MFS SECTOR OF BANGLADESH SAFEGUARDING CURRENCY MOBILITY DURING PANDEMIC

Sushmita Saha, Assistant Manager, Credit-SME and Bonnishikha Chowdhury, Executive Officer, Credit-SME

In every payment eco system, a new service can only be successful if it has significant demand. On the other hand, necessity is the mother of invention.

It all started when researchers funded by the UK’s Department for International Development (DFID), the foreign aid arm of the British government, observed that Kenyans were transferring mobile airtime as a proxy for money. On the other hand, Vodafone was looking for ways to support microfinance through its mobile platform, as access to banking and credit was limited in Kenya and transporting cash was both risky and slow. Such demand of easily accessible method of payment system paved the way of developing M-Pesa. Since its launch in 2007, M-pesa is still going strong by reshaping Kenya’s banking and telecom sector and extending financial inclusion. M-pesa has been especially successful in creating small businesses by reaching low-income Kenyans. Its impact in Kenya put mobile money services on the map, and the subsequent proliferation of similar services can be credited to this success.

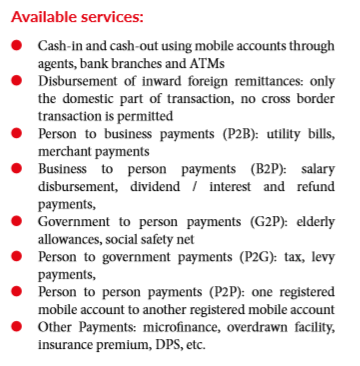

In a country like Bangladesh where the financial literacy rate is really low and a great part of the population is not under formal banking system, Mobile Financial Services is a must in order to ensure currency mobility. Thus, as a part of Bangladesh Bank’s Financial Inclusion Program, MFS was introduced. According to ‘The Global Findex Database 2017, in Bangladesh the percentage of 15-plus people having an account is 50% and only 35% of them are woman. However, as per The Financial Express January 2020 data, MFS is certainly proved successful by playing a big role in adding 48% of adult population under formal financial services umbrella which was only 20% in 2013. Moreover, about BDT 10 billion is transacted daily through this platform on an average.

Models of MFS in Bangladesh

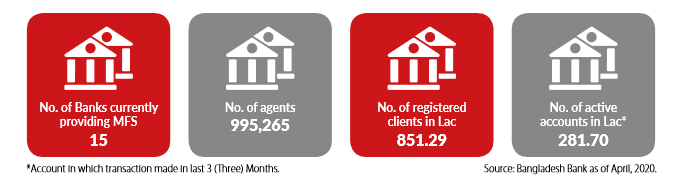

As of June 2018, eighteen banks and one subsidiary have been permitted to provide MFS, whereas fifteen are in operation. Bangladesh Bank permits only bankled MFS providers to operate in the country. Bankled MFS is a model where a bank may run the MFS as a product of the bank or a bank may form an MFS providing subsidiary with at least 51% of the share held by the bank with control of the board. There can also be Non-Bank/Telco-led MFS Model which is not available in Bangladesh. Even though there are some advantages in non-bank / Telco led model but for regulatory purpose most of the countries prefer bank lead model over non-bank/Telco led. However, around the globe telco led models are more successful as telecom industries has access to more information and an already built infrastructure.

Key market leaders

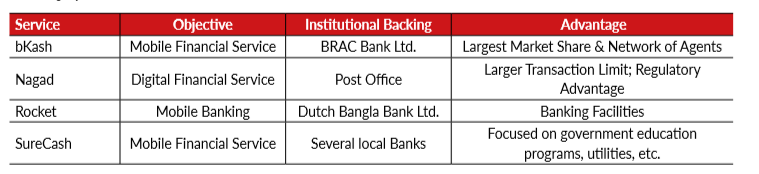

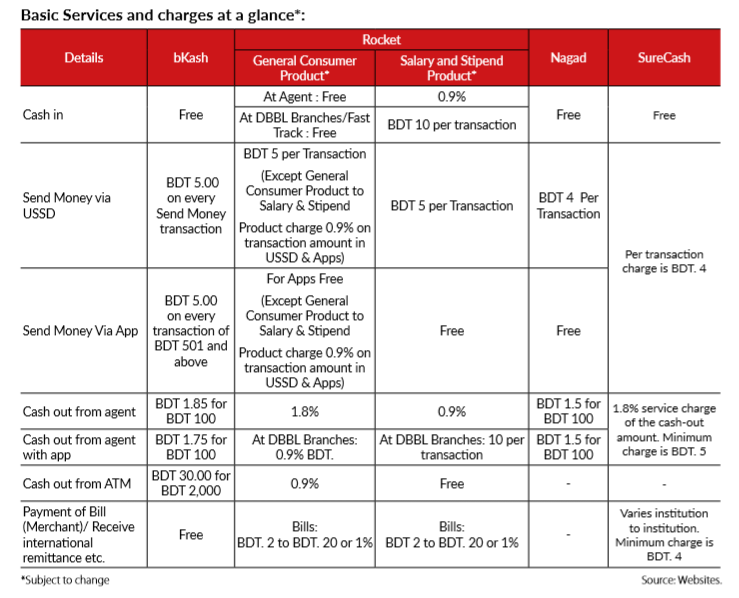

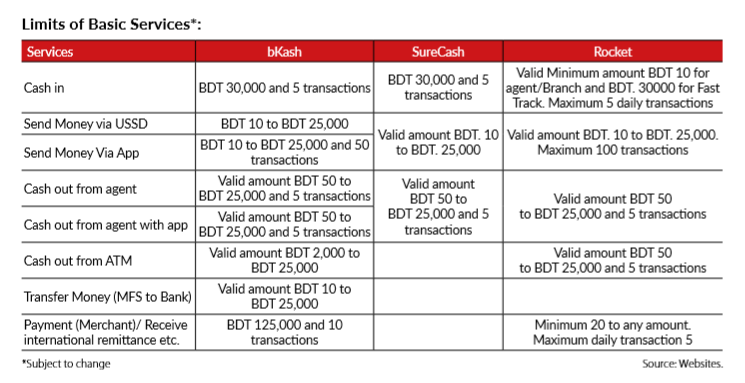

Even though Bangladesh Bank has permitted 18 banks to provide MFS but currently 15 banks are providing MFS. In this sector, both pioneer and market leader is bKash Ltd. However, Rocket, SureCash, Nagad are also considered as key market players.

bKash

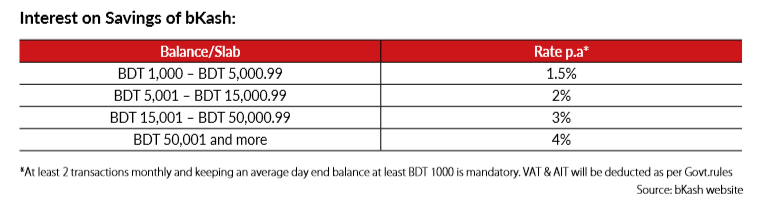

bKash started their MFS program in 2011. At that point it was only a USSD application. It is considered to be the market leader of Bangladesh in this sector. Backed by BRAC Bank, currently, bKash is running a network of more than 180,000 agents throughout urban and rural areas of Bangladesh with over 30 million registered accounts and holding 80% of the market share. They offer cash-in, cash out, ATM money withdrawal, bill payments, mobile recharge, remittance, donation, purchasing movie ticket etc. These can be availed through the prominent telecommunication networks in Bangladesh. In addition, bKash offers up to 4% Interest (annual rate) on the savings of bKash mobile account.

Rocket

After bKash, Rocket has second largest market share in this sector. Dutch Bangla Bank Limited (DBBL) launched banking services and financial facilities using the mobile communication network in 2012. DBBL provided bank-led mobile banking services were re-branded as ‘Rocket’. Customers can easily avail the DBBL provided mobile banking services via ‘Rocket’ app. As of April 2018, has 218,818 agents. Moreover, Nexus Pay is also an app provided to DBBL account holders with the goal of providing advanced banking services and integrating cards of customers. Unlike other vendors, all services through Nexus Pay are completely free and does not require any additional commissions.

Nagad

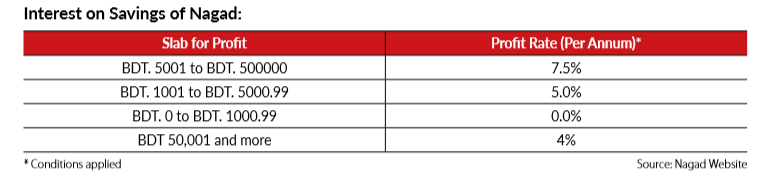

Nagad is a Bangladesh Post Office (BPO) initiative and it is not under Bangladesh Bank’s jurisdiction. It was launched in November 2018. This MFS platform covers money transactions via Cash-In, Cash-Out, and Send Money. These MFS also include popular services like, mobile recharge. The upcoming services include utility bills payment, and e-commerce payment gateway.

SureCash

SureCash is another potential MFS platform launched by Progoti Systems Ltd in 2015. SureCash represents an open network of payment in corporation with several local banks, with above 1,000 payment partners. SureCash developed their exclusive mechanism focusing on government education programs, schools, colleges, utilities, etc.

The role of mobile financing sector in this ongoing pandemic

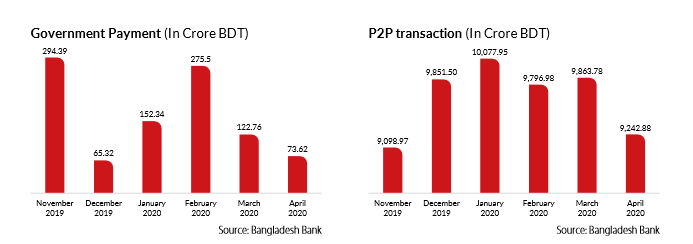

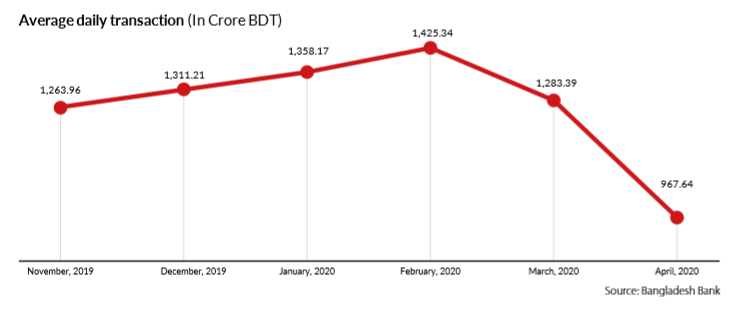

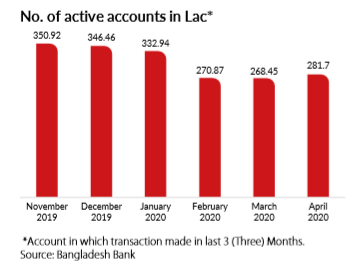

The year 2020 has been all about the global coronavirus pandemic, which catapulted MFS to an essential service for ensuring the regular money flow between urban and rural economies during the countrywide shutdown. It was assumed that considering the need for social distancing and the push towards digital transactions to prevent the spread of the highly contagious coronavirus this sector might flourish well. However, as per the April, 2020 data there was a negative growth in both average daily transaction and number of daily average transactions compared to March, 2020. It caused due to countrywide shut down declared for covid situation which lead to closure of economic activities from March 26,2020. Thus, the average daily transaction stood -24.6% and number of daily average transaction was -4.7% in April, 2020 compared to March, 2020.On the other hand, in April 2020, number of agents, number of registered clients and number of active accounts showed a positive growth of 0.3%, 3.1% and 4.9% respectively compared to March 2020 as per BB data. During the lock down period even though the use of mobile money has increased among the middle-class or the upper-middle-class but the lower income class did not transact money regularly. The outbreak impacted the overall economy and the MFS industry as well. However, considering Eid the situation got slightly better in May. As per the Daily Star data, average daily transaction of bKash in March was BDT 985 crore and it came down to BDT 800 crore in April and then again the daily average transaction volume rose to BDT 1,200 crore in May.

However, the role of MFS sector was praiseworthy in pandemic.

In April, 2020 Bangladesh Bank instructed the factories to open free of cost MFS accounts for the workers in order to disburse their March salary from the BDT. 5,000 crore stimulus package. More than half of the 4.1 million workers in the garment sector, which accounts for about 84 per cent of the country’s total exports, did not have MFS or bank accounts till then. As per BGMEA report some 970,000 new MFS accounts were opened with bKash, 550,000 with Rocket and 400,000 with Nagad till April 18, 2020. Such decision was very praiseworthy as most of the workers left for their villages after lock down declaration and it would have made the covid situation worse if they had to travel back to their work stations in order to collect salary.

14 lac families received PM’s BDT 2,500 cash aid each via MFS in May, 2020. Out of those 50 lac families, Nagad was entitled to disburse the highest amount of BDT 425 crore to 17 lac families, bKash BDT 375 crore to 15 lac families, Rocket BDT 250 crore to 10 lac families, Surecash BDT 200 crore to 8 lac families. To be added, the government was only charged BDT 15 for each disbursement even though the cash out charges are higher, all the operators sent full cash out value to the beneficiary family.

The Prisoner’s Cash fund, which receives money in cash, has historically been used by detainees to pay for various services while imprisoned. In order to curb the spread of the novel coronavirus receiving the fund through Nagad and bkash is also introduced. Inmates will not be permitted to receive more than BDT 2,000 per month and the money even can’t be sent in one go. This means friends or family members can only transfer a maximum BDT 1,000 at any given time within a month.

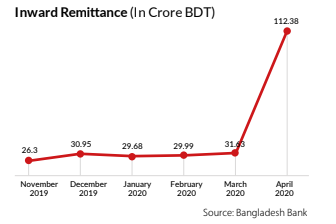

Bangladeshi expatriates are now sending more money to home using MFS compared to pre covid days. Compared to March 2020, in April,2020 inward remittance through MFS observed a growth of 255.3%.

Considering the covid situation, bKash has rolled out a new facility that allows people to transfer funds to non-account holders, in a move that may cut reliance on cash and increase the mobile financial services accessibility. On the other hand, credit card bills can also be paid via MFS now.

Limitations to be recovered for better service and way outs

There is no doubt that the number of mobile phone users are increasing rapidly in Bangladesh. However, still the biggest difficulty towards flourishing MFS sector is low penetration rate of cell phones. The reason behind this is cell phone penetration is higher in urban areas but not in rural areas. Moreover, in urban areas even in slums a wide number of MFS agents are visible which is not the same in rural areas. Thus, if the first barrier can be resolved more currency mobilization will be assured.

The development sector has more access in the financial activities of the rural area inhabitants which banks do not have. Thus, the development organizations can play and have been playing in financial inclusion by disbursing micro finance credits through MFS.

In order to broaden the horizon of MFS, it has to be included more and more aspects of banking activities. For example, till now direct transaction between bank and MFS is very limited. As a matter of fact, not all the banks of the country are even included. Such transactions have to be taken in to consideration.

However, in order to access both cell phone subscription and MFS account some regulatory documents are required for example NID Card. Thus, the availability of such documents should also be considered.

MFS sector of Bangladesh safeguarding currency mobility during pandemic

The flying MFS Sector of Bangladesh

Growth can only be sustainable when the whole population is benefitted from that.

The value addition of Mobile Financial Services (MFS) in a pandemic-hit vibrant economy like Bangladesh has been remarkable. Till March 2020, the scope of MFS was only confined in cash-in, cash-out, bill and other payments, remittance and some other ancillary services. However, the great pandemic broadened the horizon of MFS service, starting from disbursing wage to 4,000 RMG workers to disbursing government cash support to 50 Lac families. MFS is discerned to be the game-changer in payment landscape, with players like Nagad, bKash, Rocket and Surecash.

Banks are seeing immense possibilities of mobile money for financial inclusion. In a time when cash transactions pose near life-threatening risk due to containment of deadly virus, mobile money is acting like a life-savior. Not all banks have a strong infrastructure to facilitate MFS. Aside from balance transfer, banks now must work on managing payment mechanism on mass scale, for loan or deposit products. It is high time, banks should collaborate with MFS providers and reap the most benefit out of their payment infrastructure. Rocket by Dutch Bangla Bank Limited, uCash by United Commercial Bank Limited and many more have jumped on the MFS bandwagon sensing the breakneck growth opportunity. In the “new-normal” era, digital payments will take the lead and reaching mass population is only possible with the help of MFS.

Sushmita Saha

Assistant Manager

IDLC Finance Limited