CEMENT INDUSTRY: CURRENT MARKET UPDATE

Bonnishikha Chowdhury , Saraf Rahman Khan

Demand and Supply Scenario

Currently, the annual demand for cement is 33 million tonnes, while the industry’s installed capacity is 78 million tonnes with another 11 million tonnes to be added in the next three years, according to Bangladesh Cement Manufacturers Association (BCMA). Over the last seven years, the CAGR of the cement industry had been approximately 11.5%.

Per Capita Consumption

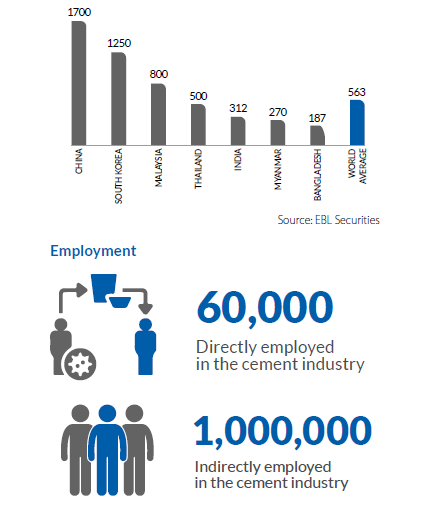

The annual per capita cement consumption has grown from 45kg to 200kg in the last two decades in line with the economic development of Bangladesh. However, Bangladesh is still one of the lowest consuming countries of cement products in the world.

Export

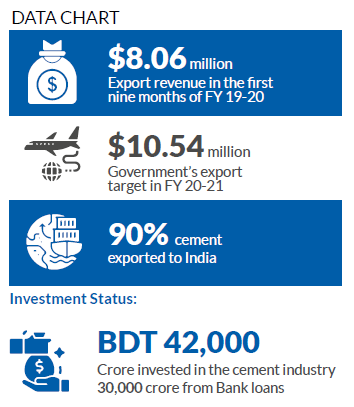

The cement industry earned export revenue of $8.06 million in the first nine months of FY 19-20. However, there were no export earnings from this sector in April due to the nationwide general holidays. At the end of ten months of the fiscal year, cement exports remained stuck in the place where it had been a month earlier. However, the government’s export target for the sector, in the current fiscal year, is $10.54 million.

Bangladesh exports 90% of its cement to India. As the rupee depreciated against the dollar, cement exports to India fell by 20% year-on-year.Some BDT 42, 000 crore has been invested in this sector. Of that, around BDT 30,000 crore is from

bank loans. Companies are pouring heavy investment into the sector to increase capacity. Bashundhara Group is investing BDT 1,000 crore for the installation of a third cement production unit. Moreover, back in July, Bangladesh Chemical Industries Corp (BCIC) and Saudi-Arabia based Engineering Dimension International Investment (EDII) agreed to build a cement plant under the name of Saudi Bangla Integrated Cement Co Ltd. These investments and the swift recovery – all point to the fact that cement manufacturers have faith in continued growth in the construction and infrastructure development of the country in the coming days.

Key market players

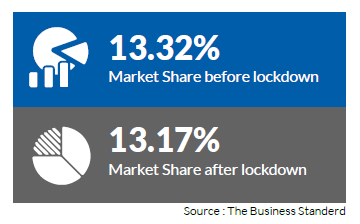

Around 81% of the cement market is controlled by 10 leading companies. However, in this ongoing pandemic situation smaller companies did better than the larger ones owing to the activity of the rural economy. From June, the sales of the big companies started to increase again.

Impact of pandemic

-Manufacturers could utilize only 10% of their capacity during lock down which caused them a loss of BDT 3,000 crore.

-Government projects were halted during the Covid-19 shutdown. As a result, sales of big companies declined up to 90%.

-Loss of income due to business shutdown meant many urban dwellers were unable to pay rent or forfeited flat purchases – the source of income for real estate developers. Moreover, ongoing projects were forced to a halt for two months. The real estate downturn translated to less demand for associated sectors including the cement industry.

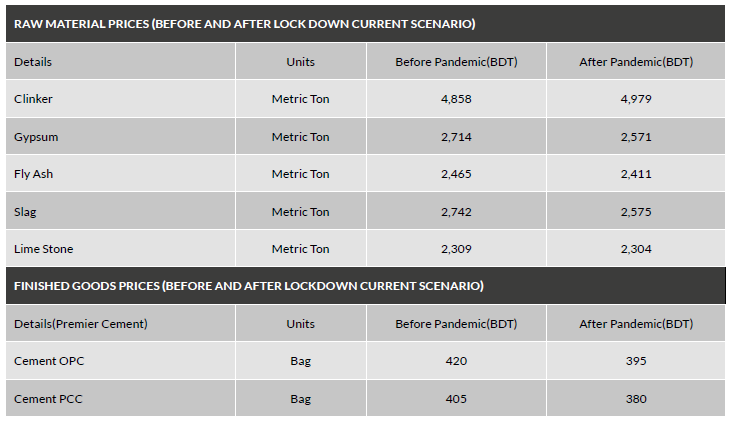

-Raw material price in the international market is already 10-15% down after the novel coronavirus outbreak.

-Exports have seen a fall in FY 2019-20 as ports were closed down during the general holidays, barring trade. Although this decline may be seen as a one-time event, there are other reasons to believe that exports will fall in the long run. Competition from Indian companies due to the granting of transit facilities will threaten the future potential of cement exports to the northeastern states of India. Moreover, Bangladeshi cement exporters also incur high transportation costs which disincentivize exports.

Before and after lockdown Financial Implications and growth status

Before the shutdown, the industry’s daily revenue was over BDT 100 crore whereas now, the daily revenue has fallen below BDT 25 crore. The industry’s biggest concern now is receivables of about BDT 10,000 - 12,000 crore because of dependence on credit sales.

Tax Burden

Almost 100% raw materials for cement factories are imported and the main item clinker is subject to BDT 500 import duty against the import of per tonne. Based on the import price of $42 for a tonne of clinker, effective import duty goes as high as 14%, which is highest among cement manufacturing countries which depend on imported raw materials.

A nearly 45% overcapacity, coupled with a rapid increase in utility bills and of course volatility in prices of imported raw materials prevent cement manufacturers from increasing prices regardless of the cost scenario. Thus, The BCMA demands the import duty at 5% or BDT 300 per tonne. They also requested that the government withdraw 3% AIT on cement supply from the factories.

Amirul Haque, managing director of Premier Cement, said, “No sector has more than five percent duty on intermediate raw materials. But in the cement sector, it is more than 15%. A huge amount of money from businesses get stuck because of the 3% advance tax.”

Industry Plea

The industry needs sufficient working capital in thecoming days so that it can withstand the reduced cash flows – both because of low revenue and slow collection of receivables. BCMA sought incentives from the government to weather the Covid-19 storm. It also sought a six month’s relief from paying utility bills and taxes. Challenges and Way Forward Currently, there are 35 cement factories in the country with a production capacity of eight crore tonnes of cement. The country has a demand for 3.5 crore tonnes which would add 1.1 crore tonnes more in the next three years. Around 81% of the cement market is controlled by 10 leading companies.

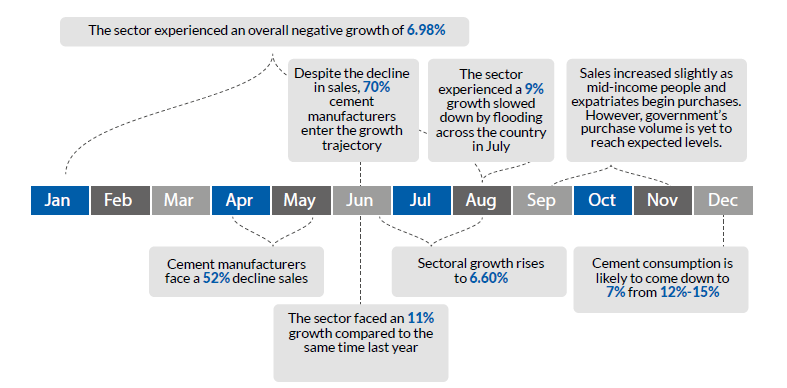

Hope still remains that the government will accelerate its infrastructure spending to offset the impact of a potential slack in private sector activities. There will also remain challenges as the government is likely to be overburdened through providing fiscal incentives to prop up the economy According to the Bangladesh Cement Manufacturers Association among 36 companies operational right now, only seven were in negative growth in August. The overall growth in the cement sector this month was more than 9%.

Impact of COVID-19 on a few prominent companies in the industry

Shah Cement

Shah Cement – a prominent name in the cement industry of Bangladesh – has faced adversities no less than others. During the second quarter of 2020, the company recorded drastic declines in sales volume. In April and May, the sales of Shah Cement dropped by 37% and 27% compared to the same months of the earlier year. In June too they recorded negative growth. However, in August, the company achieved 14.30% growth compared with the same period last year. Overall, Shah Cement recorded negative growth of 8.07% in the first three quarters of the year.

On condition of anonymity, an official of Abul Khair Group, the mother company of Shah Cement, said that their sales decreased in January as the construction of the Padma Bridge project had been halted as Chinese engineers were stuck in their country. However, supply has increased since July and it is expected that there wouldn’t be negative growth next year – according to the same official.

Bashundhara Cement

Bashundhara Cement, a supplier of the Padma bridge project, faced sales decline from 45% to 40% during the first 2 months of shutdown. The company returned to growth in June-August period.

Unique Cement

Unique cement is known to be the second leading company of the market and they have recorded a 46% negative growth from April through to May. In June-August, the company got, on average, more than 30% growth, and their market share increased to 8.39% in 2020.

Impact of Covid-19 Pandemic on the Coastal Shipping Industry of Bangladesh

The Costal Shipping and Cement Industry of Bangladesh: Recovering from the Pandemic Wave

The cement industry of Bangladesh has beenrecognized as one of the fastest growing cement markets worldwide, with a double digit growth rate over the last decade, and an annual demand of around 33 million tonnes. This is owing to the construction of mega projects undertaken, and the constant infrastructural development on way to further develop the nation. Yet Bangladesh remains as one of the least cement consuming nations in the world

topped by China, India, Myanmar etc. The deadly wave of the Coronavirus, followed by lockdowns has had an adverse impact on an industry that employs over 10,60,000 people directly and indirectly. Disrupted supply chains, halted projects, and fluctuating exchange rates have made it challenging for cement manufacturers and exporters to maintain a smooth business flow as companies incurred losses and capacity remained underutilized. However, investors remain hopeful of the future as they approve fund to enhance the cement production capacity of Bangladesh.

As we speak of exports and imports, a crucial industry comes into focus – the Coastal Shipping industry of Bangladesh, which not only assists trade but plays a vital role in the inland waterway transport system. Lightering vessels,in particular, have played an important role in assuring safe offloading process from Mother Ships as ports in Bangladesh are not deep enough for many international ships to navigate through. Necessary lockdowns, to contain the virus, have forced trade levels down, allowing only drugs and other essential commodities to be traded. This put lightering vessel companies in a state of despair as they struggled to cover their overheads with minimal business activity. However, as lockdowns slowly recede and several mega projects start construction,the industry is showing promising growth prospects.

Sushmita Saha

Assistant Manager

IDLC Finance Limited