Disruptive forces of digital transformation reshaping banking experience

The banking industry faced the heat of digital disruption when AntFinancial, Tencent join Hong Kong virtual banking race.

As Bloomberg reported, bringing major players in the virtual banking race shook up the city’s traditional banking sector. Virtual banks are estimated to snare as much as 30% of revenues from Hong Kong’s traditional lenders.

Banking sector is sitting on the cusp of disruption with the largest tech firms being in the best position to impact legacy banks of all sizes. Traditionally, consumers compared their banking providers with other Financial Institutions, but today’s customers want their banking service to be much like deeply personalized, digital experiences as they enjoy from Amazon. Research continues to show that people would switch to Amazon if the ecommerce giant offered banking solutions.

Banking sector is one of the realms fully based on trust. Trust and loyalty in banking represent the foundation of current and future financial relationships. Bain & Company’s November’18 survey of 151,894 consumers in 29 countries reflect that technology firms, such as PayPal and Amazon garner a level of trust with consumers almost as high as banks in general. 29% of respondents trust at least one tech company more than their primary bank. As the number of challenger banks and technology firms grow, traditional banks find their interactions and engagement with customers diminishing.

If the digital giants are going to invade the bank’s turf, banks must start to act more like digital giants

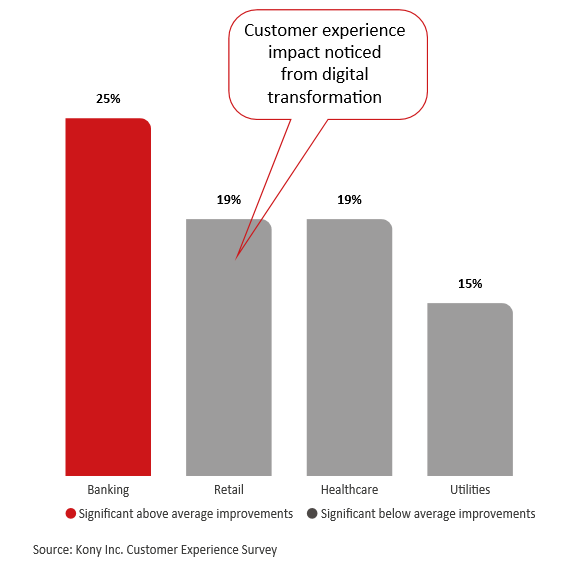

Banks who adopted digital measures to improve their efficiency reflected high satisfaction in customer experience. According to a survey conducted in July 2019, banking industry is found to be the most successful industry vertical, with 25% of banking customers reporting a significant improvement in the level of customer experience. But still, this is not enough. Prior venturing into the digital experience, banks must understand why they should ponder in exploring the digital transformation:

Profitability is strong and relatively consistent over time

Profitability is strong and relatively consistent over time

Offerings are easy to replicate and there is only modest differentiation

Inefficiency can be reduced by digital transformation

Consumers and/or segments are underserved

Innovation has been slow or non-existent

The list not only defines why Amazon or another large tech company may find the banking industry enticing for entry, but why hundreds of fintech firms globally have already entered financial services.

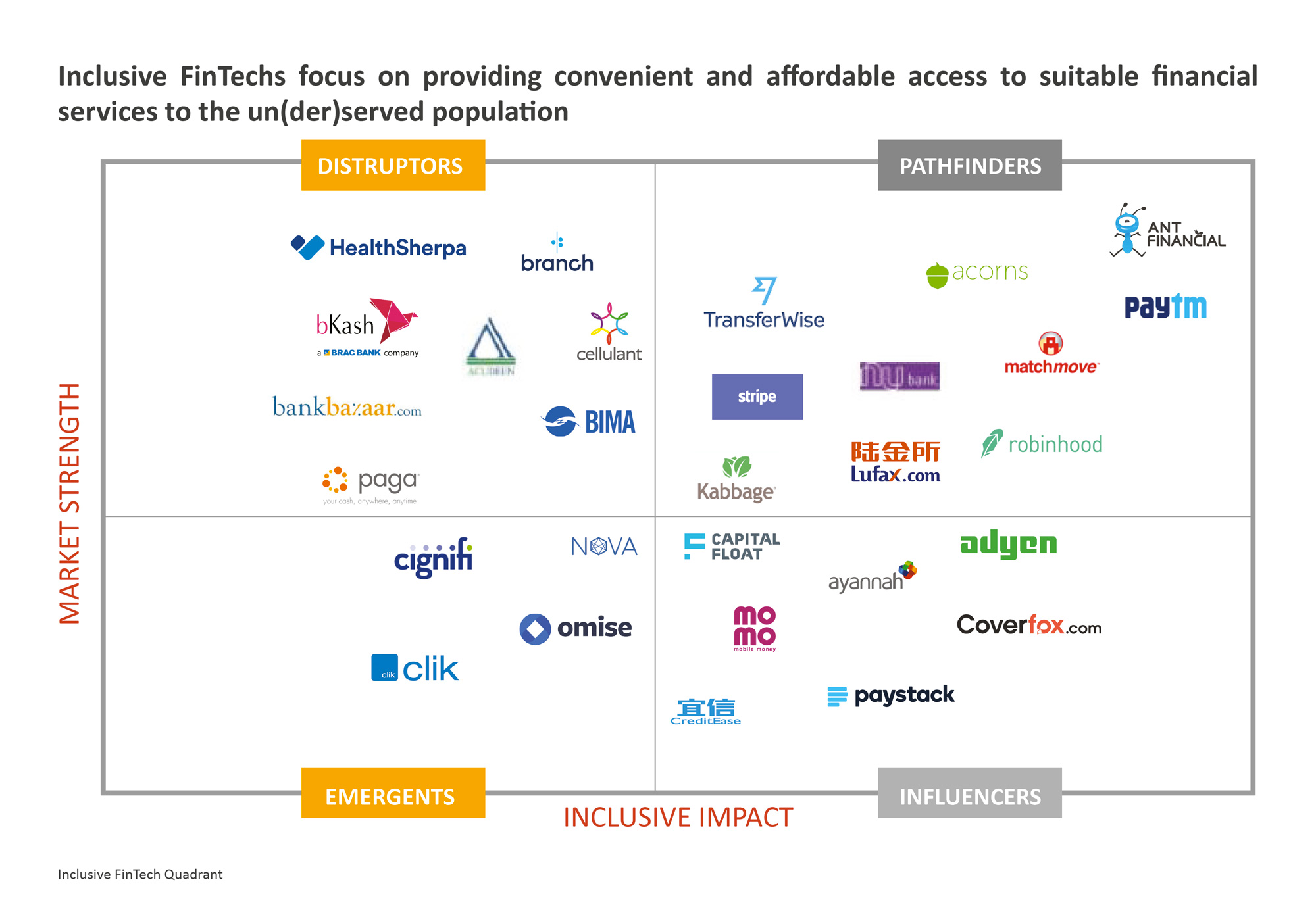

About Inclusive FinTech Quadrant

30 FinTechs are selected out of 100 across various geographies

30 FinTechs are selected out of 100 across various geographies

Selection based on “Inclusive Impact” and “Market Strength”

Inclusive Impact includes: Types of customers served (millennials, women), Inclusive Technology, Accessibility and availability of products and

services, Product mix (number and kind of products offered), Affordability of products and services

Market Strength includes: Customer growth rate, Licenses and approvals, Funding Stage, Types of Relationships, Strength of founders, Total employee strength

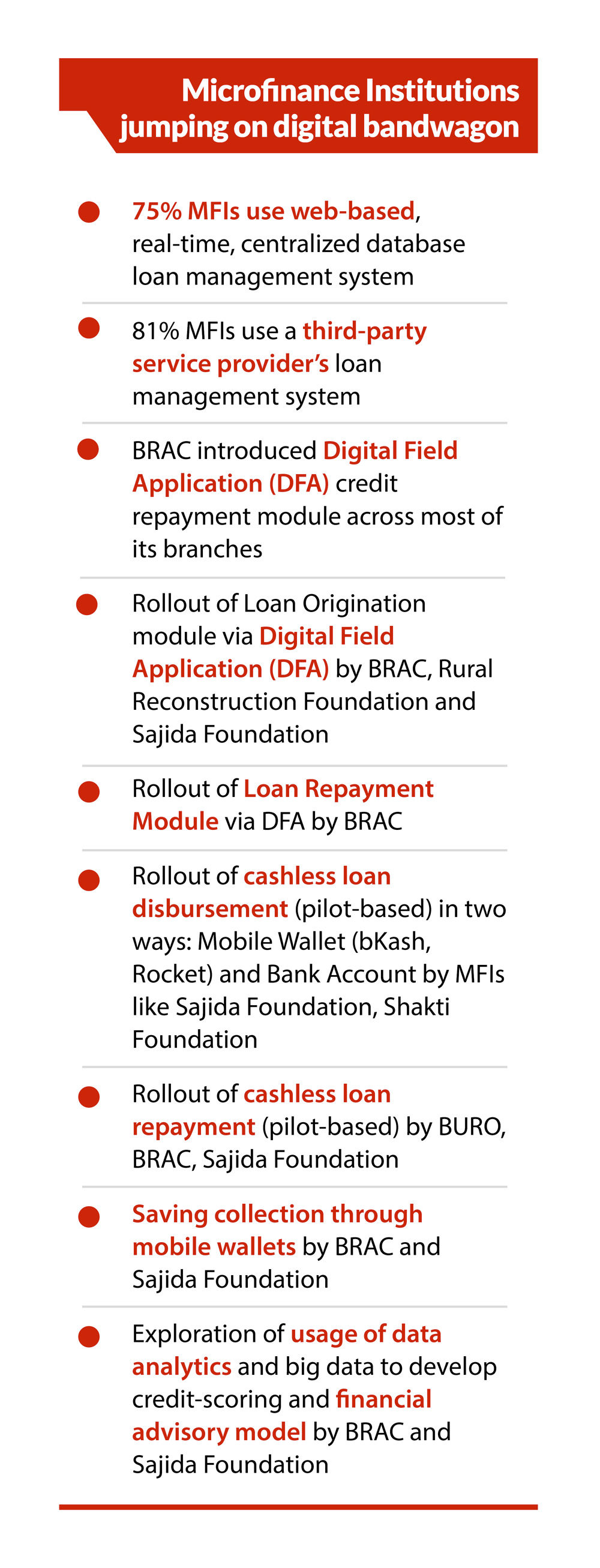

bKash, MFS of Bangladesh made its place in Disruptor quadrant demonstrating high market strength and moderate inclusive impact

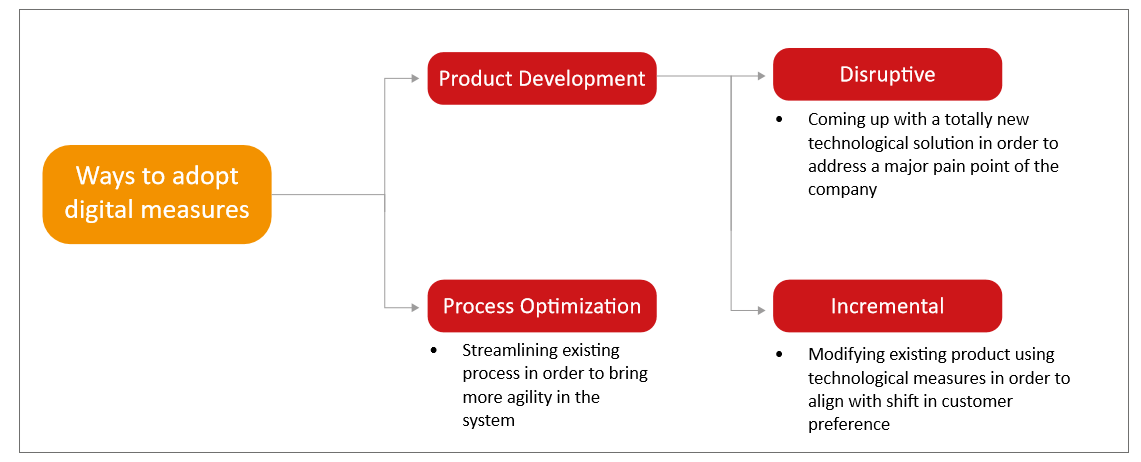

Organizations are building digital account opening, loan application and new customer onboarding processes, but the majority of these processes still require the consumer to come into the branch or have way too many steps similar to the paper-based processes of the past. And, while almost all organizations know the benefits of expanded data, advanced analytics and AI, very few have used these tools to personalize experiences or proactively offer solutions in real time.

Digitization involves disciplined adoption of appropriate standardized business processes to ensure reliability, predictability, security, and visibility into customer interactions. But identifying viable digital offerings- solutions that customers will be willing to pay for- requires experimentation.

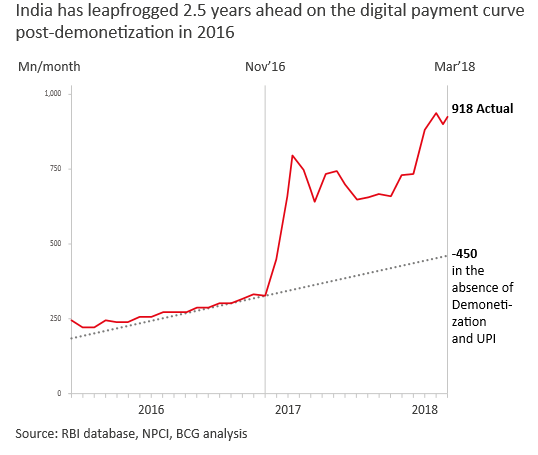

India ramping up on digital innovation

Indian banking and finance sector has long been at the forefront of innovation. From making payments to walking towards a cashless economy- banks have been opening the doors to innovation. Partnering and acquiring start-ups have become a popular method of creating an alliance with the sector. Corporates are also setting up tech labs to foster innovation. However, how India have transformed their MSME sector to become digital, is truly interesting. Currently, 85% of Indian MSMEs have smartphones. This increased access to and consumption of digital data is poised to have a significant impact on overall levels of digitization and business productivity among MSMEs in the country. As a result, in India, the cost of data has fallen by 95% in the last three years, making it the cheapest globally.

The entry of global players such as WhatsApp and Google has the potential to catalyze a step change in digital payment adoption, with small-ticket merchant

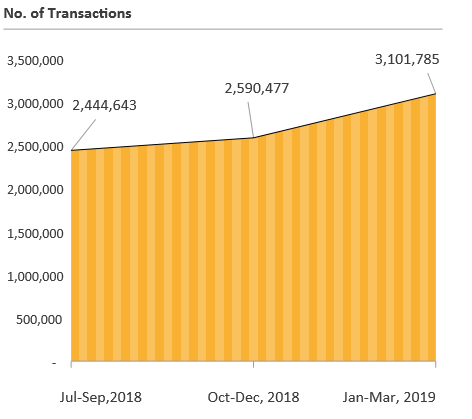

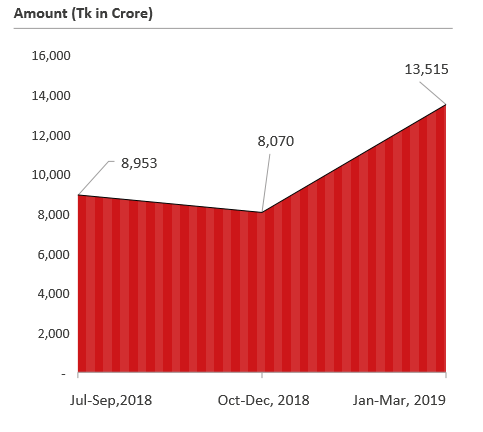

Total Digital Transactons of India

Integrating analytics with social media

State Bank of India (SBI) structured over 60 models that will help them decide on lending, setting up branches/ ATMs, launching new schemes and more. They studied over 120 branches’ data, identified trends and then used the power of social media to contact their customers directly. For instance, if a student is congratulated by his family and friends over clearing an entrance exam, SBI congratulates and makes an offer of education loan.

Partnering With E-wallets

Riding on the back of cashless economy initiatives, most of the top banks in the country have partnered with or acquired start-ups, to adapt their e-wallets and make them accessible to customers. The partnership with startups allowed the banks to grasp the advanced payment mechanism in exchange of banks’ database with the former. HDFC bank was first of its kind offering customized service collaborating with Fintech Company, MobMe in 2014. The bank’s first digital solution was ‘Missed Call Banking’ which enabled account holders to check their account balance, giving requisition for cheque book and so on without visiting the bank, which graduated to mobile banking later. Also, HDFC has partnered with PayZapp, a complete payment solutions app where the bank offers digital savings bank accounts, credit cards and instant loan to the 14 million users of PayZapp. Other banks like Yes Bank have partnered with FreeCharge and PhonePe. The alliance gives the banks easy access to technology while also providing start-ups an access to the banks’ database.

Smarter Services for Faster Growth

Another way of attracting more customers through innovation has been the launch of services by a bank that promises faster processes to a consumer. YES Bank has rolled out an initiative like SIMsePay, a service that allows a consumer to transfer money, pay bills and use other bank services, without access to the internet. Similarly, ICICI Bank’s visa-powered e-wallet Pocket eliminates the need to visit a bank. Apart from mobile recharge, bill purchase, ticket purchase and the like options, a customer can touch and pay without carrying the card at the time of purchase. Also, the app lets the user to open savings accounts anytime from the app. This feature is known as tab banking facility.

Banking in Bangladesh: Hanging back innovation

In comparison to the Indian landscape, Bangladesh is trailing behind adopting the new streams of disruption in the banking process and combating with coming out of the conservative shell. The lukewarm-responsiveness to digital means of banking ascribes to mindset of the stakeholders, unavailability and unstructured condition of data and dearth of technology-based financial service providers, mostly commonly known as Fintech. An interesting trend is discerned across the globe when innovations in banking sector comes in question, Fintechs work as the driving force behind banks’ pulling out their conventional shells.

Alternate Lending Model (BRAC)

BRAC is conducting an alternate lending model with ShopUp, though at nascent stage. ShopUp provides business development support to F-Commerce entrepreneurs, who have credit requirement, however, cannot access to finance via formal means. ShopUp provides business development support to these F-Commerce entrepreneurs and conduct their credit scoring though their algorithm based credit scoring

model. The loan amount is determined through the model and BRAC provides them digital credit. BRAC receives repayment through the startup from the sale proceeds of these borrowers and collection is also conducted by ShopUp.

New Digital Initiatives

Dhaka bank has recently launched a product named “Dhaka Bank e-Loan”, a first in Bangladesh, which will help clients get personal loans without any physical contact with the bank’s officials. Everything- from submitting loan applications to processing relevant works -- will be done through the digital platform. Initially, the loans will be available for clients with payroll accounts with the bank. For the SME sector, the lender has rolled out three digital platforms – i-Khata , i-Samadhan and Dhaka Bank MSME Bazar – to facilitate entrepreneurs.

App-based mobile banking

Banking without a mobile screen is hard to imagine in this age. Although, internet banking facility is offered by about 40 out of 57 banks in Bangladesh, only 6 banks (5 local and 1 foreign) took online banking service to the next level- The City Bank, Eastern Bank Limited, BRAC Bank Limited, United Commercial Bank Limited, Mutual Trust Bank Limited and Standard Chartered Bank. These banks rolled out downloadable apps which enable customers access their bank accounts securely from their smartphones. Services offered in these internet banking app include account to account fund transfer (including RTGS, BEFTN), utility bill and internet bill payment, mobile phone recharge, service requests such as re-issue of debit card if lost, cheque-book issue, bank statement request, loan information and the like. Fund transfer leads the internet banking transactions, accounting for 38% of the total transactions made in 2017.

Of late, City Bank and bKash, the country’s largest mobile financial services provider went into an agreement that allow Citytouch users make their credit card bill payment from their bKash wallets, Customers of bKash will be able to withdraw cash from any of the 350 City cash machines across the country, with a charge for the transactions. This is the first of its kind in the payment system in Bangladesh. In this way, a customer doesn’t have to walk to the City Bank branch to make credit card payment and bKash customers, who are out of baking reach, can enjoy banking services without having a bank account.

Digital Interactive Agent (DIA): Artificial Intelligence (AI) based chatbot

In December 2017, Eastern Bank Limited introduced an Artificial Intelligence (AI) based chatbot, called Digital Interactive Agent (DIA), which communicates with customers via Facebook Messenger and skybanking apps, providing information about their accounts, credit and prepaid cards, and general information about EBL’s products and services.

Implementing Blockchain technology

Of late, Dhaka Bank introduced blockchain technology, the first of its kind in Bangladesh, on a pilot basis to help exporters and importers carry out banking from offices or homes. The move is allowing clients to submit all export and import-related documents digitally. The businesses are being allowed to carry out trade-related procedures just by turning up at a branch once.

Challenges for banking sector to catch the “Digital Moment”

Rolling out of eKYC

The most crucial problem our banking sector is struggling with while offering digital services is, absence of eKYC in Bangladesh. Although eKYC was supposed to be rolled out by June, 2019, it got postponed. However, there are talks in the government level regarding introduction of eKYC, which is prone to roll out soon.

Dealing with unstructured data

Not until recently, the banking industry started realizing the importance of data. Banks need considerable time to streamline their wealth of unstructured data. Also, banks only keep information related to the credit behavior of customers. No such information pertaining to social /behavioral aspect of customers are recorded, which make it difficult for banks to go for alternative scorecard for lending.

Internet banking leading the way

Monthly Business Review- August 2019

In pursuit of “Digital Moment”

The global banking sector faced a new wave of change when the news of AntFinancial, Tencent and Xiaomi Corp. won virtual banking license in Hong Kong. Mobile cash is catching on in the world’s less advaced economies, in some cases, leapfrogging traditional banking. M-Pesa (Kenya) and Telenor Microfinance Bank (Pakistan) have set example of how unbanked citizens increasingly use phones to connect to the digital economy.

Modern digital technology has disrupted this legacy banking model on all levels, starting from enhancing customer experience to bring agility in the credit operation to streamlining back-office related activities, by simply leveraging on customer data. In a world where “data is king”, the cutting-edge technological inventions transformed the aura of banking services in the past two-three years. In India, ICICI Bank, HDFC Bank, Axis Bank and SBI are now deploying big data to customer profiling, collaborating with e-wallets to make the payment system more convenient, putting analytics into play in creating loan scorecards and gradually partnering with fintechs to leverage their technology for superior customer experience.

Bangladesh, albeit trailing far behind from neighboring India when innovation in banking service is in question, however, started making strides. The top banks of Bangladesh are showing an interesting trend in the commitment of organizational leadership for offering digital banking services. Few initiatives by local banks for instance, coming up with paperless e-loan for individual purpose, implementing blockchain technology (pilot basis) for trade finance, partnering with e-wallet (iPay and bKash) and so forth. Although regulatory challenge, for instance, eKYC is still there, the good news is it is being addressed from policy level. It is time regulators should undertake more “digital-friendly” initiatives so that local banks start putting data and technology into play to provide one-stop, paperless and on-the-go banking solution to its customers.

Download View