Syed Abdul Momen: Head of SME, BRAC Bank

Surfing on the Wave of SME Banking

Syed Abdul Momen is the head of SME Banking at BRAC Bank. He joined BRAC Bank in August 2005 and has been instrumental in making BRAC Bank the undisputed leader in the small business lending space in Bangladesh. He has over 18 years of multifaceted experience in the Banking Sector across Technology, Operations and Business Functions.

Syed Abdul Momen

Head of SME, BRAC Bank

Growth avenues in SME sector and SME financing

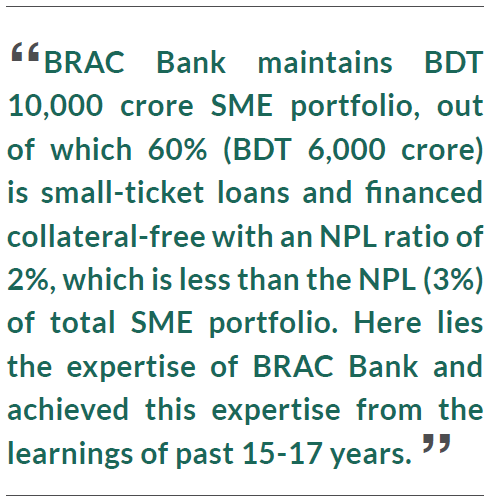

Bangladesh has come a long way in SME financing, particularly because of the role of government and Central Bank. BRAC Bank is owned 48% by BRAC which has been doing micro and small business financing since 1972, right after independence. Since 2000, BRAC found a gap in the market- none of the banks financed small businesses without collateral. BRAC Bank was formed in 2001 with a view to financing the SMEs, not the large ticket ones. Invariably in all banks, average SME ticket size is around BDT 50 lacs, whereas it is BDT 8.5 lac in BRAC Bank. Due to having small ticket size, BRAC Bank finances a large volume of clients.

Every month BRAC bank disburses around 7000 loans, out of which 60% is new-to banking.

Over the last 10 years, more banks have come under the umbrella of SME financing, thanks to the policy initiatives by Bangladesh Bank. An internal survey result showed that almost 80% of the SMEs had their first account opened at BRAC Bank, which proves that BRAC Bank made the businesses bankable. Gradually, the learnings from BRAC Bank trickled down to the industry and educated the market. Especially, over the last two years, margins in other business segments have shrunk driven by liquidity crunch and so banks are moving towards SME financing. Moreover, as per the central bank regulation, all banks must have 30% of their total portfolio in SME lending by 2025, which is another driving factor.

Research shows that SMEs contribute to 25% of our GDP and provide 80% of the employment as well. According to a study by Daffodil University, the growth of medium businesses in Bangladesh is 13% whereas small businesses grew by only 10%. If small businesses grew at a much larger scale, it would be possible to achieve double digit GDP growth in the Bangladesh economy.

Collateral-free small SME lending is the key focus of BRAC Bank

Over this span, the institution has followed 3 different models, all of these having some pros and cons. At one point, NPL went up to as high as 18-19% in the SME sector. The model currently followed is a decentralized one. Credit is decentralized while the business acquisition model is sales team based. BRAC Bank has around 2000 sales people spread across the country with 460 unit offices and 186 branches. The SME Unit Offices are small sales offices with only SME loan processing facility which comprises of 2-3 sales persons in each office based on business volume. 260 SME Unit Offices operates as a stand-alone basis and Disbursement and collection take place primarily through corresponding banks. Last year, BRAC Bank embarked on its journey with agent banking by obtaining its license. By this year, 260 locations will be converted to agency and there will be no dependency on corresponding banks.

BRAC Bank’s current operating model is designed by establishing accountability in each and every role which are involved in the life-cycle of the loan –

![]() The Acquisition Team is responsible for collection

The Acquisition Team is responsible for collection

![]() The Credit Approver visits each and every business and provides approval

The Credit Approver visits each and every business and provides approval

Along with accountability, a strong governance culture is also established. Previously, internal control team used to visit every office once every 3 years which was very ineffective. Now, BRAC Bank established a monitoring team of more than 300 people. They visit each SME Unit Office once every 3 months and also talk to the customers of that unit.

Once loans are long overdue (more than 90 days), BRAC Bank’s Special Asset Management (SAM) team comes. SAM comes early because BRAC Bank wants to intervene at early stage and take decisions on the loan early. SAM Team comprises of Legal Experts.

Coming up with market-tailored products

The SME lenders must have top-notch market knowledge. Currently, SME products are much like “one size fits all”. A substantial portion of SME business is seasonal, and 80% of transactions are seasonal. Cash flow is not the same throughout the loan period. During production, there are more cash requirements and during sales, inflows are high. Products need to be designed based on the cash flow cycle which will make customers’ life easier. This area is largely missing. BRAC Bank is in the process of developing such product and discussing the idea with Central Bank. The key issue is, if banks want to serve customers, they must customize.

Educating the market- the core challenge of SME Financing

The level of education and the business documentation among SME customers is not up to the mark. Many customers still use notebooks for sales record keeping. BRAC Bank’s loan officers sit in the shops during peak times, observe customer frequency to the shops, recreate financial statements and give the sales format to the customer so that s/he maintains proper recording. If the customers come for repeat financing, it will be easier to process. In this manner, BRAC Bank is educating this vast SME market. They prefer hands-on training more than classroom training for SME customers. There are other challenges regarding compliance of businesses, including absence of trade licenses and tax identification number.

Initiative from policy level

Banks need to have the liberty to design their own products. In addition, there are definition problems which people take advantage of. For example, in the new definition for trading concerns, if yearly turnover is less than BDT 12 crore, it is considered as Small Business and more than that is considered as large corporate. This is not practical and the bank is proposing to Central Bank to relook at these limits especially for Small & Medium sized trading concerns.

Emergence of fintech in the SME sector

Recently, many international FinTechs tried to venture into creating digital credit model for Bangladesh by analyzing the available data points. Unfortunately, no one could come up with a decisive model as the Quality & depth of data is good enough to establish a model. Thus digitalized credit lending has a long way to go in Bangladesh. However, in recent times, many Payment Service Providers are investing in building this ecosystem.

Monthly Business Review- April 2019

Banks/FIs deserve accolades for expanding their SME portfolio over the past years and thus exceeding the SME disbursement target given by the Central Bank. However, the financial industry is still saddled with some concerns when SME lending is in question. Banks find it hard to consider SME loans as a core focus segment because of the higher cost of monitoring and underwriting, as SMEs are scattered all across the country and are unstructured in terms of account management. Therefore, underwriting of SMEs is expensive and time-consuming since the cost and underwriting process for all borrowers (irrespective of size and value) are similar. FIs can come up with scoring models for SME businesses by deploying technology leveraging on the huge set of customer data. Also, more than just funding, small businesses require business management tools and advice on how to

diligently manage working capital and FIs are the best fit to help them out in this scenario.

Lastly, this is worthy to mention that the whole financial industry played a crucial role in building SME ecosystem and educating the market at this level, with prudent guidance from the Central Bank. Now, expanding the SME market reach in a low cost manner, by deploying technology should be the priority of Banks or FIs.

Download View