 600,000 workers are earning their living by this industry. About 60,000 MSMEs operate in this sector are still many things that need to be developed in this sector which can help us move towards becoming a developed nation.

Impact of COVID-19

COVID-19 had a severe impact on this sector as around 90% of the workshops were forced to shut down due to lock down, as well as due to shortage of labor. Most of the LE are micro enterprises with very little capital as it was very difficult for them to sustain that time. Though some enterprises which are involved in manufacturing agricultural spares and machineries remained open though they also faced shortage of labor due to limited transportation.

Path to Recover and Future Prospects

After withdrawal of lock down, this sector has revised very soon mainly in North Bengal as most of the industries are agro-based with constant demand side.

RESILIENT TURN AROUND OF SMES FROM THE ADVERSE IMPACT OF COVID-19

Recovery of the SME Sector: An Essential for Ensuring Economy’s Overall Survival

Like in most other nations, the outbreak of the COVID-19 pandemic was unprecedented and shook the Bangladeshi economy. One of Bangladesh’s most prominent industries, the fisheries and livestock industry, employing about 70% of the individuals in the rural areas was struck hard. The dairy farmers also lost around BDT 189 million daily during the lockdown. The disruption of activities in the transportation industry, broke down the supply chain of the construction industry as shipments were delayed. Traders could not operate for two months, causing the price of construction materials fell significantly. Similarly, the fixtures and furniture industry, which employs the second highest number of workers in the country after the RMG industry, lost 70% of its business due to the pandemic, causing 0.60 million worker to be laid off. The non-allopathic or alternative medicine industry on the other hand is one of the few industries to make profit from the pandemic as people turned to Ayurvedic products, Naturopathy and Yoga to boost their immunity. At the same time the demand for Homeopathy medicine saw a sharp rise as people visited Homeopathic practitioners to treat any symptom related to COVID-19.

On the other hand, disruption of activities in the food and food processing industry, resulted in decreased sales for super shops and local vendors, while online sales saw a huge surge. At the same time the price of important staples rose by 15-20%. The local textiles industry faced losses due to an increase in price of raw materials. The light engineering sector, like most other sector also suffered a huge loss as 90% of the workshops were forced to shut down. The situation improved for most business once the lockdown was lifted, with many business recording higher profits than the previous years. The government’s stimulus package worth BDT 5000 crore also fastened the recovery process.

Sushmita Saha

Assistant Manager

IDLC Finance Limited