Exports to Jobs: Boosting the Gains from Trade in South Asia

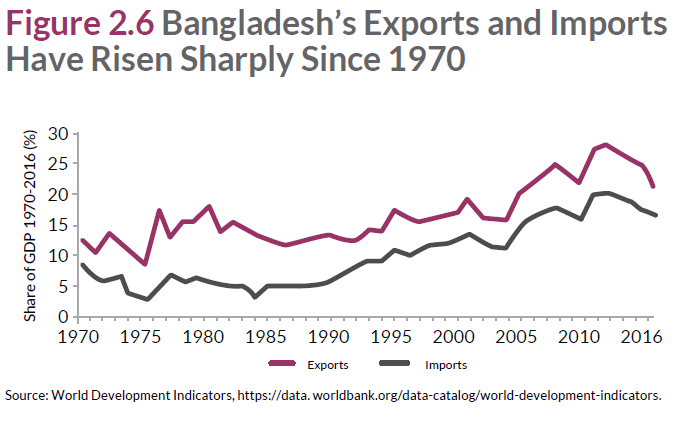

Bangladesh being strong in export growth

Bangladesh went through 56% population increase from 106 million in 1990 to 166 million people in 2018. The rate will be lower than the growth of working age population growth in near future. In Bangladesh labor force participation rate declined from 60 to 58 percent, which indicates that Bangladesh needs additional labor force. Bangladesh managed to improve the gender balance with increase of women’s participation in different sector. Female LFPR rose from 23 percent in 2005 to 36 percent in 2015.

According to it, increasing exports per worker in South Asia would result in higher wages for workers generally found in the formal sector and falling informality for many marginalized groups.

Bangladesh went for launching a wide-ranging trade reform strategy (including exchange rate policy reform) aimed at easing imports and expanding exports for rapid industrialization, led by the private sector.

Bangladesh’s exports of final apparel in 2013—which have nearly tripled since 2007—amounted to over USD26 billion, making it the second-largest exporter of final apparel in the world next to China. As a result, this economy’s exports are highly concentrated in textiles and apparel sectors.

Policies to benefits export growth

![]() Images/public/VD4GvKj9dTpGEED61zpFuT.pngBoosting and connecting exports to people (for example, by removing trade barriers and investing in infrastructure)

Images/public/VD4GvKj9dTpGEED61zpFuT.pngBoosting and connecting exports to people (for example, by removing trade barriers and investing in infrastructure)

![]() Eliminating distortions in production (for example, through more efficient allocation of inputs)

Eliminating distortions in production (for example, through more efficient allocation of inputs)

![]() Protecting workers (for example, by investing in their education and skills)

Protecting workers (for example, by investing in their education and skills)

![]() Scaling up exports in labor-intensive industries could significantly lower informality for groups like rural and less-educated workers. Other workers would also benefit from increasing skills and the participation of women and young workers in the labor force.

Scaling up exports in labor-intensive industries could significantly lower informality for groups like rural and less-educated workers. Other workers would also benefit from increasing skills and the participation of women and young workers in the labor force.

ABOUT THE RESEARCH

‘Exports to Jobs: Boosting the Gains from Trade in South Asia’ is a survey published by World Bank Group in association with International Labor Organization (ILO) to shed light on growth of south Asian region and reduction of poverty with export based job.

Monthly Business Review- April 2019

Banks/FIs deserve accolades for expanding their SME portfolio over the past years and thus exceeding the SME disbursement target given by the Central Bank. However, the financial industry is still saddled with some concerns when SME lending is in question. Banks find it hard to consider SME loans as a core focus segment because of the higher cost of monitoring and underwriting, as SMEs are scattered all across the country and are unstructured in terms of account management. Therefore, underwriting of SMEs is expensive and time-consuming since the cost and underwriting process for all borrowers (irrespective of size and value) are similar. FIs can come up with scoring models for SME businesses by deploying technology leveraging on the huge set of customer data. Also, more than just funding, small businesses require business management tools and advice on how to

diligently manage working capital and FIs are the best fit to help them out in this scenario.

Lastly, this is worthy to mention that the whole financial industry played a crucial role in building SME ecosystem and educating the market at this level, with prudent guidance from the Central Bank. Now, expanding the SME market reach in a low cost manner, by deploying technology should be the priority of Banks or FIs.

Download View