Things to Know about Credit Card

Credit card has become essential nowadays for all, especially to the younger generation. But although it is a great thing to have around, as in an emergency the credit card allows the user to access money immediately, credit card can become harmful without careful utilization of its facilities it.

How to get Benefit from Credit Card

![]() Buy things online: Credit card is a really useful tool to buy things online

Buy things online: Credit card is a really useful tool to buy things online

![]() Spreading the cost of purchase over months: Credit card is useful when someone is planning to purchase something with an EMI to reduce big cash outflow in a single month

Spreading the cost of purchase over months: Credit card is useful when someone is planning to purchase something with an EMI to reduce big cash outflow in a single month

![]() Incentives and discounts: Credit cards usually come with a variety of offers when used to make payment, such as free product or service, discounts from stores, lounge access at airports etc.

Incentives and discounts: Credit cards usually come with a variety of offers when used to make payment, such as free product or service, discounts from stores, lounge access at airports etc.

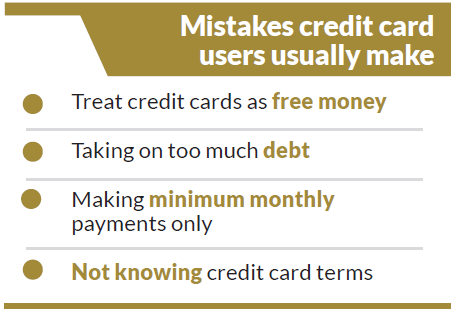

What to Check about Credit Card

![]() Annual Percentage Rate (APR): This is the cost of borrowing on the card, if the whole balance is not paid off each month. It can either be a fixed rate or a variable rate that is tied to another financial indicator. However, even a card with a fixed interest rate can change based on certain triggers, such as paying a card late, or going over the credit limit. Go for the card which has, or appears to have, the lowest APR.

Annual Percentage Rate (APR): This is the cost of borrowing on the card, if the whole balance is not paid off each month. It can either be a fixed rate or a variable rate that is tied to another financial indicator. However, even a card with a fixed interest rate can change based on certain triggers, such as paying a card late, or going over the credit limit. Go for the card which has, or appears to have, the lowest APR.

![]() Credit limit: This is the amount of money that the credit card issuer is willing to let the card holder borrow. It is undesirable to find oneself in a situation in which he or she is close to maxing out the credit limit. It can hurt the credit score, carries the risk of getting credit limits cut to an amount that’s lower than the current, and also there is a penalty when that happens.

Credit limit: This is the amount of money that the credit card issuer is willing to let the card holder borrow. It is undesirable to find oneself in a situation in which he or she is close to maxing out the credit limit. It can hurt the credit score, carries the risk of getting credit limits cut to an amount that’s lower than the current, and also there is a penalty when that happens.

![]() Minimum repayment: This is an amount that has to be repaid if the balance is not paid off each month. This amount should be minimum.

Minimum repayment: This is an amount that has to be repaid if the balance is not paid off each month. This amount should be minimum.

![]() Annual fee: Some cards charge a fee each year for use of the card. The fee is added to the amount due and interest on the fee has to be paid as well as on the spending, unless it is paid in full. But if spending is high enough, a fee card may net higher rewards.

Annual fee: Some cards charge a fee each year for use of the card. The fee is added to the amount due and interest on the fee has to be paid as well as on the spending, unless it is paid in full. But if spending is high enough, a fee card may net higher rewards.

![]() Charges: These range from going over credit limit, for using the card abroad and for late payments.

Charges: These range from going over credit limit, for using the card abroad and for late payments.

![]() Introductory interest rates: Initially the rate is low or there is none at all. The rate then increases after a certain amount of time. Look at how long the introductory rate lasts as well as the interest rate it changes to at the end of the introductory period.

Introductory interest rates: Initially the rate is low or there is none at all. The rate then increases after a certain amount of time. Look at how long the introductory rate lasts as well as the interest rate it changes to at the end of the introductory period.

![]() Loyalty points or rewards: Check for the variety of shops or transactions where these rewards can be used. Also, the card should offer loyalty points for those goods or services that are relevant for the card holder. Rewards can also include cash back offers.

Loyalty points or rewards: Check for the variety of shops or transactions where these rewards can be used. Also, the card should offer loyalty points for those goods or services that are relevant for the card holder. Rewards can also include cash back offers.

The attractiveness of a credit card comes down to the spending habit. There is not one particular card out there that fits the bill for all. Careful evaluation of the pros and cons of a credit card before getting one can make life more convenient.

Monthly Business Review- April 2019

Banks/FIs deserve accolades for expanding their SME portfolio over the past years and thus exceeding the SME disbursement target given by the Central Bank. However, the financial industry is still saddled with some concerns when SME lending is in question. Banks find it hard to consider SME loans as a core focus segment because of the higher cost of monitoring and underwriting, as SMEs are scattered all across the country and are unstructured in terms of account management. Therefore, underwriting of SMEs is expensive and time-consuming since the cost and underwriting process for all borrowers (irrespective of size and value) are similar. FIs can come up with scoring models for SME businesses by deploying technology leveraging on the huge set of customer data. Also, more than just funding, small businesses require business management tools and advice on how to

diligently manage working capital and FIs are the best fit to help them out in this scenario.

Lastly, this is worthy to mention that the whole financial industry played a crucial role in building SME ecosystem and educating the market at this level, with prudent guidance from the Central Bank. Now, expanding the SME market reach in a low cost manner, by deploying technology should be the priority of Banks or FIs.

Download View