GLOBAL BANKING ANNUAL REVIEW 2020: A TEST OF RESILIENCE

BANKING INDUSTRY ON THE EDGE

It has been almost a year since the novel coronavirus has deeply shaken economies all over the globe. Industries of all types have been widely affected. The banking industry being one of them has had to endure through challenging times as well. Banks are expected to have severe credit losses, likely through late 2021, almost all banks and banking systems are expected to survive. Then, amid a muted global recovery, banks are likely to face profound challenges regarding ongoing operations. These challenges

are expected to persist beyond 2024. According to McKinsey Global banking annual review, global banking seems to be more in a stable situation than it had been during the recession 12 years ago. If the institutions are efficient enough in terms of capital management, then return on equity can be gained back within five years.

DEALING WITH THE VIRUS

Initially when the crisis began, banks took protective measures for both employees and their customers while their financial system kept operating smoothly. Moving on to few months later, with the number of cases as well as deaths rising, productivity of the banks had eventually declined. Even before the crisis, leading banks in developed markets had achieved 25 percent less branch use per customer than their peers by migrating payments, transfers, and cash transactions to self-service and digital channels. In addition to those who were already digital-only customers previously, another 10 to 15 percent of customers will be unlikely to use a branch after the crisis, further increasing the need to act.

MCKINSEY CATEGORIZED THE PANDEMIC INTO TWO PHASES

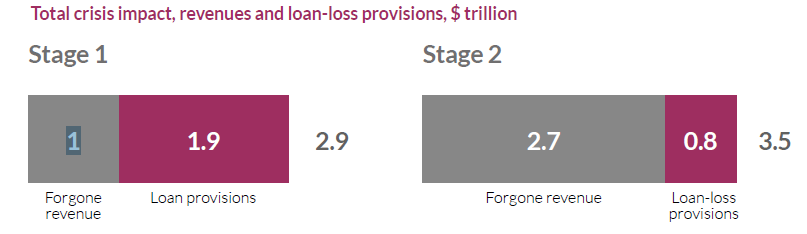

Phase one: The very first one being the increase in loan loss provisions. As soon as the third quarter of 2020 was reached, provision of loan losses went up to $1.15 trillion. With the economy crashing down at a steady rate, millions have lost their job,

shelter and subsequently shutting down their businesses. This ultimately drove most banks to a very high liquidity level which disrupted their initial goal- securing liquidity and funding according to McKinsey. Businesses play the most important role as a customer to the banks. The pandemic declined their sales which eventually increased their obligation towards their banks. Banks were seen to have dramatic drop in provision due to the support provided by the government. A new standard referred to as International Financial Reporting Standard 9 (IFRS 9), which calls for banks to take provisions sooner than previously. This new implementation can give a rise in loan amounts which is enough problematic already.

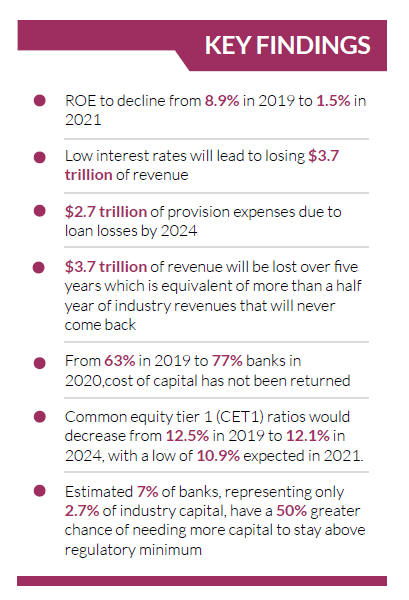

Phase two: The coming years, from provision of loan losses, the spotlight will be shifted on revenues- entering phase two of the pandemic. According to McKinsey, revenues may be recover for two to four years. Revenues are most likely to drop by 14% considering their precrisis situation by the end of 2024. Sparking globally, from 2020- 2024 the industry could encounter losing $1.5 trillion to $4.7 trillion revenue. As many name it, the revenues generated by shadow banking grew twice as fast as the balancesheet companies of banks between 2017 and 2019. Observing revenues from business lines, we see that retail and corporate banking were by far the main contributors to the top line in 2019, which are both vulnerable to a zero-rate setting and elevated risk. Feebased companies are a smaller component of wealth and asset management, market infrastructure, investment banking, and payments.

INVESTMENTS GREW IN DIGITAL CHANNELS

Even during a global pandemic, banks have continued investing in different platforms. The McKinsey Global banking annual review explained two prospects of investments during this crisis.

Wealth Management: It plays a crucial role in times of crisis. Looking into the next four years, market performance will be leading the revenue growth globally. Business owners will try to capitalize their business through lowest interest rates possible. While the pandemic has had an adverse effect but an increase in digitalization has led services to be more accessible for clients locally and internationally as well. Nonetheless, wealth management will continue to be an attractive business due to its capital efficiency and growth profile relative to other opportunities, and its increasingly central role in financial advisory as other advisory services such as insurance consolidate.

Capital markets, investment banking, and market infrastructure: During the early stages of the pandemic, market based businesses at some banks were running at the same pace as they had previously, but with time their progress and productivity declined. Since the growth of the businesses have slowed down their sales and services will eventually adjust at a lower level. The crisis will motivate businesses to engage into M&A activities but buyers and sellers are likely to be less enthusiastic compared to how they used to be.

As per the report issued by McKinsey, the above points do not represent the full impact the crisis has on revenues and balance sheet of the business. Businesses are most likely to fall behind in terms of their profitability. The bank’s management has to make intricate moves to make way through the difficult path that lies ahead them.

Impact of Covid-19 Pandemic on the Coastal Shipping Industry of Bangladesh

The Costal Shipping and Cement Industry of Bangladesh: Recovering from the Pandemic Wave

The cement industry of Bangladesh has beenrecognized as one of the fastest growing cement markets worldwide, with a double digit growth rate over the last decade, and an annual demand of around 33 million tonnes. This is owing to the construction of mega projects undertaken, and the constant infrastructural development on way to further develop the nation. Yet Bangladesh remains as one of the least cement consuming nations in the world

topped by China, India, Myanmar etc. The deadly wave of the Coronavirus, followed by lockdowns has had an adverse impact on an industry that employs over 10,60,000 people directly and indirectly. Disrupted supply chains, halted projects, and fluctuating exchange rates have made it challenging for cement manufacturers and exporters to maintain a smooth business flow as companies incurred losses and capacity remained underutilized. However, investors remain hopeful of the future as they approve fund to enhance the cement production capacity of Bangladesh.

As we speak of exports and imports, a crucial industry comes into focus – the Coastal Shipping industry of Bangladesh, which not only assists trade but plays a vital role in the inland waterway transport system. Lightering vessels,in particular, have played an important role in assuring safe offloading process from Mother Ships as ports in Bangladesh are not deep enough for many international ships to navigate through. Necessary lockdowns, to contain the virus, have forced trade levels down, allowing only drugs and other essential commodities to be traded. This put lightering vessel companies in a state of despair as they struggled to cover their overheads with minimal business activity. However, as lockdowns slowly recede and several mega projects start construction,the industry is showing promising growth prospects.

Sushmita Saha

Assistant Manager

IDLC Finance Limited