Dr. Ahsan H. Mansur Executive Director, Policy Research Institute

MBR had the privilege to get the insight from Dr. Ahsan H. Mansur, Executive Director at the Policy Research Institute, and a former Economist of International Monetary Fund (IMF), regarding the recently liquidity situation in Banking sector of Bangladesh.

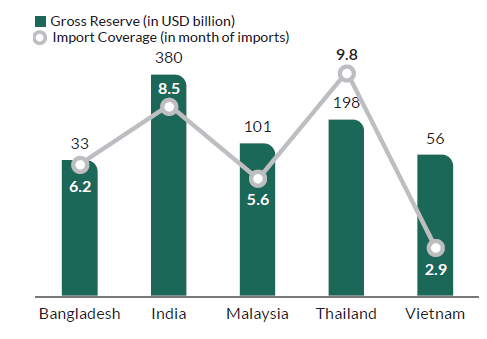

The Bangladesh Bank announced its Monetary Policy Statement for the second half of FY2019 on January 30, 2019. The statement reflects the commitment of the Central Bank to coordinate its policies in line with the government’s agenda to sustain real economic growth with ongoing macroeconomic stability. However, Bangladesh Bank faces a number of challenges in a number of fronts in executing its announced MPS. One such area is managing the balance of payments (BOP). In the early months of FY2019, the condition improved slightly in the provisional figures for the current account balance (CAB), although it still recorded a $4.3 billion deficit in the seven months of FY2019 and may approach $8 billion by the end of the fiscal year. The BOP’s weakening has contributed to instability in the exchange market. During FY2019, Bangladesh Taka’s exchange rate against the US dollar depreciated slightly. By intervening in the foreign currency market, BB had attempted to stabilize the exchange rate by selling $1.3 billion by January 27, 2019. However, it is not possible to intervene indefinitely. In addition, some banks refuse to open LCs at the rates dictated by the BB on behalf of their customers due to a shortage of foreign exchange in the interbank market. The gross official reserve has not increased in dollar terms in the last four years, whereas imports have increased significantly. Thus, the reserve coverage for import payments has dropped significantly and is likely to fall further. The reserve level is still comfortable at six months of reserve coverage and compares well relative to its regional peers. Since Bangladesh Banks’ reserve coverage has already declined by two months, this type of rapid fall cannot continue for long, flexible and market based exchange rate management is the way forward.

Deviation of MPS in Policy Operation

Obviously there is a wide gap between what BB said about exchange market operations in the MPS and what it still practices. Since the statement in the MPS with regard to market-based exchange rate determination is widely supported, an actual change in BB’s operational-level exchange rate policy was expected, especially after the national elections. But that’s still to be done. Such a move would certainly lead to Taka’s further depreciation against the US dollar, but that would be consistent with the dollar’s appreciation against all major currencies in the global exchange markets. This type of adjustment would also help boost exports and contain pressures for excessive import growth, thereby helping to restore BOP’s balance and a resumption of BB’s foreign reserve growth. Bangladesh needs to increase or at least maintain its current level of reserve coverage and also increase money market liquidity.

The emergence of the liquidity issue in 2018 pushed up the banks ‘ interest rate structure and this has not happened overnight. The increased inflow of NFA since FY12, which lasted through FY16, was a major source of injection of liquidity into the banking system. Simply put, the domestic liquidity / broad money expanded by about BDT 80 or more for every US dollar of NFA growth. Furthermore, BB’s significant intervention in the foreign exchange market also reduced liquidity in the banking system. It effectively withdrew BDT 83 for every US dollar that the Central Bank sold.

The manner in which Bangladesh banking system is expanding—characterized by rapid accumulation of non-performing assets and increasing number of new banks—is also contributing to further tightening of liquidity in the banking system. Many banks, especially the new ones, were engaged in excessive lending beyond the limits established by BB’s macro prudential conditions. As BB started to focus on this issue and started to exert pressures on banks to comply with the macro-prudential conditions, this resulted in a general tightening of lending, pushing up the interest rate structure in early 2018. This increase, however, should not be blamed on the Central Bank’s intervention in terms of enforcing macro-prudential conditions as it must do. Against this background, the banking system’s deposit growth rate slowed from a healthy rate of about 20 percent to less than 10 percent in FY2019 contributing to further tightening of liquidity.

Roadblocks in Achieving Market Based Lower Interest Rate

BB and the government must address the fundamentals— not superficially, but at the core issues— that contributed to the decline in liquidity and to higher interest rates. To improve liquidity, one dimension is to manage the exchange rate and export diversification policy proactively to restore BOP equilibrium with positive impact on BB’s gross and net official foreign exchange reserves. Addressing loan loss can help inject liquidity in the banking system. The diversion of funds towards the National savings certificated, as described below, also must stop to retain liquidity in the banking system.

In addition to increased liquidity in the banking system, lowering the domestic interest rate structure would also require a number other positive developments, such as, improving the efficiency of the banking system and its intermediation role and a deceleration of the rate of inflation. . For example, if the inflation rate is 2.5 percent, banks can offer 3 percent deposit rate, providing depositors with positive real interest rates. This essentially implies that BB / government should not be complacent about Bangladesh’s inflation performance and should continue to aim for a lower inflation target. Countries with lower interest rate structures generally also enjoy lower inflation rates.

The other way to help reduce the lending rate is to lower the spread between lending and deposit rates. This lowering of spread will require measures on multiple fronts. Large number of banks essentially means very large overhead cost for the banking system as a whole. The overhead costs include head office costs and high cost of qualified top management in an environment of increasing shortage of qualified senior bank staff. Cost of automation and putting in place cyber security systems are very costly and more so for smaller banks with lower asset base. The only way these major overheads can be contained or reduced to generate savings is reducing the number of banks by consolidating the banking system through mergers and acquisitions of weaker banks with stronger ones as it is often done in other countries.

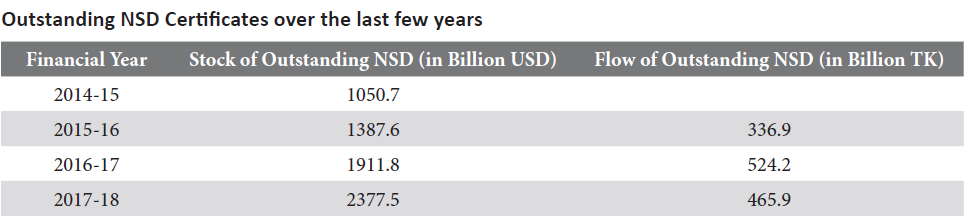

Savings Certificates issued by the National Savings Directorate (NSD) is a major stumbling block in achieving market-based interest rate structure. As seen from the Table below, the outstanding stock of NSD instruments increased from a little over Tk. 1 trillion in FY15 (accumulated over the last 45 years since independence in 1971), to almost Tk. 2,4 trillion within a 3-year period through FY18. This massive diversion of funds away from the banking system contributed to the serious liquidity problem in the banking system and limited the balance sheet expansion of commercial banks and their profitability.

In order to achieve a level of lending rate structure that will enhance Bangladesh’s competitiveness and promote investment and growth objectives, market based interest rates will require a far deeper level of policy undertakings as described above. Banks can not expand lending without a commensurate increase in deposit base while adhering to BB’s macro prudential requirements.

In the Near Term, Limiting Government Borrowing from the Banking System will Support Private Sector Lending

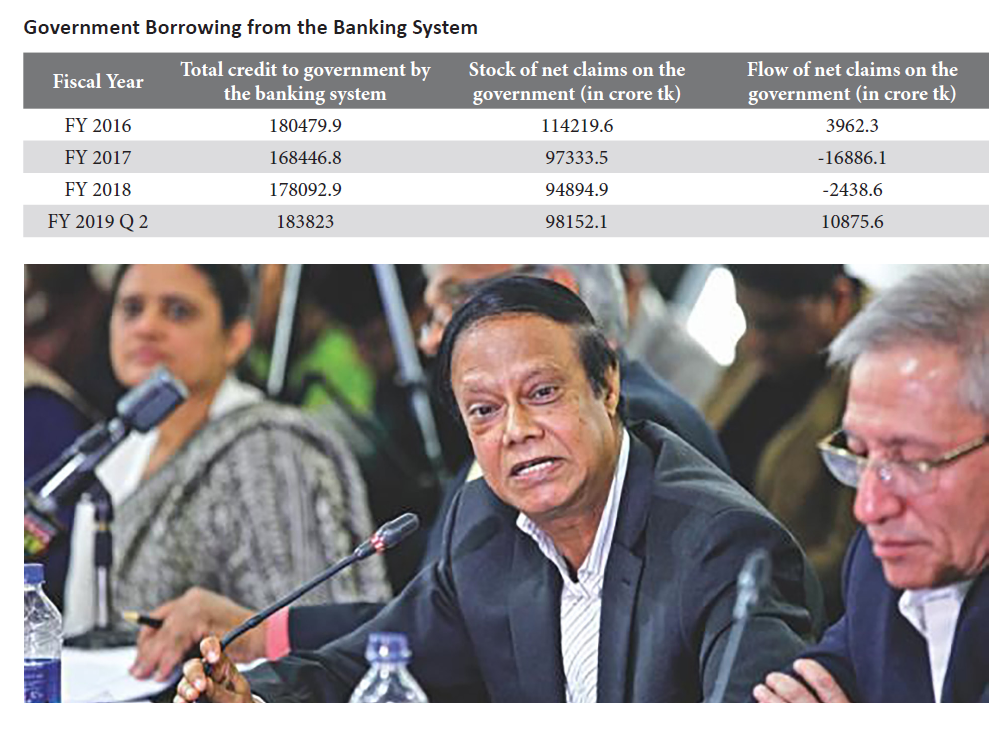

A new development in FY 19 is that the government has renewed its borrowing from the banking system after several years giving rise to the potential crowding out of the private sector credit by the government, Until FY2019, government borrowings from the banking system were negative indicating that the government paid back the banking system on a net basis because of much larger borrowings through the issuance of NSD instruments. This situation has changed, and despite continuing heavy NSD borrowing, in the financial year 2019 the government borrowed heavily from the banking system. The increasing recourse to government bank finance is attributable to the very weak revenue performance of the National Revenue Board. The fiscal revenues of the NBR only increased by less than 7% over the first seven months of FY 19, compared to the budget target of 43%. The huge deficit in projected government revenue is likely to result in crowding out of the already diminishing private credit. Such an outcome that is currently unfolding will not support real GDP growth at an above 8 percent rate.

Monthly Business Review- May 2019

During July-February of FY 2018-19, the net sale of National Savings Certificate (NSC) exceeded the target for the entire fiscal by 35%, already BDT 5,602.49 crore worth of NSCs sold against the target of BDT 26,197 crore. Deposit mobilization for the same period registered only 9.6% average growth. On the other hand, according to media reports, USD sale by Central Bank increased to a greater extent, to the tune of USD 1.87 billion in July to March of FY2018-19, whereas BDT 84 for USD 1 sale is being withdrawn from banking system.

Central Bank already took measures to address the liquidity situation, for instance, reducing the Cash Reserve Ratio (CRR) to 5.5%. However, sale of NSCs can only be ensured to those in need of social safety net. Also, it is high time Government should focus on money market (banking system) and capital market (bond) as alternative source of funding.

Download View