WHITE GOODS FINANCING

Prospective Market Segment for Retail Lending

Did you know that consumer electronics and domestic appliances have been categorized on the basis of colour such as brown goods, grey goods and white goods? Consumer electronics (electronic devices bought and made for personal use rather than commercial use), comprise the brown goods class. Grey goods are mostly computers and all devices associated with computers such as printers, scanners, joysticks etc. The gray and brown markets have been known to intersect every now and then, with electronics that fall into both categories. Finally we arrive to the topic of discussion – white goods. White goods are heavy consumer durable goods which usually have a white enamel finish. This category includes air conditioners, refrigerators, dishwashers, microwave ovens, induction cookers and many more. The term ‘home appliances’ is quite self-explanatory as it includes goods or a device or piece of equipment designed to perform a specific task. Thus, entertainment devices such as televisions are not included in the white goods category.

The market for consumer electronics consists of a number of segments, each of which has a significant share in the total market size. In order to get a comprehensive understanding of the market, the consumer durables market has been classified into 3 major categories Refrigerators, Air Conditioner & Home Appliances:

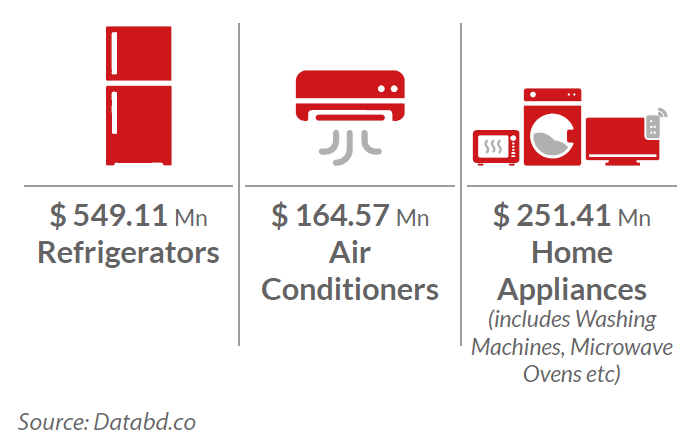

Market Size:

The continually growing market in Bangladesh stands

at USD 965.78 Million as of 2017.

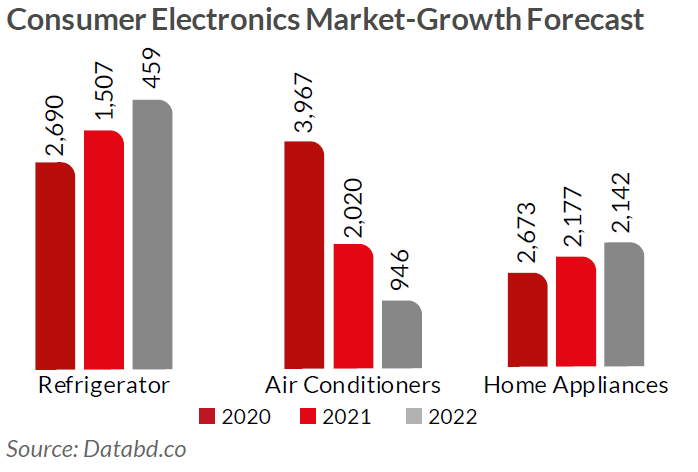

Growth Forecast

All of the product categories are experiencing rapid growth and forecasts indicate a continuous growth in the coming years. The market standing for refrigerators look the most promising in terms of growth.

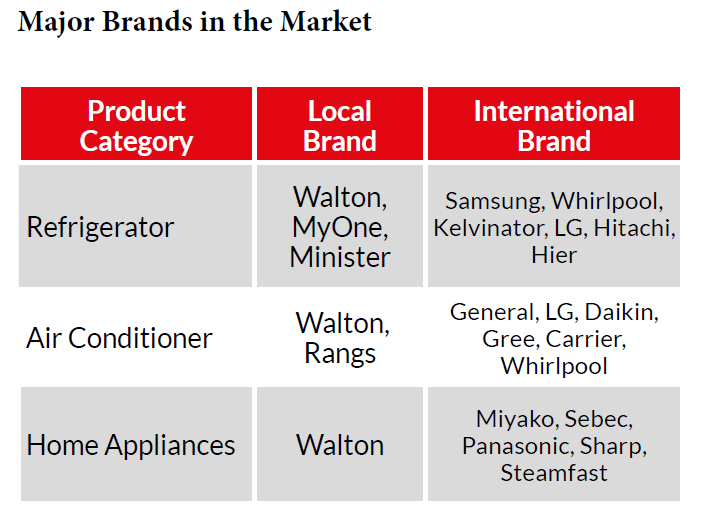

Competitive Landscape

Consumer Electronics is a competitive market with a wide ranging products from both international and local players. Due to the brand image and credibility, the international brands have stronger association with the customers. Local players, however, are dominating the market in terms of sales volume, mainly due to competitive pricing.

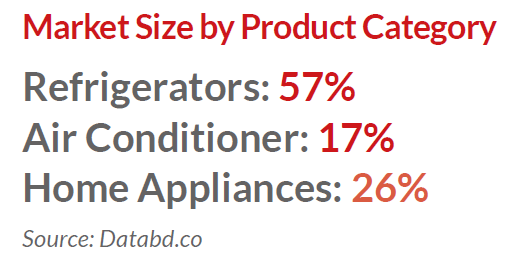

Market Share by Category

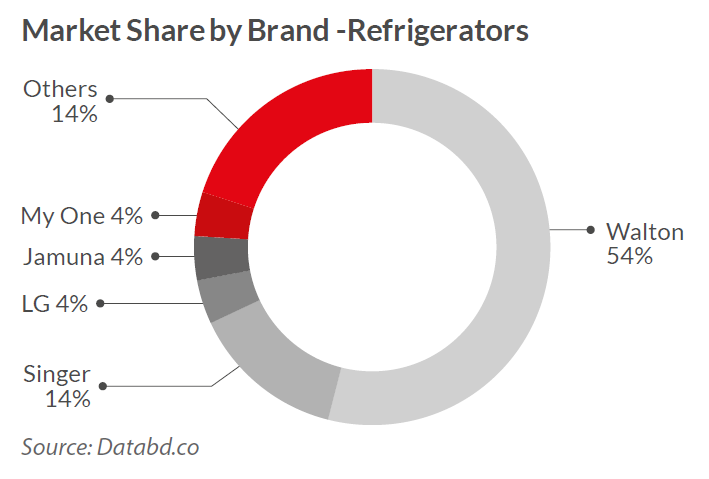

Refrigerators

In the market for Refrigerators, famous local brand Walton is in the leading position with 54% market sharing, taking over more than half of the market share. The second position is held by international brand, Singer.

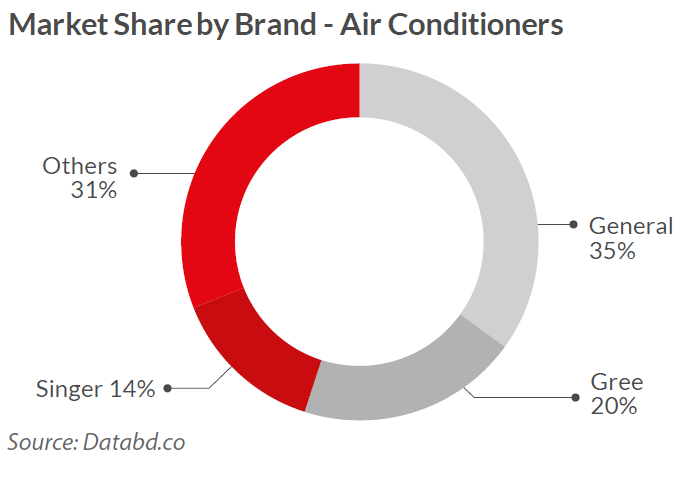

Air Conditioners

The Air Conditioner market used to be dominated by foreign brands like LG, General and Gree. In recent years, local brands such as Walton has started manufacturing/assembling air conditioners at competitive prices.

Reasons behind increase of demand:

Bangladesh consists of the world’s 8th largest population, with consumer spending at around USD 200 billion and a booming economy growing at 7% annually. Bangladesh’s geo-strategic positioning between India and China allows it to be a trading focal point of South Asia, this has allowed expansion opportunities for multiple sectors over the last decade. Now obviously, a booming economy, a huge population (mostly under 35) and an increasing number of business industries means that the Bangladeshi consumer market is growing at an exponential rate. The rising middle and affluent class (income of USD 400 or higher) consumers have been playing a critical role in this extraordinary growth. According to a study in 2015 by the Boston Consulting Group, the middle and affluent class in Bangladesh is expected to grow to 34 million in number by 2025.

Factors that are affecting consumption patterns are demographic dividends – a younger population depicts there is strong demand for goods like fast food, coffee and other beverages and consumer durable items. The increasing urban population and growing number of nuclear families (30% of the total population now lives in urban areas, a large increase from only 19% back in the 1990s). A rising literacy rate, growing middle class and white collar culture and globalization (all thanks to the advent of information technology and social media), has changed the consumer market quite drastically. Due to growing economic prosperity across the board, middle and affluent class population residing in smaller cities increasingly have spare capital to invest in consumer durables.

With rising income, demand for consumer durables will be increasing and the current industry growth of 15% is projected to increase further. Alongside, with ease of making hire purchase and new electricity connections across the country, demand for consumer durables are expected to increase in the near future.

White goods financing in India

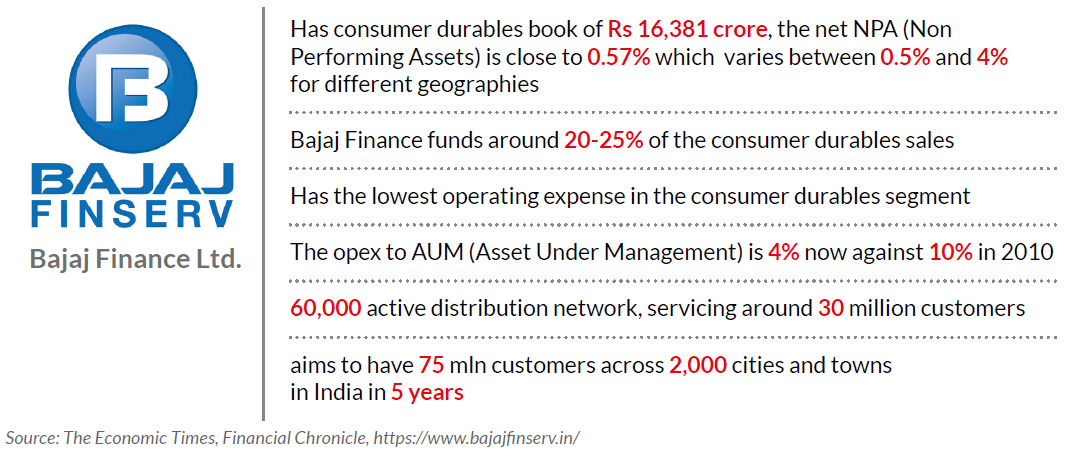

The rapid growth in the economy of India has been mentioned in the past few years. Considering almost same socio-economic condition and other variability, the consumption of white goods in India is also growing significantly. Moreover, because of the recent import duty hike and mirroring the smart phone and television producers, the producers of refrigerators, washing machines and air conditioners have launched a “make in India” thrust. According to the Economic Times, the local manufacturers have already invested in the expansion of the manufacturing plants. However, such initiatives are taken to cater the growing demands of white goods. As the white goods are not considered luxury products anymore to cater the demands of the financial industry of India, it has also achieved a great advancement in case of financing such products. Now the consumers do not have to go through time consuming process of taking personal loans to avail their desired white good products. The clients are able to take on the spot loan or even a loan without credit card to buy the desired product which means that they do not have to undergo lengthy documentation processes in order to take a credit. Such facilities are available not only for white goods but also for brown or grey goods. To reach the mass people, the financing companies are building a robust network with the home appliances supplier outlets. Moreover, the consumers are getting the scope to select a flexible EMI plan which suit their pockets and does not cause any burden on their monthly expenses. Surprisingly, some financial institutions even offer some value added services with such apparently risky financing schemes. The value added services include payment holiday, free early repayment and other fringe benefits. Among the financial institutions, the Non-Banking Financial Companies (NBFC) of India are doing better in case of financing white goods or home appliances. As a matter of fact, NBFCs such as Bajaj Finance are doing better than the banking institutions. According to the Financial Chronicle (a newspaper and global business networking platform of India), 60% of the total sale of consumer appliances are sold through financing (50-55% of which are through NBFCs and 12-15%) through credit card sales. The NBFCs have the early movers advantage here banks still have a long way to go to give a strong fight. Moreover, in India, NBFCs can offer zero interest financing which banks are not allowed to provide as such loans are not transparent enough. However, the interest cost of such zero interest schemes are normally distributed among the manufacturers, dealers and customers as processing fees. The Financial Chronicle also mentioned that Bajaj finance is the market leader, followed by Tata Capital and Capital First which recently merged with IDFC.

Even though consumers can avail credits facility for any home appliances but according to Bajaj Finance Limited; the products which are popular among their appliances credit takers are: refrigerators, washing machines and air conditioners. This means that the consumers take credits to buy white goods more compared to other products. The secret behind the rocket fast credit services of these institutions is the advancement of information technology. With the blessings of IT, the financial institutions of India are now capable of offering spot credit to their clients as the eligibility analysis takes only a few minutes. Moreover, the documentation is also easy. All the client must have a regular income source and mandatory documents are required by the regulatory board. The client does not even need to visit the financial institution to get the credit as all the processing will be done at the retail store of the white goods. Moreover, if the client has taken any other credit previously from that particular institution, he or she will be eligible for some pre-approved credits and there will be no need of documents resubmission. Such loans normally run for 6 to 9 months and the clients have some flexibility to choose EMI size and tenure. However, for the institutions, operational strength is very crucial for such schemes as underwriting and collection strength are absent because of absence of collateral. It can be said that the conventional way of underwritings has been replaced by data analytics tools, credit bureau and social media presence. To be successful in this sector, banks and NBFCs depend largely on data analytics. The only way to manage is to create a homogenous pool and use analytics for disbursement which is possible only with strong analytics team. Thus companies that can manage to keep the credit and operational cost low, will win the game.

White goods financing: Scenario of Bangladesh

Current ways of borrowing money for white goods

“0% Interest-EMI payment” is the most widely used term in the world of consumer appliances financing in Bangladesh. Besides traditional financing through personal loans, now a days buying appliances through credit cards has gained enormous popularity among the consumers. Thus, banks are in a better position than Non-Banking financial institutions (NBFIs) as credit card facility is mostly provided by the banks in Bangladesh. Availing a personal loan is comparatively time consuming and requires a good amount of documentation. On the other hand, using credit cards does not require extra documentation or processing time. White goods are not considered a luxury rather a necessity. Now the consumers of white goods can vary from sub-urban to rural areas. Credit cards can be easily accessible around the urban parts of the country although it’s not quite popular in the sub-urban or rural areas.

However, even though credit card is a very handy way to buy desired goods immediately, it is advised not to charge such big amount with credit card. It is because buying white goods blocks a good part of credit limit which can be needed in case of emergency. Sometimes the manufacturers or distributors arrange a non-financial institution credit service for their clients where the clients are allowed to pay back in installment. In such cases local knowledge is the collection strength.

Question may arise why it is important to have a product dedicated for white goods financing. Considering the usage and demand side availing a personal loan is a quite lengthy process. Moreover, such goods are widely used in day to day life. Thus, every household will be interested in having the product as early as possible. On the other hand, comparing to other major loan facilities like home, car etc. the amount of white goods credit is comparatively small. Thus, having a financing product, which is faster in processing for such products will increase the sale of such products and the growing demand will lead to industrialization. Moreover, the white goods distributors are widely targeting the sub-urban and rural market and lengthy documentation process is not much appreciated in such markets. Thus, a consumer financing product with faster processing can be a blessing for white goods industry.

If Banks and NBFIs are capable to finance such goods through spot financing like India

Such small ticket loans can make a huge asset portfolio if provided in bulk amount. Banks and NBFIs of Bangladesh are definitely capable of providing such spot loan service like India but unfortunately the infrastructure is still not ready. To provide such service it is very important to have a strong data infrastructure and alternative credit scoring model which the biggest strength of India and our weakness. For India the whole process of credit analysis takes only two minutes because with strong data infrastructure the financial institutions are capable of analyzing an individual’s deposits, credit and other transaction related behavior within seconds and provide a score based on which the financial institution reach the conclusion about that individual’s credit worthiness.

Opportunities and threats in such schemes

Such alternative score card system can only be a blessing for any sector if the data is not manipulated. If spot loan service is established it will be a milestone for consumer financing. As it can be seen from home and auto mobile loan, easy financing can boost the industry any consumption. The similar trend can be assumed for white goods. The demand is already there; easy financing will not only boost the consumption but also motivate the local manufacturer to produce more.

However, every credit facility comes with risks. It can be assumed that for such facility the chances of defaulting are very high. Moreover, data manipulation or system failure can also be considered as threats. Considering the instability of the economy before launching such product ensuring strong security and provisions against such loans is important.

Way Forward

There is no doubt that ensuring easy financing will unleash a new era for consumer financing. Even though right now the economy of Bangladesh is concentrating more on industrialization, consumer financing can be a way to achieve desired success in industrialization. Thus, regulatory incentives are compulsory followed by a strong data infrastructure and data analytics expertise. Moreover, a strong collection process is mandatory to avoid the consequences of non-playability. In such case, the manufacturers and dealers can come to an agreement where they can share the burden of payment defaults.

One option for such collaboration can be, forwarding the collection responsibilities in the hands of the dealers or manufacturers as the manufacturer or distributors have the strength of local consumer knowledge. This would require dealers to be sincere in their efforts to collect money from their customers. If the dealers have a large number of customers, then they will have to even open new departments and hire new employees to ensure collection is done efficiently and on time, because accountability of payment now lies with the dealers. First loss credit facility/second loss credit facility can also be an alternative where the financial institution will cover a smaller part of the default amount and the rest will be covered by the manufacturer/distributer or vice versa. This is a fruitful process as the default portion can be covered by the manufacturer or distributor’s profit margin. Another solution can be the overdraft system. This means that the manufacturers will take loans from the financial institutions and then sell using EMI system themselves. This will allow smaller businesses to sell using the EMI method and thus acquire a large customer base. Now if the loans for the manufacturer is at a 5-10% rate, in order to ensure a profit, the manufacturers may charge a significantly higher rate while selling via EMI. They may not also be equipped to handle or ensure collection from a large customer base moreover the manufacturer or distributor can charge higher amount of interest which will not be fair to the clients. Guarantee coverage is also very important when handing out loans in Bangladesh. Because the infrastructure is not very strong, people tend to take advantage of it. Any form of guarantee to ensure payment is important. This can be keeping the landlord as the guarantor for white goods financing, so that he may seize assets when the individual tries to move or elope. A down payment may also be a form of guarantee coverage, so that the minimum losses may be covered in case payments are not paid periodically. However, incentives from regulators is a must for any kind of changes thus nothing can be done without the support the regulatory authority.

In the end, it can be stated that, like other consumer financing products easy processing spot loan for white goods is also possible to establish in Bangladesh even though we are some steps behind. However, in past few years Bangladesh made mentionable advancement in information technology. Thus, with proper planning and regulatory incentives the financial industry of Bangladesh can be able to make the sub urban and rural households of Bangladesh well equipped with white goods.

Monthly Business Review - December 2019

According to a study in 2015 by the Boston Consulting Group, the middle and affluent class (MAC), which includes households that earn at least USD 401 (or BDT 34,000) per month or higher, in Bangladesh is expected to grow to 34 million in number by 2025. Which means, in the coming years the demand of the consumer durables will increase significantly.

Question may arise out of all the consumer electronic durables, why only financing of white goods (large machines with an enamel finish; for example: refrigerators, air conditioners, washing machines, microwave ovens etc.) is more focused here. The answer is simple, it’s growing demand. Even a few years ago air conditioners or microwave ovens used to be a sign of luxury but now a days such products can easily be categorized as necessity. One of the reasons behind such rapid growth in usage can be increased purchasing power but the role of nuclear families or working women cannot be denied. Convenience is the biggest selling trait of any product in the modern world.

Although the middle income class has drastically risen in the last decade, people are not comfortable spending large amounts of money at once. India has achieved a praiseworthy expertise in case of white goods financing. 60% of the total sale are now made through specific financing instruments out of which only 12-15% is via credit card. With the blessings of data analytics and alternative credit scoring, India is now capable of analyzing a client’s credit worthiness within few minutes which helps them to cater the growing need efficiently and this is where we have a great scope for improvement. However, to achieve such expertise, the first and foremost requirement is infrastructural development and expertise on data analytics. Moreover, regulatory incentives are also necessary to reach such accomplishment.

Download View