Liquidity in local banking sector

The banking sector is currently going through a phase where, such instances where banks are not being able to disburse credit even after sanction of proposals, are evident now.

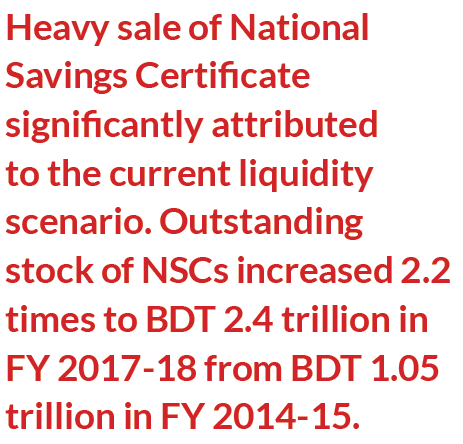

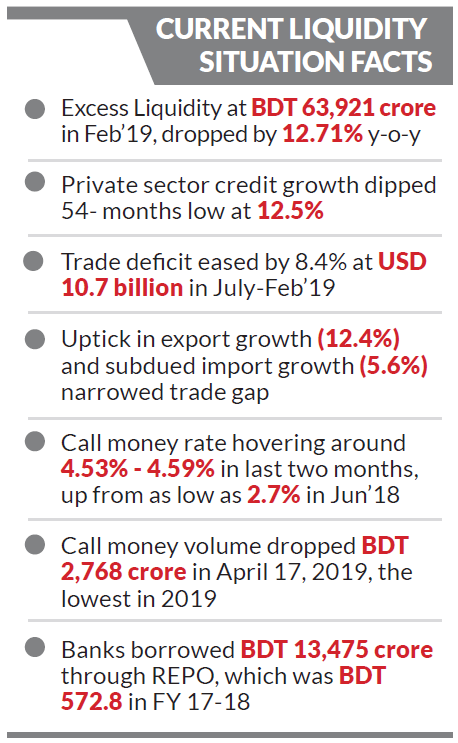

Private commercial banks are combating a tight liquidity condition at this moment. Excess liquidity dropped as low as BDT 63,921 crore in February’19, a slump of BDT 3,721 crore from January’19 and the lowest in last 37 months. As a resulting impact, frequent interest rate hike on loan products are evident in banking sector. The excess liquidity in banking sector crossed BDT 1-lac crore mark in 2015 and after May 2017, it never moved to the 1-lakh crore territory. The upward and downward movement of excess liquidity has been a cyclic phenomenon over these years. Spiraling net sale of National Saving Certificate (NSC) is a reason that a significant portion of money could have otherwise been channeled into traditional banking sector. The high interest rate offered on NSC lured the depositors to choose it as their most preferred method of investment, compelling banks to be left with a sloth in deposit growth.

On another note, high import growth intensified the liquidity situation, as Central Bank is selling US Dollars to the private commercial banks so that the banks don’t fail payments on Letter of Credits. Alongside, both export and remittance portrayed a depressing picture for a long time, which further widened the Balance of Payment (BoP).

Liquidity Scenario explained

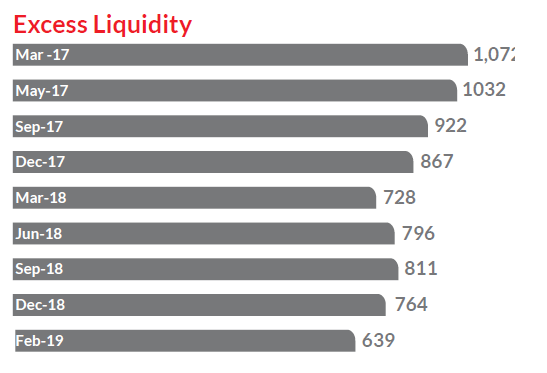

Over the last two years, the liquidity scenario of banking sector took a U-turn. Banking sector was sitting on excess liquidity worth of BDT 1.23 lakh crore

in December 2016, at a time when private sector credit growth stood at 15.5%, below than its 16.6% target. The problem was exacerbated by the fact that investors did not see attractive growth for private sector investments.

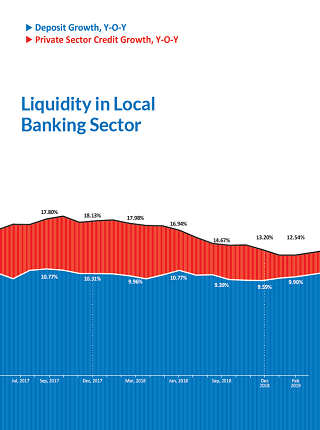

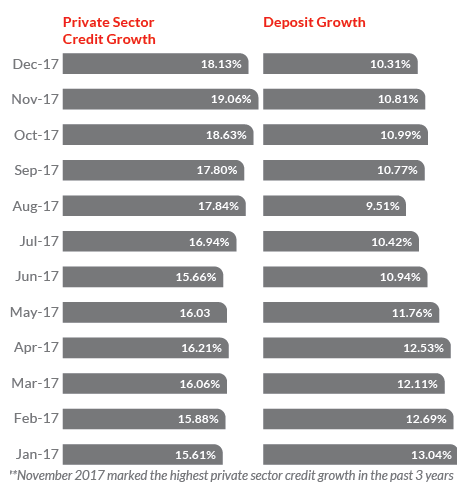

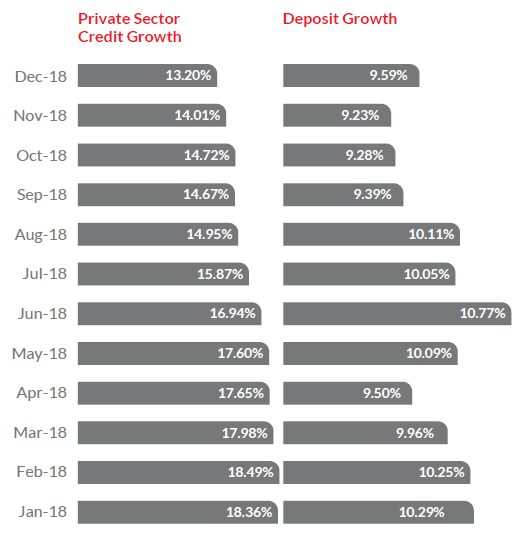

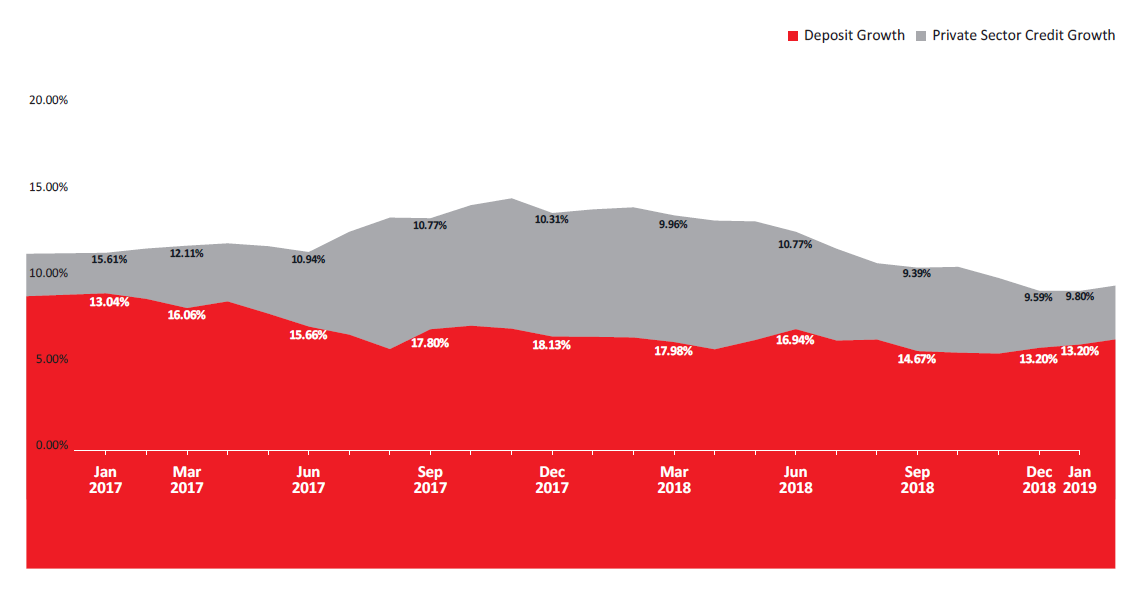

Surplus liquidity of banking sector amounted to BDT 1.26 lakh crore in January 2017. In a bid to make effective utilization of the excess money and achieve the private sector credit growth target given by the Central Bank, banks started disbursing loans at a high volume. The year 2017 started with a private sector credit growth at 15.61% level and ended at 18.13% level. November 2017 marked the highest private sector credit growth of 19.06%. SME market also got a significant drive in 2017, marking the highest SME loan disbursement amounting to BDT 161,811 crore.

However, on the other hand, deposit growth in 2017 registered a steady growth. During 2017, banks have received a total deposit of around BDT 85,000 crore, while they disbursed loans around BDT 1,25,000 crore. The weighted average interest rate on deposit was 4.95% in 2017 and it was as low as 4.84% in June 2017. Because of the low interest rates offered by the banks, investors took interest in National Savings Certificate, which is comparatively safer and lucrative investment option to commoners.

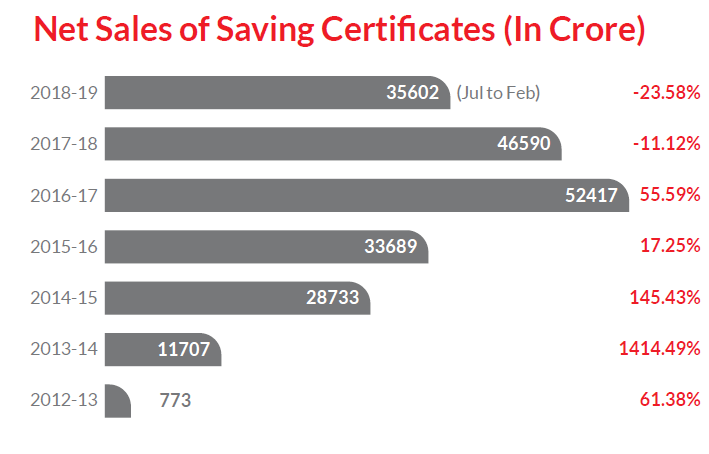

The government’s net sales of NSCs stood at BDT 35,602.49 crore in July-February of FY19, up BDT 6,405 crore on the government’s BDT 26,197 crore budgetary target for the entire fiscal year.

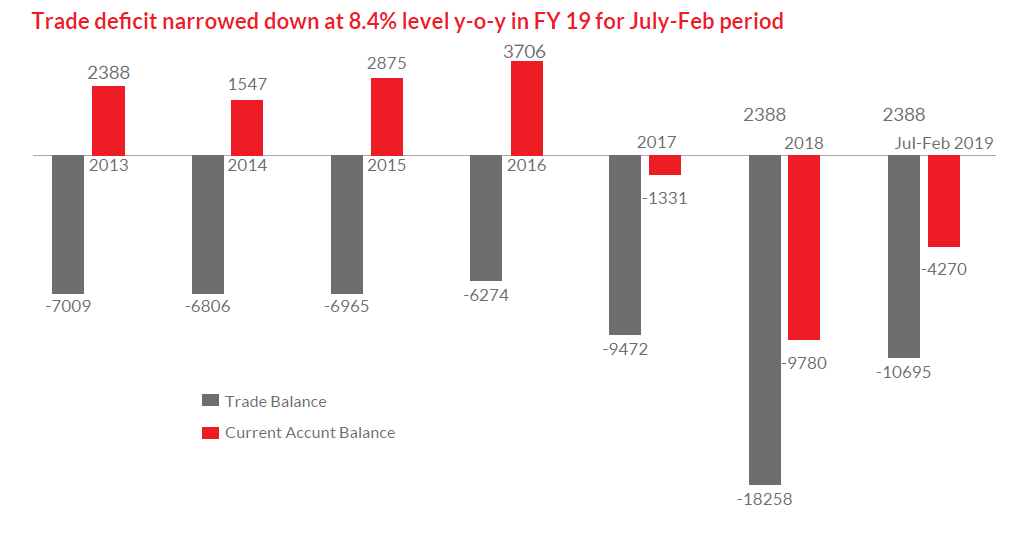

Not only excessive credit disbursement, soaring demand for import from businesses were the main reasons for plummeting excess liquidity. The trade deficit stood at USD 8.62 billion at the end of December 2017, with current account deficit registering USD 4.34 billion in FY 2017-18. The import of capital machinery and industrial raw materials has registered a significant growth in the first half of 2017-18. In July’17, trade balance went into negative territory for the first time in the past 15 years and current account balance registered deficit for the first time since FY’13. The sudden increase of import payment has led to a 2.5% depreciation of the local currency against the dollar in the July-December period of FY 2017-18. Current account deficit plunged into deficit zone, ascribing to a moderate growth in export and remittance.

The year 2018 started with the Central Bank’s regulation of lowering the ceiling of Advance-Deposit Ratio (ADR) by 1.5 percentage points to 83.5% in order to put a check on banks’ heavy credit disbursement. Although, the deadline of new ADR limit was extended upto December 31, 2018, banks started focusing on attracting investors to opt for deposit products by increasing the deposit rate. Also, in an effort to keeping the ADR below the target, the private sector credit growth also started plummeting.

To provide for further cushion, on April 2018, the Central Bank reduced the Cash Reserve Ratio (CRR) by one percentage point to 5.5% to ease the liquidity condition. The reduction of the CRR eased the liquidity condition. The resulting impact of these measures reflected on increasing liquidity base from March’18, at BDT 72750.03 Crore to BDT 79649.69 crore at Jun’18.

However, again the liquidity base started eroding since September 2018. Between July 2018 and January 2019, the government’s bank borrowing stood at BDT 4,451 crore. In contrast, a year earlier it did not borrow any fund but repaid BDT 15,030 crore to adjust its previous lending.

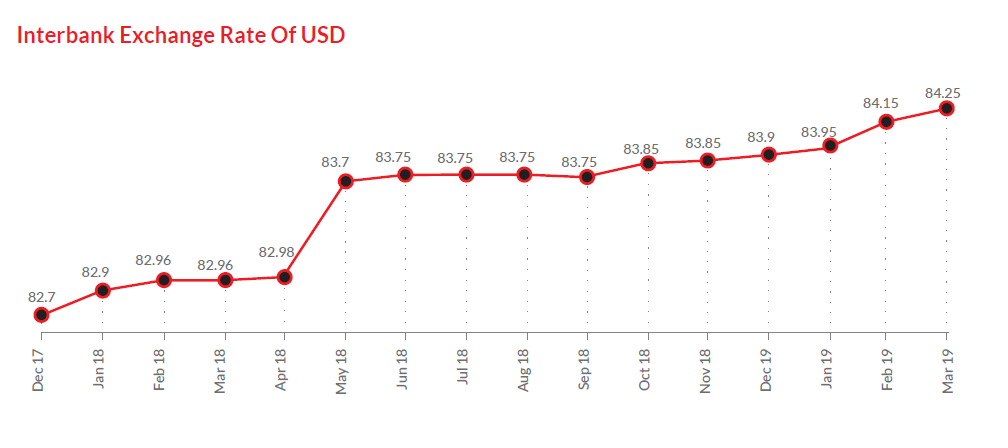

High import expenditure and low export earnings made the currency market volatile by widening demand-supply gap of US Dollars. Since 2017, foreign currency payments has been a challenging task as the dollar price is on the rise. In 2017, USD 46,345 million import LCs were settled, whereas, the same grew at 17% level to USD 54,189 million in 2018. Export earnings and remittances have not kept pace with imports and this resulted in a shortage of dollars. In order to ensure stability in the currency market, Bangladesh Bank sold USD 1.87 billion in July to March of FY2018-19 according to media reports.

The rising demand for dollar compelled Bangladesh Bank to devalue the local currency gradually, which stood at BDT 84.25 in March 31, 2019. The devaluation of local currency, ascribing to higher import growth, put pressure on the liquidity market as well.

According to Bangladesh Bank’s latest data of January 2019, banking sector is sitting on BDT 67,642 crore excess liquidity, a 12.9% reduction y-o-y. Riding on higher demand for liquidity, call money rate increased to 4.53% in April 2019, which was 2.77% in June 2018. The call money rate hovered around 4.53% - 4.59% in the last two months. Alongside, the call money volume dropped as low as BDT 2,768 crore in April 17, 2019, the lowest in 2019.

Banks borrowed BDT 13,475.8 crore from the central bank through repurchase agreement (REPO) in the period between July, 2018 and March 5, 2019, while the entities borrowed BDT 572.86 crore in the entire FY 2017-2018. In FY 2016-2017, banks’ borrowing through REPO was BDT 115.67 crore.

How to win over the tight liquidity condition

The Central Bank took some policy measures in order to ease the liquidity condition. Also, another move by the government to address the current liquidity situation is, allowing the State-owned Enterprises (SoEs) to deposit 50% of their funds with the Private Commercial Banks (PCBs), up from 25%. However, some core areas need to be worked on if liquidity condition is actually to be addressed:

![]() For FY 18-19, the target of net sale of NSC has already been achieved and exceeded by 35%. Unless Government takes measures to control the sale of NSCs, traditional banking sector may always have a potential loss of substantial cash flow. If Government can ensure the sale of NSCs to those in need of social safety net, naturally the overall sale will have a decreasing impact.

For FY 18-19, the target of net sale of NSC has already been achieved and exceeded by 35%. Unless Government takes measures to control the sale of NSCs, traditional banking sector may always have a potential loss of substantial cash flow. If Government can ensure the sale of NSCs to those in need of social safety net, naturally the overall sale will have a decreasing impact.

![]() Bond market needs to play a strong role as an alternative source of raising fund.

Bond market needs to play a strong role as an alternative source of raising fund.

![]() Our export basket is heavily dependent on RMG, which has been the case for decades. It is high time Government should take adequate measures to diversify the export basket so that trade balance and exchange rate remain within control.

Our export basket is heavily dependent on RMG, which has been the case for decades. It is high time Government should take adequate measures to diversify the export basket so that trade balance and exchange rate remain within control.

Monthly Business Review- May 2019

During July-February of FY 2018-19, the net sale of National Savings Certificate (NSC) exceeded the target for the entire fiscal by 35%, already BDT 5,602.49 crore worth of NSCs sold against the target of BDT 26,197 crore. Deposit mobilization for the same period registered only 9.6% average growth. On the other hand, according to media reports, USD sale by Central Bank increased to a greater extent, to the tune of USD 1.87 billion in July to March of FY2018-19, whereas BDT 84 for USD 1 sale is being withdrawn from banking system.

Central Bank already took measures to address the liquidity situation, for instance, reducing the Cash Reserve Ratio (CRR) to 5.5%. However, sale of NSCs can only be ensured to those in need of social safety net. Also, it is high time Government should focus on money market (banking system) and capital market (bond) as alternative source of funding.

Download View