NON PERFORMING LOANS BANKING SECTOR: COMBATING AMIDST MACRO CHALLENGES

Adnan Rashid & Monthly Business Review Team

Financial industry is the driving force of any country by being the intermediary between deficit units and surplus units of funds. A stronger and dynamic banking sector is the key for any economy to function properly. The same applies to Bangladesh as well. With an above 6% GDP growth rate over the last decade, Bangladesh is recognized as one of the highest growth potential economies of the world. However, high Non-Performing Loans (NPLs) has

been a growing concern for the local banking sector and the economy as a whole for quite some time now.

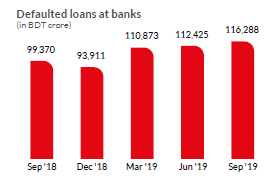

And the ever more worrying fact is that the situation is yet to show any sign of improvement. NPL has direct impact on a bank’s profitability. Due to provisioning requirement against NPL, banks are required to keep provision of fund against the diligent accounts and cannot book profit on them. Continuous rise in NPL pushes the banks into red and eventually requires banks to raise equity to cover for the provision requirement. If the provisioning shortfall continues for long and the NPL scenario of the bank does not improve, the bank may struggle to repay depositors money and eventually the question of solvency of the financial institution may arise. If such instances happen to majority of banks and for longer period of time, the economy may face liquidity shortage and acute dearth of public confidence, hence, eroding country’s growth potential and economic development.

Definition of Non-Performing Loans

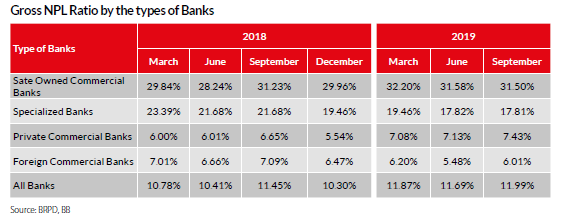

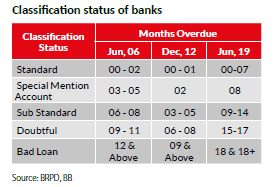

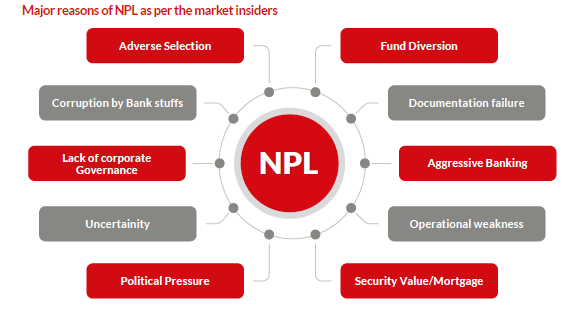

Let’s first look at what state defines an account to become non-performing loan. The definition of NPL was changed twice in last 10 years. Initially, the general definition of NPL was that when an account becomes 6 months past due, it becomes a diligent loan. In 2012, Bangladesh Bank changed this definition in line with BASEL II and defined a loan to be default when it becomes 3 months past due. Obviously, this tightening of policy in line of international standard gave rise to the NPL state of the local banking sector. It multiplied by a series of scams and irregularities that unearthed one after another, which hit the overall health of the sector hard.

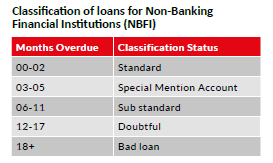

Again, in the middle of 2019, Bangladesh Bank relaxed the classification policy and regulated that a 9 month past due will be termed as a default loan. However, the policy remained same for Non-Banking Financial Institutions (NBFI) as post-2012.

Now, the policy relaxation may ease up the NPL ratio of the banking sector, but the underlying vulnerability of bad loans to the banking system will remain the same as before, as per market experts. To some extent it may encourage the defaulters rather than bringing qualitative change to loan origination or recovery processes as in retrospect, this actually benefits the defaulters as they get longer time period to pay off loans than the good borrowers and even with lower cost. Moreover, it does not ramp up the confidence of depositors as banks can actually defer the provisioning requirement which is essential to safeguard small depositors’ money.

Restructure, reschedule and written off rules and their negative impact on default culture

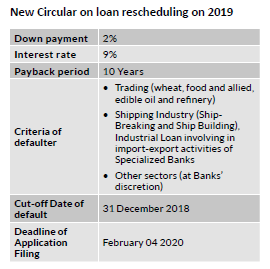

The policy of restructuring loans was initially introduced in order to facilitate the borrowers with good payment behaviour. Such benefits were supposed to be a one-time offer on the condition that if the firms fail, the banks will take legal action. However, today as it stands, all the business groups which restructured their default loan under this large loan restructuring package have defaulted on their loan repayments. Banks recovered only 25% of total restricted loans in last four years. The usual policy for rescheduling was, a borrower must pay at least 15% of the outstanding balance to avail a fresh loan from the rescheduling bank. However, The Central Bank issued special policies on May, 2019 on loan rescheduling and one time exit.

This, on the paper, seems like a really lucrative opportunity for the defaulters to start with a clean slate. But such opportunities were extended to the large loan defaulters of the country before, and most of them took the opportunity and reverted back to the bad loan zone. Also, this somewhat look like a reward for bad borrowers and punishment for good borrowers. At present, the normal lending rate of almost all types of loans are in the double digit, while a delinquent customer is getting this record clean at 9% for 10 years, which is even lower than what some banks offer against deposit due to liquidity crunch. Earlier in 2015, the Central Bank extended such facilities. At that time, 11 large business groups got their loans of nearly BDT 15,000 crore restructured on relaxed terms. However, the amount swelled to BDT 17,103 crore as repayments were not made, according to Bangladesh Bank.

A rundown on the ARA and NI act for possible repercussions of defaulting in loans and current state of cases in queue in courts:

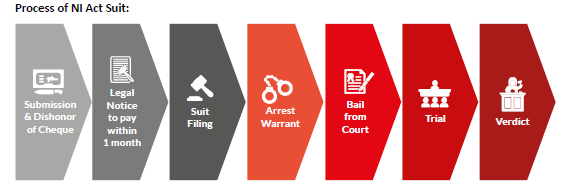

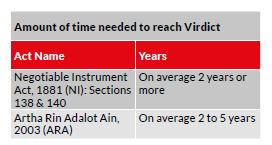

Negotiable Instrument Act, 1881 (NI): Sections 138 & 140

Financial institutions can file criminal suit against dishonoured cheques after legal notice and the suit can be filed without termination of the agreement. After paper submission of the suit, the court will issue a summon notice. If the notice is not honoured the court will issue an arrest warrant. Arrest warrant is the most powerful tool of NI act as it puts the defaulter under pressure of going to the jail. The defaulter can take bail from the court later after getting arrested. However, if the summons notice does not work, there will be trial followed by verdict. On average it takes 2 years or more to reach the verdict depending on the lawyer and court pressure.

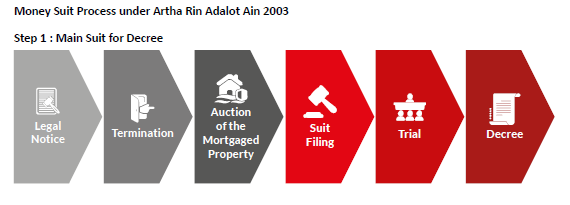

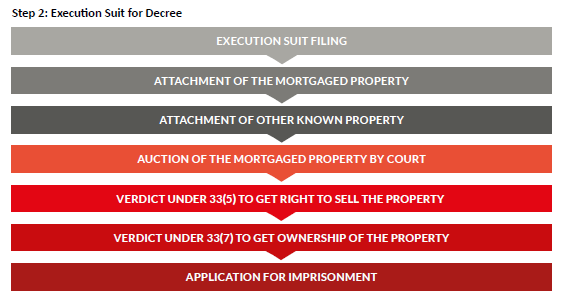

Artha Rin Adalot Ain, 2003 (ARA)

It is filed to recover entire receivables from bad clients. Loan call up is the prerequisite for the act. Directors and their personal properties can be attached. Normally it takes on average 3 to 5 years to reach verdict.

The number of cases piling up in the court is very high. On average a bank or financial intuition has around 4000 to 4500 cases piled up in the court.

Provisioning Shortfall due to high NPL As per central bank regulations, banks have to keep 0.50% to 5% provision with Bangladesh Bank against defaulted loans for general category, 20% against classified loans of sub-standard category, 50% against classified loans of doubtful category, and 100% against classified loans of bad or loss category. However, 12 banks faced a combined provision shortfall of BDT 12,000 crore in the third quarter of 2019. Rising trend in defaulted loans in the banking sector is largely responsible for the huge provisioning shortfall.

Possible further adverse impact of liquidity crisis

As of November 21, 2019 the Government borrowed BDT 42,607 crore (90% of its annual limit) set in the budget. In contrast, only BDT 26,446 crore was

borrowed from the banking sector in the entire fiscal 2018-19. Soaring government borrowing may lead to a liquidity crisis for Banks/FIs since most of their loanable funds are occupied there. On the other hand, upward pressure on devaluation of USD-BDT exchange rate is prone to have an adverse impact on the import-oriented/trading businesses, which will, in turn, work as an impetus for default culture and hit the banks’ profitability.

IMF and ADB’s assessment of current NPL situation of Bangladesh

A recent report of the International Monetary Fund draws a gloomier picture of the state of non-performing loans of Bangladesh’s banking sector. According to the report, the actual size of bad loan is more than the officially recognized amount as Central Bank’s definition of default loan does not capture all sources of problem assets.

IMF opined that around 675 large borrowers that are previously reported as defaulters have obtained stay order from the high court and no longer appear in the CIB database and banks can report them as nonclassified. There are BDT 79,242 crore such loans as of January 10, 2019, according to Bangladesh Bank. Those loans should be counted as problem assets as well as those in the Special Mention accounts, which is the precursor to classified category. The report also mentioned, large number of the special mention loans are rescheduled or restructured many times and in so doing mask the problem loans. However, as per the report the solution to such problem should be in line with the country’s macroeconomic performance.

According to another report titled “Managing Non Performing loans in Bangladesh” by ADB, any kind of irregularities in the credit management can contribute to the NPL growth in the Banking System. Moreover, it hampers the new lending capacity because of the shortage of fund causing economic slowdown. To improve asset quality, including writing-off loans with the rise of NPL level the banks are required to raise provisions against probable loan losses and carry out internal consolidation which apparently cause decline and return on equity taking place and affecting bank

solvency and liquidity. Thus, the high NPL ratio is weakening the overall credit quality of the banking sector in Bangladesh.

However, as per the report, apart from following the international best practices and the resolution strategies implemented in other countries Bangladesh needs to follow the below mentioned key measures:

- Corporate governance should be strengthened and carefully due diligence should be followed in lending decisions by banks.

- The existing Bankruptcy Act, 1997 should be strengthen or a bankruptcy and insolvency law should be enacted as a one stop solution consolidating all the laws.

- Both the Government and the Central Bank have to ensure rigorous implementation of the present banking rules and regulations.

- Fair pricing of collaterals through competent accounting firms with global best practices should be ensured. A data warehouse for collaterals also needs to be set up in order to ensure that.

- Consolidation, merging, divesting, restructuring or even privatization of State Owned Commercial Banks can be done in order to bring down their number.

- A national AMC like the Republic of Korea’s KAMCO or Malaysia’s Danaharta can be established to take over NPLs from ailing banks

Approaches made by the neighbouring countries in managing ballooning NPL and what we can learn from them:

China

China penalized the defaulted customers by putting restriction on enjoying different social benefits that the regular citizens are entitled to avail. Restrictions are namely not being able to purchase air ticket, purchase tickets of high-speed train, serve as executive or representative of corporate entities, avail further credit requests and getting banned on personal ID that is used to avail the hotel accommodation facilities. This blacklist contains many political bodies, legislative and government staffs of China and there is no exception in punishment. Even, they cannot buy any real estate. In some cases, the defaulters do not get any promotion upon being defaulter. In some of the provinces of China, the defaulters are socially and publicly shamed. For Example, a court in the Southwest Sichuan Province began leaving recorded messages on the phones of 20 debtors. When someone rings a defaulter, the message

plays: “The person you are calling has been put on a blacklist by the courts for failing to repay their debts. Please urge this person to honor their legal obligations.”

Malaysia

Malaysia blacklisted their overdue clients. Defaulters in Malaysia are not allowed to leave the country. Besides penalization, Malaysia went through a major

restructuring of credit disbursement. Malaysian government used a recovery strategy in a non-cash format to settle down the outstanding loans, by converting non-cash recovery asset or collaterals into cash. Malaysia introduced Asset Management Companies (AMC) to extract these loans.

Republic of Korea

To bring a comprehensive financial stability, the Government of the Republic of Korea took steps and succeeded in a very short time. The licenses are cancelled and operations are suspended for those financial institutions which failed to meet the minimum capital adequacy standard, the balance sheets of viable ones are cleaned up to give a boost, mergers are created into large banks and restructured banks are given responsibility of corporate restructuring with allocation of public resources. NPL is a concerning issue but NPL ratio dropped when Korea Asset Management Corporation (KAMCO) purchased NPLs with discount but sold it off with high prices. The healthy banks received capital through public bonds by acquiring insolvent ones by the Korea Deposit Insurance Corporation and guaranteed by the government on interest costs. As a result, commercial banks had become more transparent and healthier than before, and both foreign and local investors ‘confidence has largely been restored. NPL, was fought well to be reduced. This legal framework, securitization and other reforms such as in the bankruptcy law, contributed to KAMCO’s success.

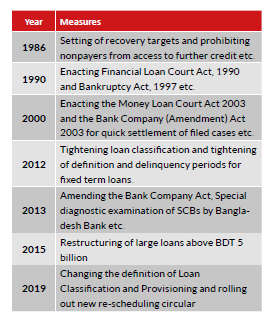

Initiatives by Government and regulators to buckle down the burgeoning NPL and what more should be done

Over the years several measures have been adopted by the regulators in order to address nonperforming Loans in Bangladesh. Some mentionable measures are:

However, there are also some very important ongoing reform measures among which if necessary amendments to the major acts are especially mentionable.

Ongoing and prospective reform measures:

Merger or consolidation between FIs with strong equity base with FIs with relatively small equity base:

Regulations on merger can help decrease the rate of NPL. As the strong and efficient banks with better underwriting capacity merges with weaker and smaller banks, then it becomes easier for them to avoid default payments. Liquidation of a financial institution leaves scars on a country’s economy which takes years to heal. Restructuring is always a better idea than liquidation

for mainly three reasons. First of all, it prevents from system collapse, secondly, liquidation leads to spread widening which restructuring prevents. Thirdly, saves from credit crunch caused by fund crisis. The success of restructuring can be seen widely in our neighbouring countries. In 1985, two

large state-owned banks of Philippines, that together owned 50% of the total banking assets, saw 70% of their assets going bad. These two banks were eventually restructured through a comprehensive rehabilitative process like transferring NPL to a third party trust, heavy cost cutting measures etc. However, through new management, recapitalization, the banks were able to be improve their capital adequacy ratios and return to profitability by 1987. On the other hand, a major step taken by Vietnam in reducing NPLs, was the establishment of the Vietnam Asset Management Company (VAMC) in July 2013, which acquired approximately $13.5 billion in NPLs by the end of 2017, financed by the issuance of VAMC

(special) bonds. This measure played an important role in reducing NPL on the banks’ balance sheets. As a matter of fact, some of our successful institutions of present days are also results of restructuring.

Establishing Asset Management Company (AMC)

Successful AMCs can help banks improve their balance-sheet picture, thereby allowing them to free up capital for lending. The government may decide to set up special bankruptcy courts to attend to AMC transferred assets cases only, along with strict timebound proceedings including the appeal process. These measures will help increase the price offered by AMCs to the banks as the residual value of restructured NPL assets will increase, thereby encouraging banks to release the better-priced bad loans.

Reinforcing Corporate Governance

Moreover, in order to diminish NPL growth good and transparent corporate governance must be ensured in the management and board committee. The governance bodies should be empowered to make objective decisions while issuing loans.

Setting up data-warehouse

Recommendations of creating of secondary market for NPLs, setting up a separate data warehouse for NPLs under the existing facilities of the Credit Information Bureau of the Bangladesh Bank, and tax rebate facility for traders of the default loans should also be considered.

Monthly Business Review - January 2020

Bangladesh, the once “bottomless basket” has grown to be the new “Asian Tiger”, on account of incessant growth in the last decade. International investors are eyeing for Bangladesh as a promising investment destination due to immense growth opportunities. Also, the ongoing mega projects will change the blueprint of the country’s infrastructure, which is considered to be an obstacle in doing business.

However, the ever-piling up non-performing loans in the banking sector can make the situation worse.

Non-performing loans eats up the portion of loanable fund of a Financial Institutions by keeping provision, which was otherwise supposed to be channeled to the deficit sector i.e. the business entities or to productive sectors. As of November 2019, government already borrowed 90% of its annual limit from the banks, which will in turn, reduce banks’ portion of loanable fund. Further NPL pressure may aggravate the situation and lead to a liquidity crisis. Alongside, rising non-performing loans will have a direct hit on banks’ solvency scenario, for which banks may succumb to an unhealthy position in long run.

As NPL is constantly becoming a burning issue for the banking sector as well the economy, NPL management is need of this hour. Reinforcing good corporate governance is a prime activity for the sector. Instances of how companies become bankrupt in absence of good governance are aplenty worldwide. In India, merger between the strong banks and the weak banks (in terms of balance sheets) is evident recently as the problem of non-performing bank loans has emerged over the past few years. Our banking industry can also follow their suit, as combining portfolios can provide additional risk diversification. Lastly, establishing Asset Management Companies (AMC) which will purchase the toxic assets of the banks at a discount, and collect from the non-performing assets via selling securities over the years. Without taking care of ever-stacking NPL, the banking sector cannot contribute to the real economic growth. Hence, it is high time the top management of the FIs should come up with effective solutions.

Download View