Capital Market Review

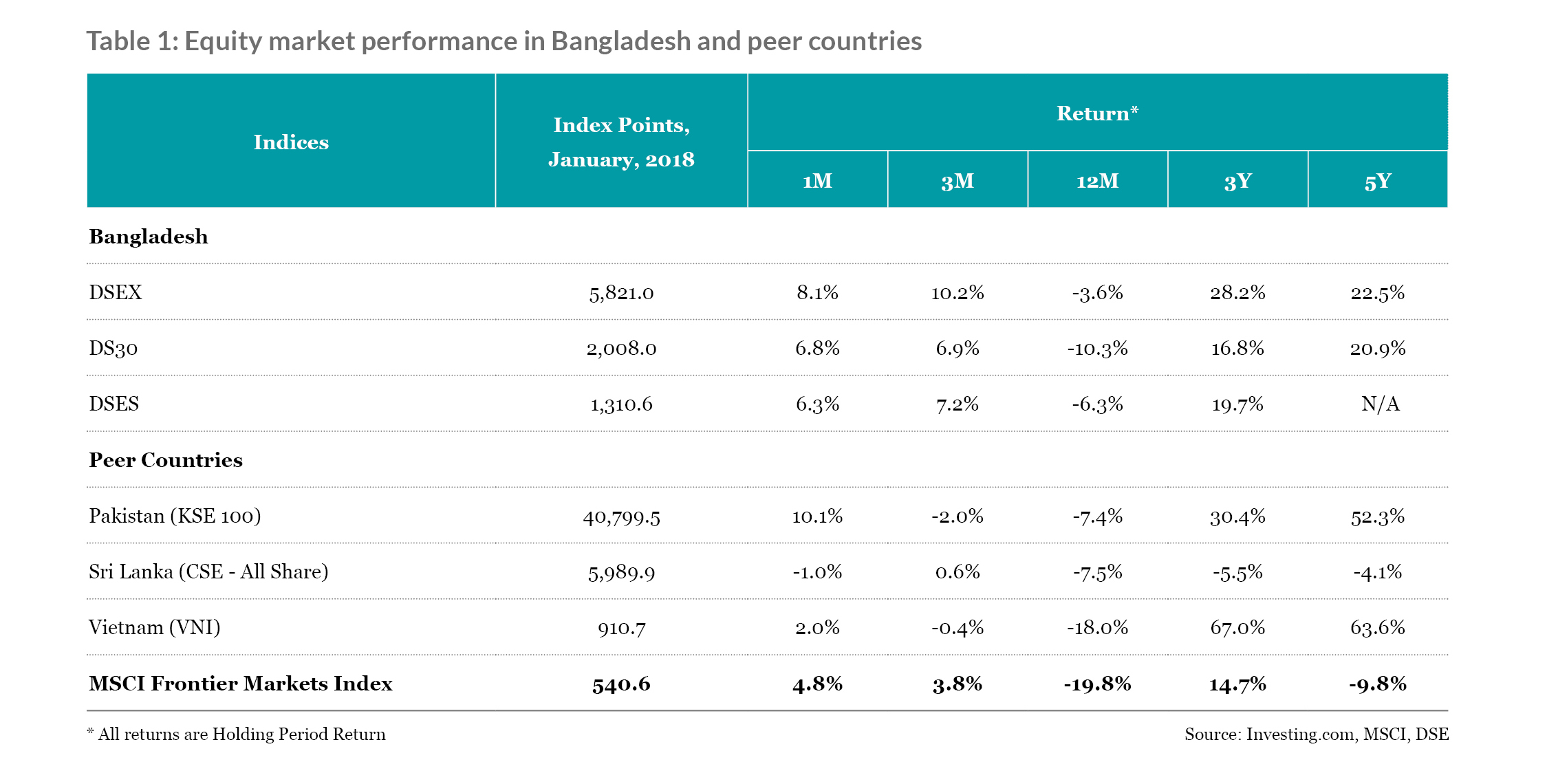

Performance of Equity Markets of Bangladesh and Peer Countries

Bangladesh equity market rejuvenated during the first month of 2019 amid post-election stable political scenario. During the month the broad index DSEX advanced by 8.1%, adding up 435.4 points. Blue chip index DS30 and Shariah index DSES also gained 6.8% and 6.3%, respectively.

Among the regional peers, Pakistan and Vietnam gained 10.1% and 2.0%, respectively during the month, while Sri Lanka lost 1.0%. Vietnam showed the most encouraging longer term track record with a 5 years’ return of 63.6%, while Bangladesh had 22.5% during the same period. Meanwhile, MSCI Frontier Markets Index ended the month with 4.8% return.

Liquidity Condition in Equity Market of Bangladesh

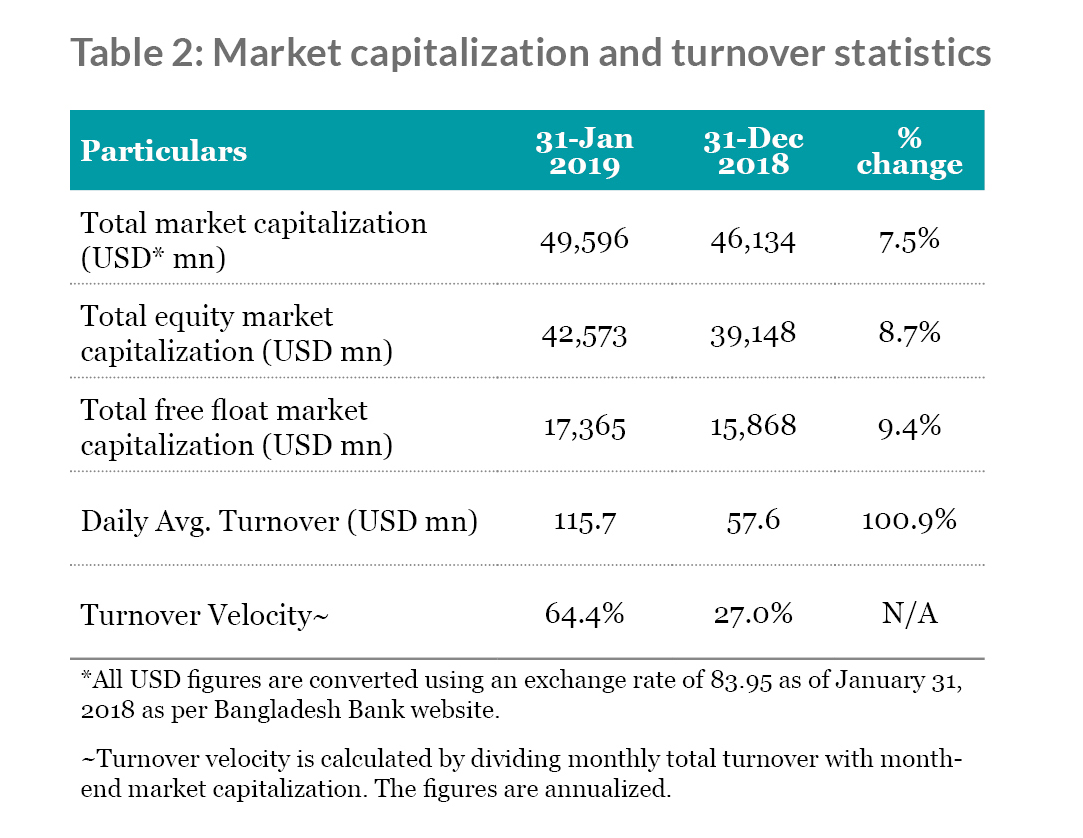

During January, the total market capitalization increased by 7.5%, while free float market capitalization increased by 8.7%. Meanwhile, average turnover of January 2019 was BDT 9.7 bn (USD 115.7 mn), increasing by 100.9% from that of last month. Accordingly, turnover velocity which represents overall liquidity of the market increased to 64.4% in January compared to 27.0% of last month.

Historical Index Points and Market Participation Data

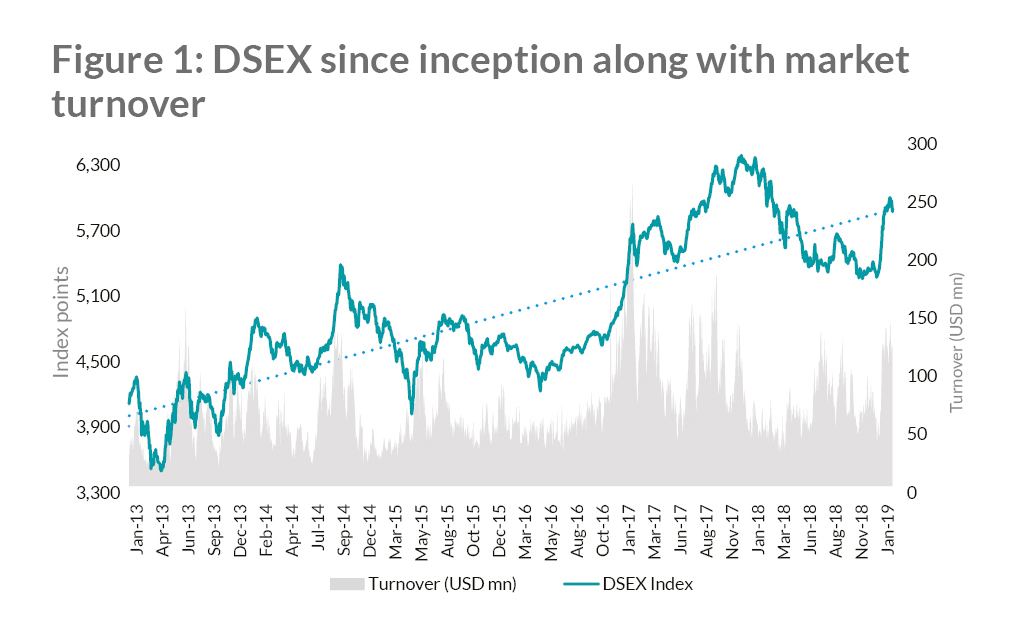

Since its inception on January 27, 2013, DSEX yielded a holding period return of 43.5% till January, 2019. During the same period, daily average turnover of the market amounted to BDT 5.5 bn (USD 66.0 mn) (Figure 1).

Market Valuation Level - P/E Ratio

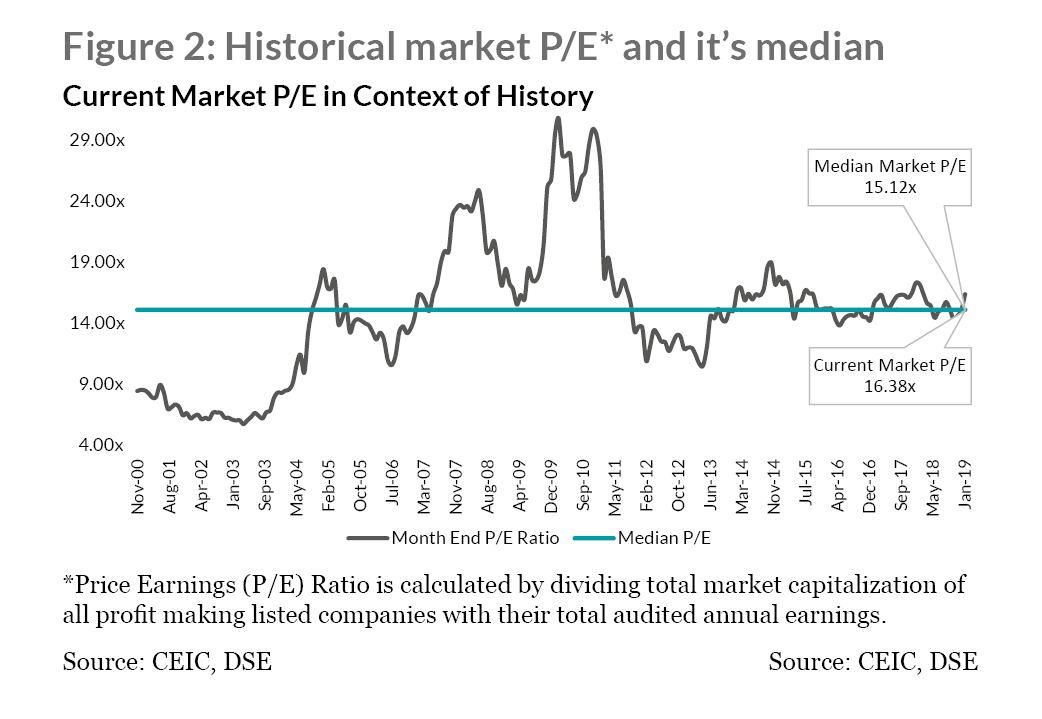

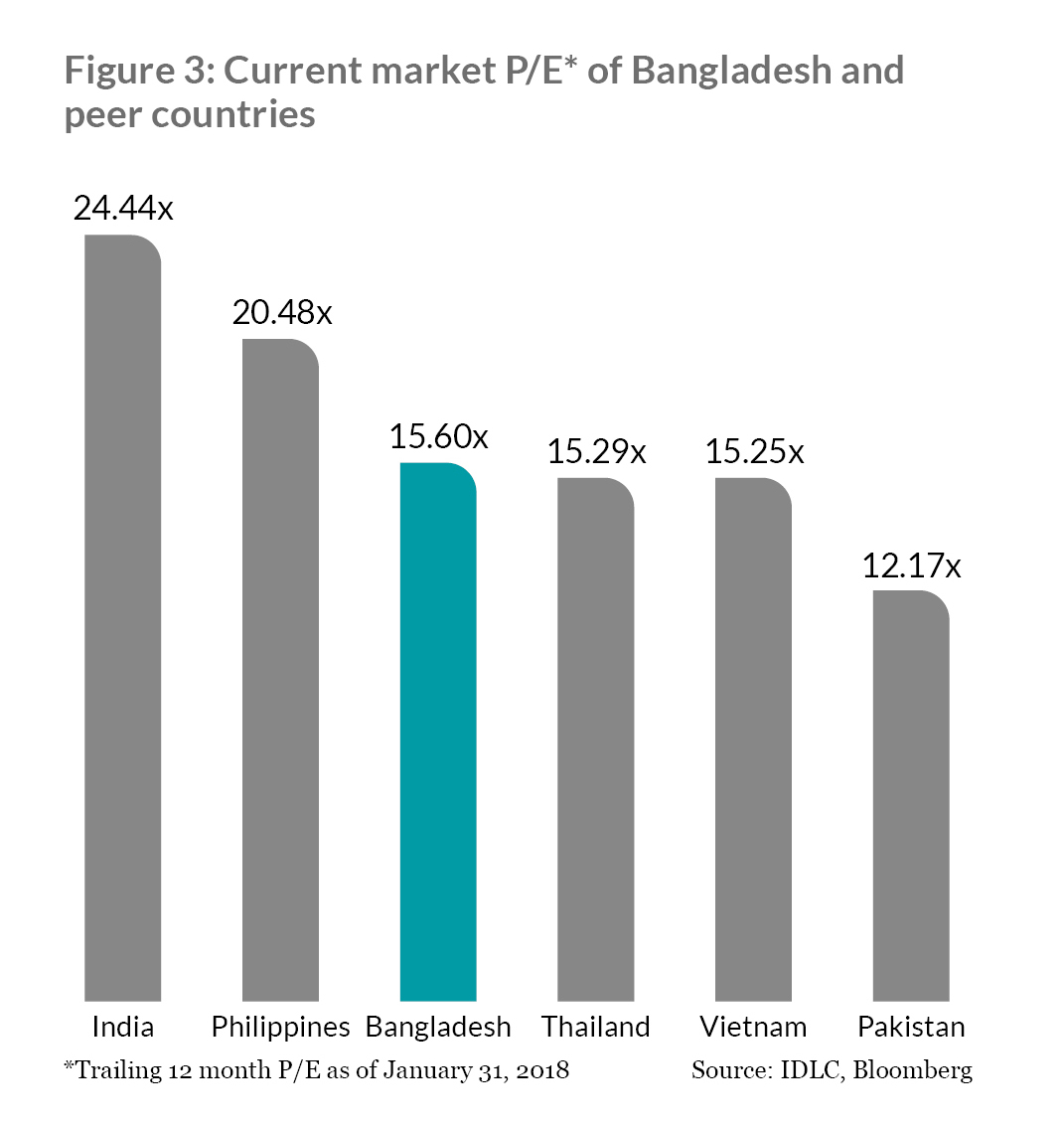

Increasing for the last three months, the market P/E as of January, 2019 was 16.38x, which is greater than 18 years’ median market P/E of 15.12x (Figure 2). In terms of trailing 12 month P/E ratio equity market of Bangladesh is still relatively undervalued than that of India and Philippines (Figure 3).

Sector Performance

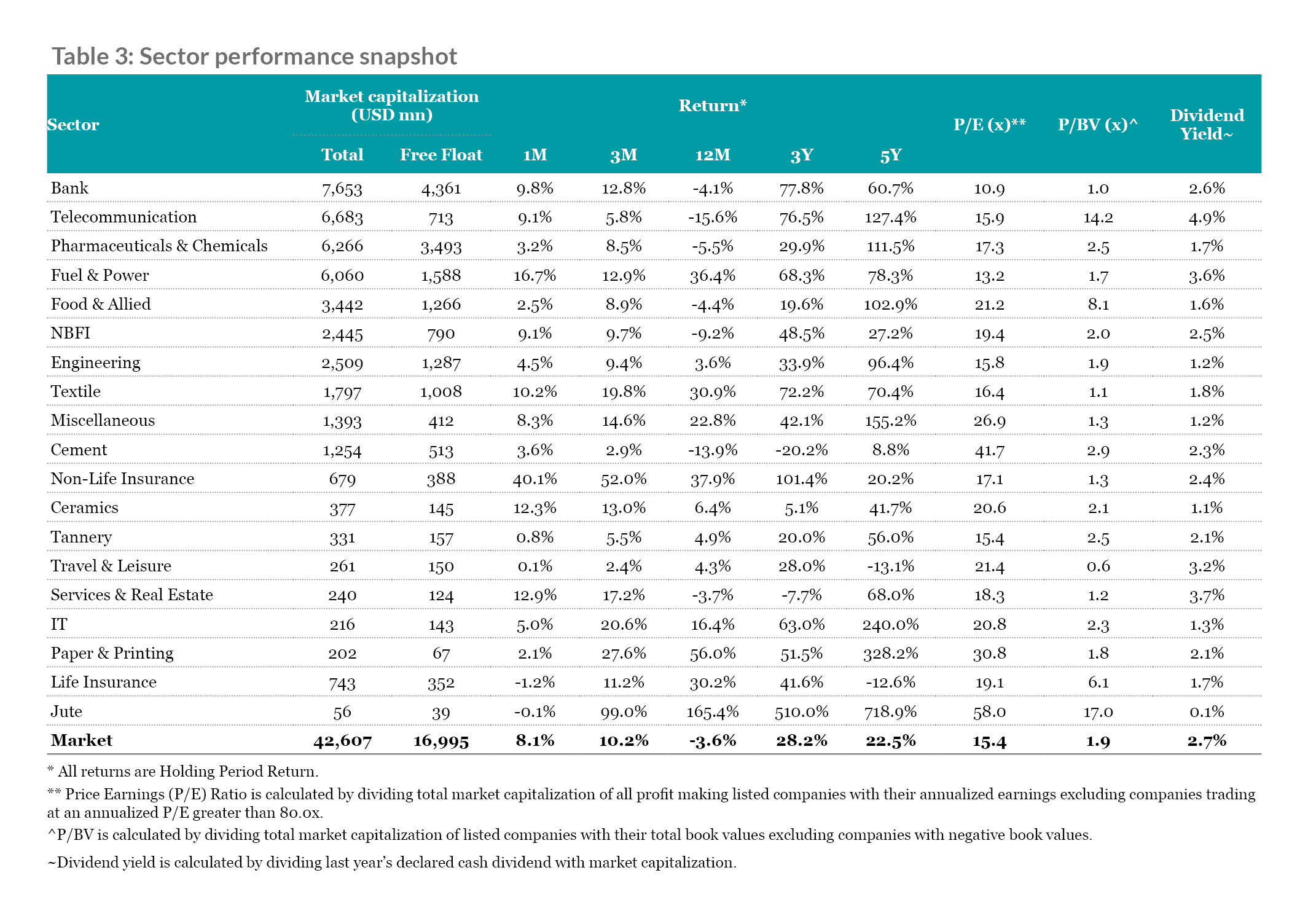

Among the major sectors, Non-Life Insurance yielded the highest return, appreciating by 40.1% in January. Fuel & Power followed next, advancing by 16.7%. Besides, Textile and Bank increased by 10.2% and 9.8%, respectively during the month. On the contrary, Life Insurance faced the highest selling pressure during the month, declining by 1.2%.

Despite good performance in January, the largest sector in terms of market capitalization, Bank is still relatively undervalued in terms of P/E ratio due to correction in previous year.

Cap Class Performance

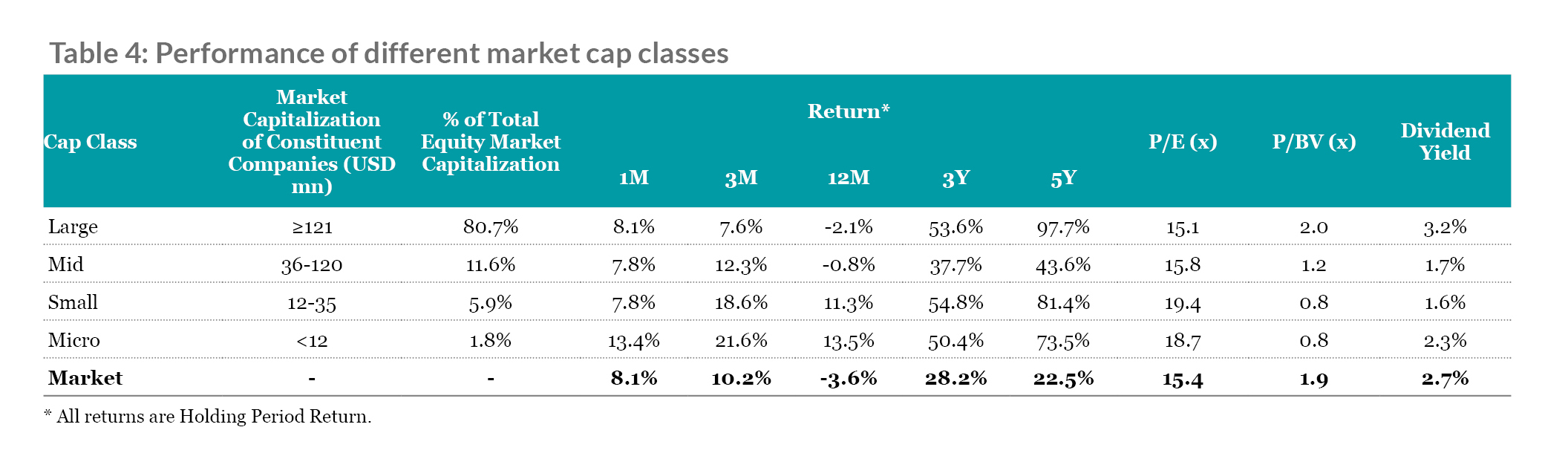

During the month of January, Micro Cap Class outperformed the market, yielding 13.4% return. While Large Cap Class paced with the market with 8.1% return, both Mid Cap Class and Small Cap Class increased by 7.8%

Performance of 20 Largest Listed Companies in Bangladesh

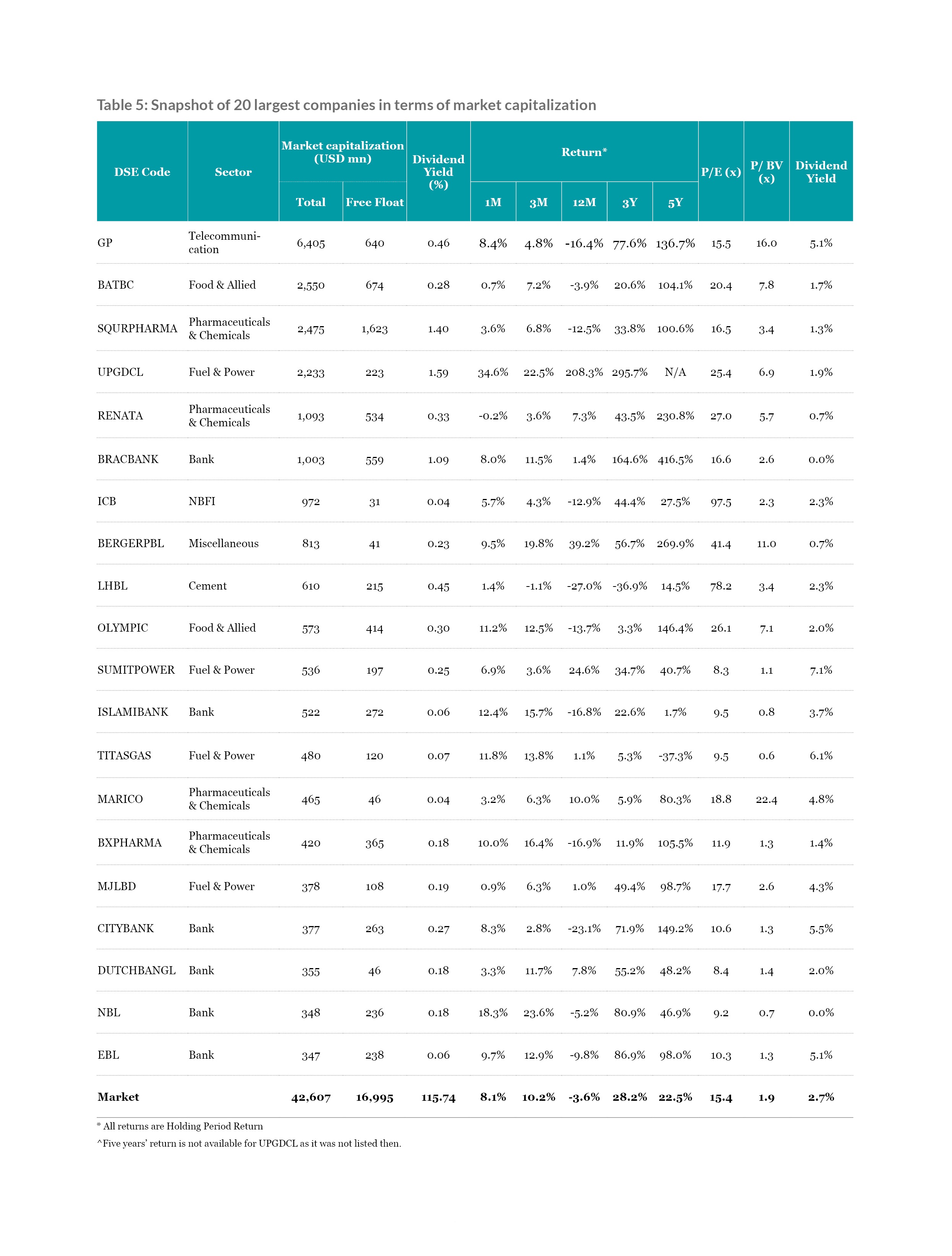

Among the 20 largest listed companies in terms of market capitalization UPGDCL (+34.6%), NBL (+18.3%), ISLAMIBANK (+12.4%), TITASGAS (+11.8%) and OLYMPIC (+11.2%) posted significant return. On the contrary, only RENATA (-0.2%) faced selling pressure during the month.

Majority of these companies yielded outstanding return over longer time horizon (5 years) such as BRACBANK (+416.5%), BERGERPBL (+269.9%), RENATA (+230.8%), CITYBANK (149.2%) and OLYMPIC (+146.4%).

Among the scrips SUMITPOWER, TITASGAS, CITYBANK, GP, EBL, MARICO, and MJLBD recorded a higher dividend yield compared to that of market. Moreover, SUMITPOWER has the highest dividend yield (7.1%) and lowest P/E (8.3x) among the 20 largest companies.

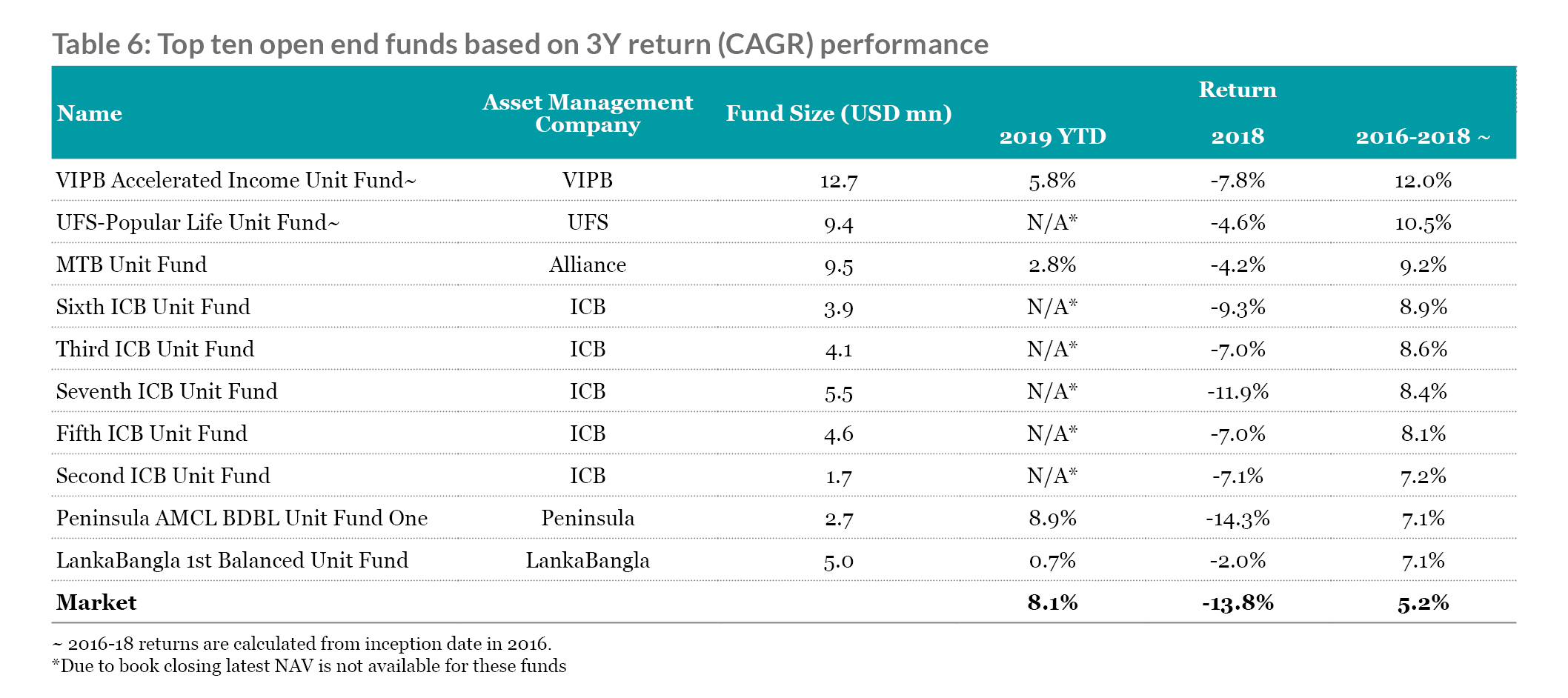

Top Performing Mutual Funds

Top ten open end mutual funds based on 3 year CAGR outperformed the market during the same period. Among them VIPB Accelerated Income Unit Fund (12.0%) and UFS-Popular Life Unit Fund (10.5%) made significant return. However, based on available data of 2019, Peninsula AMCL BDBL Unit Fund One made the highest return.

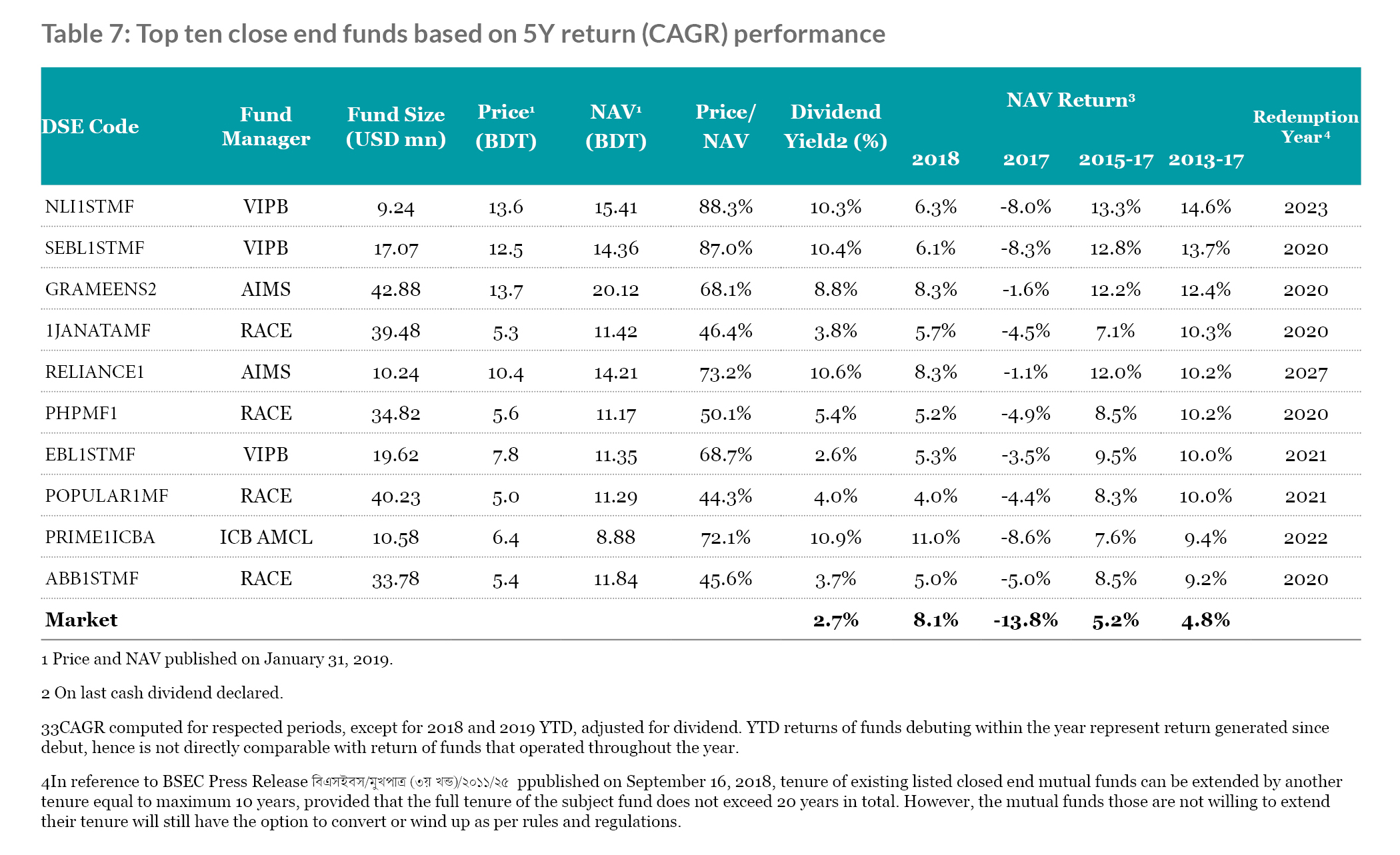

The top ten closed end mutual funds on the basis of 5 years (2014-2018) performance yielded positive return in January, 2019 yet underperformed the market. Among these funds, PRIME1ICBA (11.0%) and RELIANCE1 (8.3%) gained the most.

Despite strong performance in January, 2019, the funds are traded at a lucrative discount compared to their NAV. Besides, all the funds also offered higher dividend yields compared to market except for EBL1STMF. (Table 7).

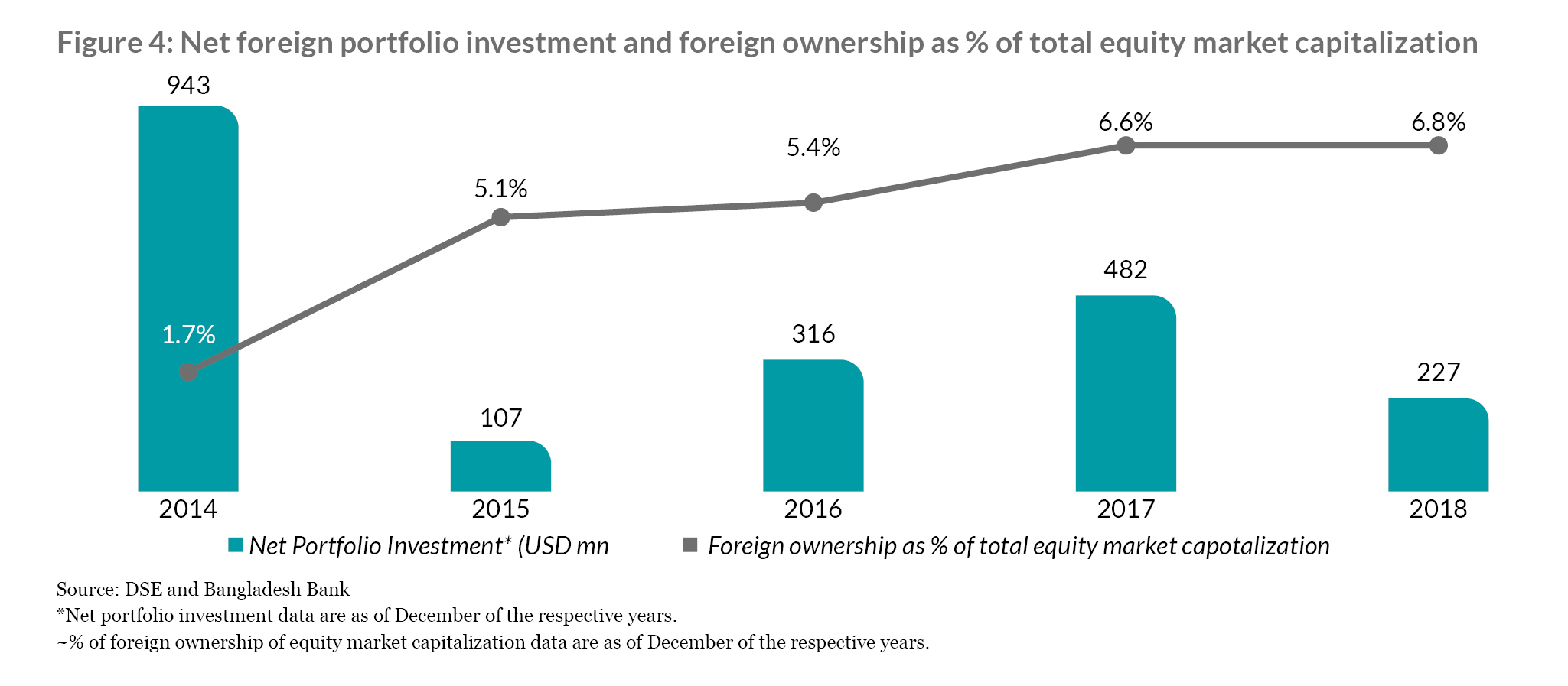

Foreign Participation in Equity Market of Bangladesh

Over last 5 years, Bangladesh equity market has seen a surge of foreign investment. As of December, 2018 total foreign ownership stood at 6.6% of the total equity market capitalization, which was only 1.7% in 2014.

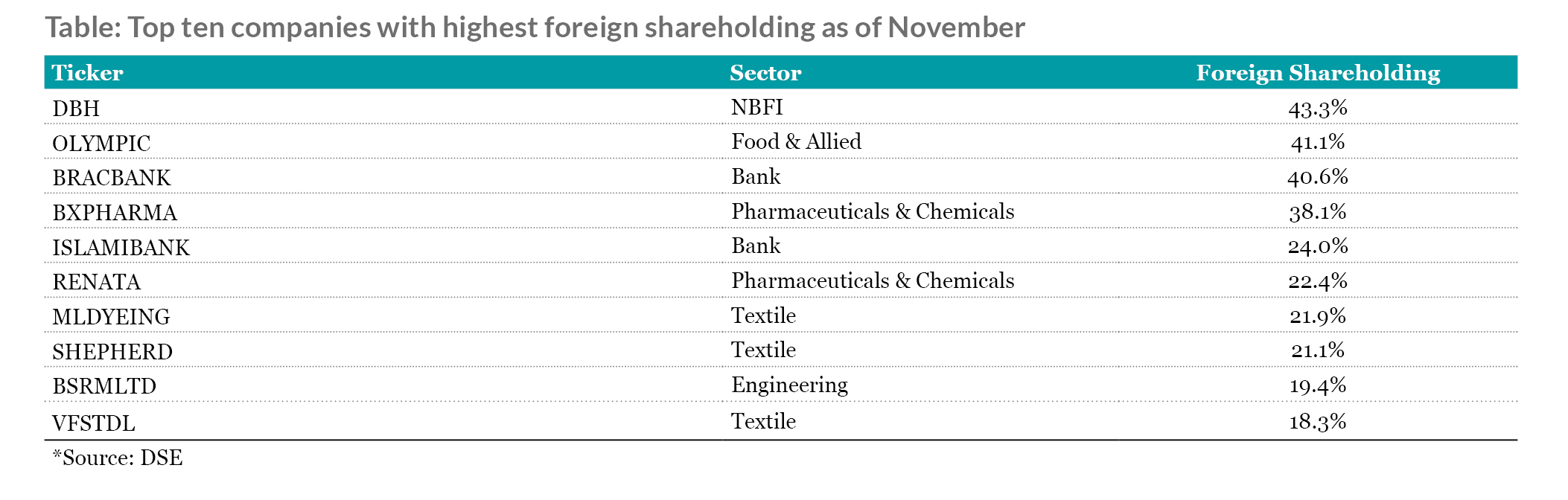

Among all the companies with foreign ownership, DBH had the highest foreign shareholding of 43.3% as of December 2018, followed by OLYMPIC with 41.1%.

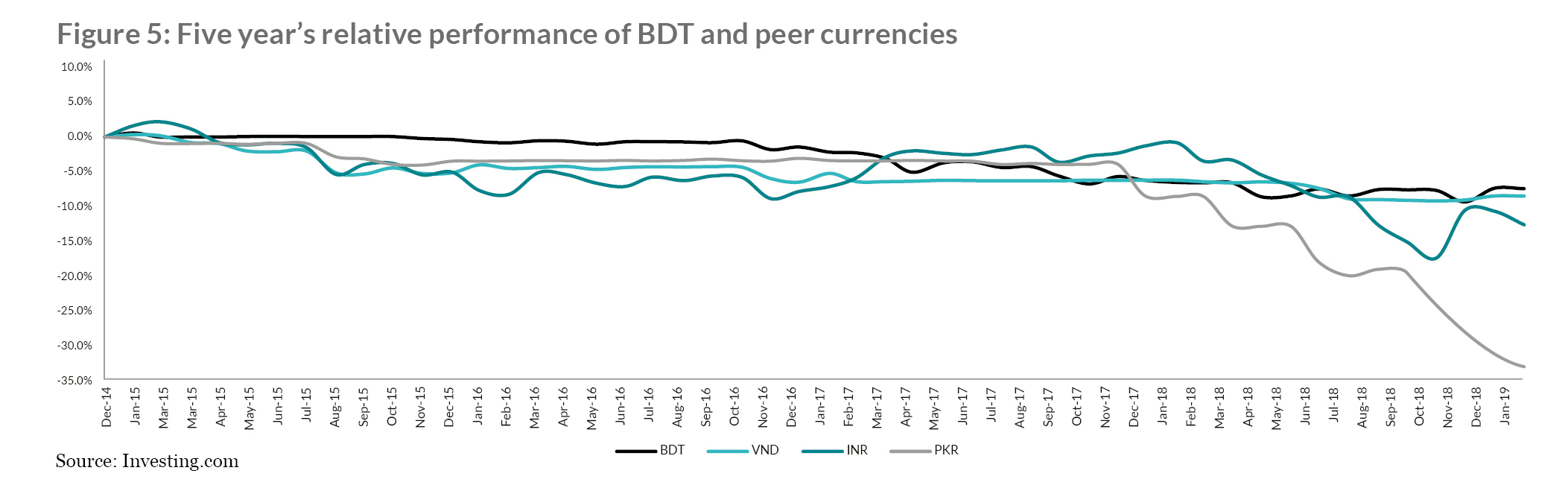

Performance of BDT and Currencies of Peer Countries against USD

Since 2015, BDT retained its value better than the currencies of peer countries. While BDT depreciated by 7.4% against US Dollar, other currencies of neighbor countries like Vietnamese Dong (VND), Indian Rupee (INR) and Pakistani Rupee (PKR) lost 8.5%, 12.6% and 38.2%, respectively.

Monthly Business Review- February 2019

Bright picture for Capital Market in 2019

The Market Capitalization (Mcap) /GDP ratio lowered to 17% in 2018 from 24% in 2014, whereas the peer countries mostly picked up for peer countries. One potential reason for this phenomenon is lack of listing of large corporates in the market. However, 2018 witnessed a number of developments in the form of partnerships and regulations. The strategic partnership between DSE and a Chinese consortium of Shanghai and Shenzhen Stock exchanges is expected to contribute in capital market improvement. BSEC approved the draft Qualified Investor Offer by Small Capital Companies Rules, 2018 that is expected to increase efficiency of the market by providing a separate market for small cap companies.

Future prospect of the capital market in 2019 looks bright as government expects GDP growth to be at 7.8% and inflation at 5.6%. Economic Intelligence Unit (EIU) and UN predicted Bangladesh to be one of the fastest growing economy. Provided that interest rates remain under control and liquidity conditions improve, the market is expected to perform better. Stable political environment will attract foreign investment and improvement of exports and remittance can help ease pressure on currency.

Download View